Will Anthem Blue Cross withdrawing from Covered California SHOP cause the program to crash?

Anthem Blue Cross of California has withdrawn their application to offer small group health insurance plans through Covered California. Initially, Covered California required that carriers that wanted to participate in the new individual market place also had to participate in the Small Business Health Options Program (SHOP). That requirement was dropped in June and emerging details suggest that Anthem Blue Cross no longer saw a benefit from offering small group health plans through Covered California.

Are small group health plans doomed?

There has been lots of speculation on whether guarantee issue individual and family plans offered through Covered California will spell the end of the small group health plans. The evolving question now is whether Covered California’s SHOP will be a real “value added” alternative for small businesses. Employers with less than 50 full time employees will not face any penalties if they don’t offer health insurance to their employees as will larger companies. Since employees of small businesses might be eligible for the Advance Payment Tax Credit through Covered California, their monthly premiums might actually be lower through the new health insurance marketplace than with a small group health plan.

Carriers already have extensive small group framework

Large health insurance carriers such as Anthem Blue Cross, Blue Shield of California, Health Net, Kaiser and many others have significant marketing and operational structures established for both the small and large group markets. In addition to their appointed independent agents, these large carriers work with general agencies such as BenefitMall and Word and Brown to market their products. The SHOP program isn’t necessarily offering them anything they don’t already have in place.

The money is in life insurance

Unlike the individual and family market health plans purchased through Covered California that will be invoiced directly by the respective carrier, the SHOP plans are to be purchased and administered by Covered California. In other words, a small business that purchases SHOP coverage would be invoiced through Covered California. Does a large carrier like Anthem Blue Cross really want to diminish their ability to sell new ancillary products such as dental, vision and life insurance because they won’t be billing the group directly? Those are all products that don’t fall under the Medical Loss Ratio regulations and can represent valuable profit centers for the carriers.

Little market growth potential in small group

The prospect of expanding membership and market share through individual health insurance because of the “individual mandate” is far greater than any market expansion for small business group health plans. When a small business owner considers that their employees might achieve lower costs through Covered California coupled with the hassle of administering a small group health plan, many employers might just jettison existing plans and never look at SHOP.

Covered California is replicating existing marketing channels

On a recent webinar with the Director of Sales and Marketing for Covered California, Michael Lujan, he reviewed the ongoing implementation for the exchange to support SHOP. This included the administration of SHOP by Pinnacle Claims Management who has hired sales directors for Northern and Southern California. Before insurance agents can represent the small group health plans offered through Covered California they will have attend 12 hours of training and pass a test.

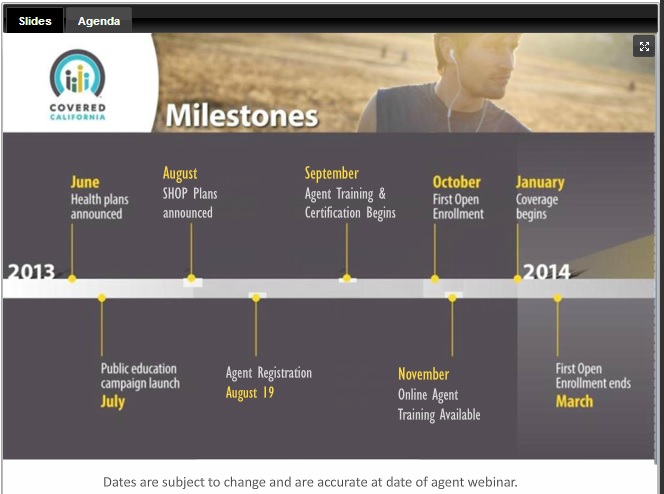

Covered California timeline of agent and SHOP dates.

CalSIM, no growth in small group market

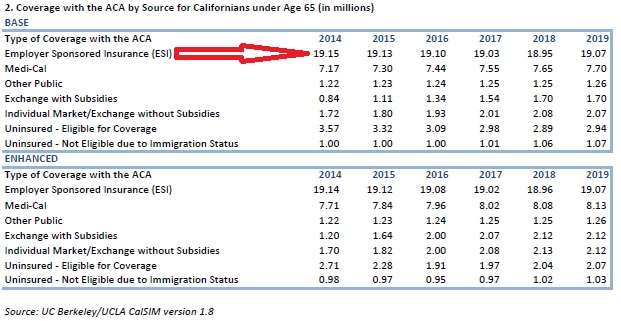

Lujan also referenced the CalSIM data which was funded by The California Endowment and conducted by UC Berkeley Center for Labor Research and Education and the UCLA Center for Health Policy Research. The California Simulation of Insurance Markets (CalSIM) estimates the number of subsidy eligible Californians by region and demographics. Included in the CalSIM data is projected changes to employer sponsored insurance plans. CalSIM projects a flat to declining numbers for small group health plans.

CalSIM data: no increase in employer sponsored insurance enrollment.

Carriers locking up small group business

The numbers indicate that not many small businesses will be enticed to move into the SHOP program. These numbers were forecast before the large carriers such as Anthem Blue Cross, Blue Shield of California and Kaiser started small group retention programs. Essentially, the large carriers have been offering early renewals with favorable terms to retain their small group clients which have the impact of dulling any speculated exodus to SHOP or scrapping the small group plan altogether. Consequently, there may be even fewer small businesses that will seriously look at SHOP.

Is there a need for SHOP?

If a small business doesn’t offer health insurance currently, there seems to be little likelihood that they will consider SHOP. Reluctance to start a small group plan combined with existing small group plans locked in for another year and businesses that will scrap current group coverage represents a diminishing pool of potential companies for the Covered California program aimed at small businesses. From a purely administrative standpoint, Anthem Blue Cross may have seen little to gain from offering new small business plans through Covered California. If there is no new business to be gained and they already have their marketing channels in place, other carriers with established small group plans might also consider pulling out of SHOP.

Small group benefits

There are still many advantages to having a small group plan which include health benefits that are deducted pre-tax and lower the withholding taxes for both employee and employer. In addition, small businesses can offer dental, vision, life and disability insurance with better coverage and lower rates than found in the individual market. All of these advantages, including rates probably as competitive as SHOP, are already available to any small business interested in a small group plan. They don’t have to use Covered California.

Insurance agents can add value

There is little doubt that insurance agents will be a valuable source of information and sales for Covered California in both the individual and small group health plan markets. A central theme of Michael Lujan’s comments during the webinar was directed at alleviating anxiety from the fear of the unknown among insurance agents. The fear of not knowing what to expect also pervades the small and large business community with respect to the tectonic shifts in the health insurance market place brought on by the Affordable Care Act.

You jump in first

Since the only mandate falls on the shoulders of individuals and families to secure health insurance in 2014, I suspect many businesses will take a wait and see approach before they jump into the group insurance market place. Small businesses that are happy with their existing plans will likely opt to stay put and not become a “test case” for the new SHOP plans and potentially incur the wrath of their employees if a new plan produces unwanted headaches.

Will Anthem Blue Cross withdrawal start a trend?

This scenario might subtly change if the new SHOP plans offer unprecedented value for businesses above and beyond their current situation. But with the pulling out of Anthem Blue Cross from the Covered California SHOP program they are signaling that they have plenty of faith in their existing small group health plan framework and competitiveness. We’ll have a better understanding of the small group health plan market place and SHOP after Covered California announces the carriers, plans and rates in August.

Insurance Commissioner fist pump

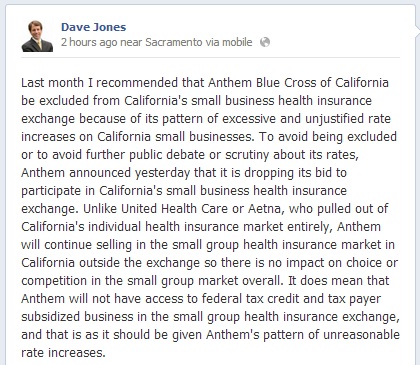

Insurance Commissioner Dave Jones was gleeful on his FaceBook page over the fact that Anthem Blue Cross has withdrawn from the SHOP program after he called for them to be excluded from the Covered California small business program last month. Commissioner Jones felt Anthem should be banned because of their pattern of “excessive” rate increases. He attributed Anthem’s withdrawal as a preemptive move as opposed to being embarrassed over not being selected to participate in SHOP. If that is the case, Commissioner Jones has more “insider” information about contract negotiations at Covered California than most people.

Insurance Commissioner Dave Jones gloats over Anthem’s withdrawal.

Politics or economics?

Was Anthem’s move to withdraw political? Did they see the error of their ways, and not wanting to cross political paths with Commissioner Jones, and decide they were not worthy to participate in SHOP? I can completely understand the frustration from Dave Jones over the numerous rate increases that Anthem Blue Cross filed for their small group plans.

Why has Anthem Blue Cross filed so many rate increases?

- Because they can. Yes

- Because their actuarial staff is stupid and miscalculated the cost of health care. Doubtful

- The cost of health care and utilization is rising faster than anticipated. Maybe

- They had low premiums to “buy” business and now have to adjust to market levels. Maybe

- They have to raise premiums to cover anticipated Affordable Care Act provisions such as no cost preventive office visits. Yes

- They are spiking rates in advance of full implementation of the ACA. Maybe

Insurance industry is three steps ahead of Covered California

Regardless of the reasons why Anthem Blue Cross withdrew their application Commissioner Jones is correct; nothing is going to change in the small group market. Large carriers like Anthem have already built huge complex software programs that exceed the size of what Covered California is creating in order to administer and market their insurance products. As much as I support Covered California, they are no match for business resources of health insurance industry.

Small business loathes health care reform

Anthem Blue Cross also recognizes how little support there is among small business for health care reform specifically and government in general. From my own discussions with small business owners, which is purely subjective and anecdotal, there is overwhelming opposition, if not pure hostility, on the part of small business towards government involvement with health care. This is irrational from my standpoint, but companies like Anthem Blue Cross are also fueling the conspiratorial anti-government flames by funding websites focused on repealing the Affordable Care Act.

[wpdm_file id=82 title=”true” desc=”true” ]