Health plans are more complicated solving a quadratic equation. However, I do remember from my calculus classes to break the problem into different parts in order to find the answer. Even though health plans do not have final result, in most cases, we can still break the problem down into separate parts to better understand their functions.

Coverage Sections: MOOP, Deductibles, Prescriptions, Health Care Services

The nice aspect of the Covered California health plans is that they are essentially uniform across the different carriers. Whether you buy a Silver 70 plan through Covered California or directly from the carrier, off-exchange, they operate and function the same way. The caveat in this discussion is there can be slight variations between PPO and HMO plans and non-standard benefit design plans off-exchange.

Annual Maximum Out-of-Pocket Amount

The annual Maximum Out-of-Pocket (MOOP) amount is your maximum liability for health and drug expenditures when using network providers of the health plan. In a world where surgeries and cancer treatments can easily exceed $100,000, limiting your liability to less than $10,000 for an individual is a big deal. One way to think of health insurance is asset protection. In the worst medical crisis imaginable, you know your medical expenses will be capped. This protects you from having to sell your assets or declaring bankruptcy.

Once you hit the maximum out-of-pocket amount, all in-network health care services and prescription drug cost are covered 100 percent by the health plan. While the annual out-of-pocket maximum is very important, it should not be the biggest factor in deciding a health plan. Even though a Platinum plan has a maximum amount of $4,500, which is lower by $3,700 over the Bronze plan, the annual premiums of a Platinum plan will usually exceed the $3,700 difference. When 2 family members meet the MOOP, it is met for all other family members on the health plan.

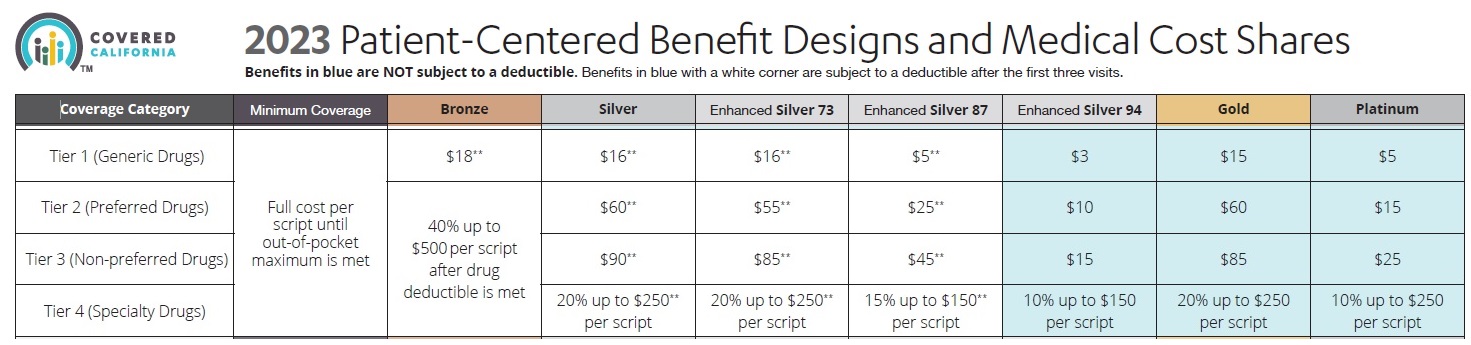

Deductibles: Medical, Pharmacy

Not shown on the Covered California metal tier plan summary is the Bronze HDHP. With the Bronze HDHP, the combined medical and pharmacy deductible is $7,000 which is also the maximum out-of-pocket amount. When you have met the deductible, you have met the MOOP and all health care costs are covered for the year.

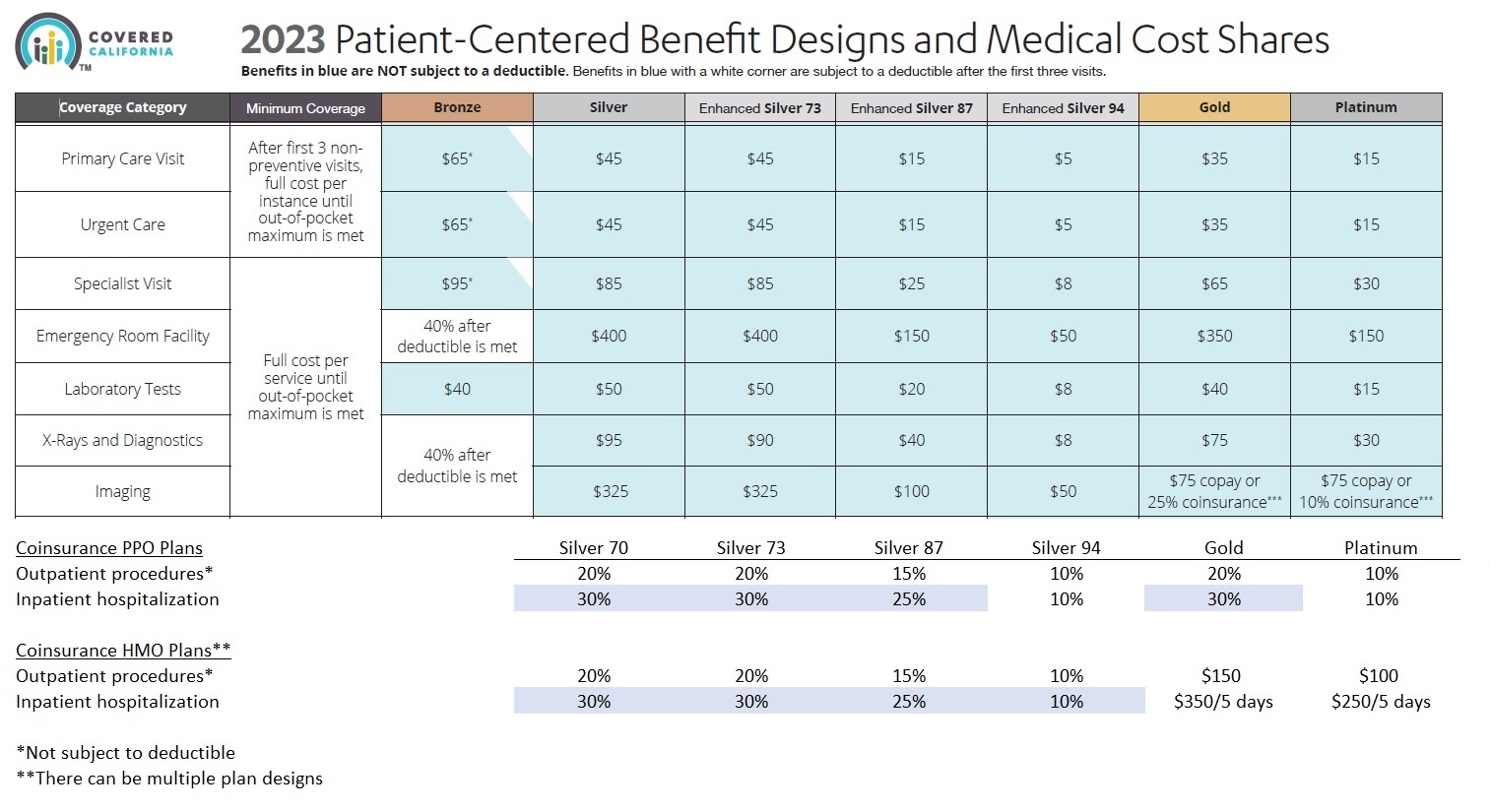

The Standard Bronze 60 plan has $6,300 individual medical deductible. While the Bronze 60 has three office visits and labs at a set copayment, you have to pay the full negotiated rate for medical services until you have reached the deductible of $6,300. After the deductible has been met you go into 40 percent coinsurance. You pay $0.40 of the next dollar billed and the health plan pays $0.60. When the deductible, any copayments, and coinsurance equals the MOOP, then the health plan covers everything for the remainder of the year.

Gold and Silver plan have no medical or pharmacy deductibles. You go straight into a set copayment or coinsurance percentage. When all the copayments and coinsurance equals the MOOP, the health plan pays for everything for the remainder of the year. When 2 family members meet the deductible, it is met for all other family members on the health plan.

Silver plans are interesting because the medical deductible is only applied to inpatient hospitalizations and skilled nursing facilities. The deductible does not have to be met for many routine services and procedures that either have a set copayment or coinsurance. Many people are never subject to the medical deductible during the year. In addition, you can meet the maximum out-of-pocket amount of the plans without ever have a medical service subject to the deductible.

Prescription Drugs Benefits

The Bronze plans have no real mechanisms to lower prescription drug costs until your have met your annual out-of-pocket maximum amount. If your primary drugs are generic and are low in cost, a Bronze plan may be satisfactory. If you are prescribed a brand name and specialty drugs, a Silver or higher metal tier will help financially. The Silver plans have a modest pharmacy deductible that must be met before you go into either the tiered copayment or coinsurance cost structure.

Even with the higher premiums of the Silver, Gold, and Platinum plans, the savings from set copayments and coinsurance for expensive drugs will be greater than the savings with a lower premium Bronze plan. There is also a maximum cap on the monthly cost of specialty drugs with the Silver and higher metal plans. For the Silver plan, if you are prescribed a Tier 4 drug with cost of $1,000, your pharmacy price would be $200, which is equivalent to 20 percent. If the drug cost $2,000, the 30-day supply would be capped at $250, not $400, the 20 percent coinsurance.

What is important is to run all your prescription medications through the insurance plan. The costs of the drugs accumulate toward meeting your out-of-pocket maximum. Even if you receive a lower price for a drug using a pharmacy discount program, it can be beneficial to run the prescription through the health plan to realize the cost as accumulating toward your pharmacy deductible and maximum out-of-pocket amount.

Each health plan has its own drug formulary. If you have specific drug or brand name medications, you’ll want to check to make sure the drug is even covered for cost-sharing. A drug with one health plan might be Tier 2, while another health plan can have the same drug listed as Tier 3. While the higher tier means you will pay more on a monthly basis, the health plan with the higher Tier 3 drug may have the doctors you want to see in-network.

Routine Health Care Services Member Cost Sharing

For most people, the covered health care service benefits of the health plans, with set copayments, is the heart of health insurance. There is a menu of routine health care services that are not subject to the medical deductible. The service is either a set copayment or coinsurance and helps bring affordability and predictable to health care services.

The Bronze HDHP has no copayments or coinsurance. You pay the full negotiated rate for the services until you meet your annual maximum out-of-pocket amount, then everything is covered 100 percent by the health plan. The Bronze 60 includes 3 office visits at a set copayment and unlimited laboratory tests at $40. With the Bronze 60 you must pass through a $6,300 medical deductible before you go into the 40 percent coinsurance phase for many of the health care services.

For people who must use health care services on a regular basis, a Silver, Gold, or Platinum plan will save money in the long run over a Bronze plan. As most people will not meet their maximum out-of-pocket amounts during the year, having set copayments for routine services such as office visits, labs, tests, and imaging can save a lot of money.

Confusing Coinsurance

The one wildcard with outpatient services is the coinsurance. Coinsurance is a percentage of the invoiced services that the health plan member is responsible for. For outpatient procedures, the coinsurance is not subject to the medical deductible for Silver plans. However, you may find yourself getting billed for coinsurance when you thought the health service had just a set copayment. For example, imaging with the injection of a dye to enhance image contrast. The machine imaging scan will have a set copayment, but the injection of the dye is considered an outpatient procedure subject to coinsurance.

Coinsurance is also a health plan cost sharing element that changed for the 2023 plan year. Inpatient hospitalization coinsurance has increased for most Silver and Gold plans. Whereas coinsurance for the Silver 70 plan is 20 percent, in 2023, if you are hospitalized, the percentage increases to 30 percent. In other words, after you have met your medical deductible when you are in a hospital, you pay $0.30 of the next dollar invoiced and the health plan pays $0.70.

The higher inpatient coinsurance coupled with a higher annual maximum out-of-pocket amount for the Silver and Gold plans in 2023 means the consumer has higher medical cost liability for health care services than in 2022. Always carefully review the summary of benefits and the Evidence of Coverage documents of the health plans. HMO plans can have a couple of different plan designs with some plans substituting coinsurance percentage for set hospitalization copayments.