Selecting a health plan can be confusing. California has many different health plans for individuals and families throughout the state, but some of them are very regional, and they may not be offered to you. Below is an overview of health plans offered in California for 2026.

California Individual and Family Plan Overview

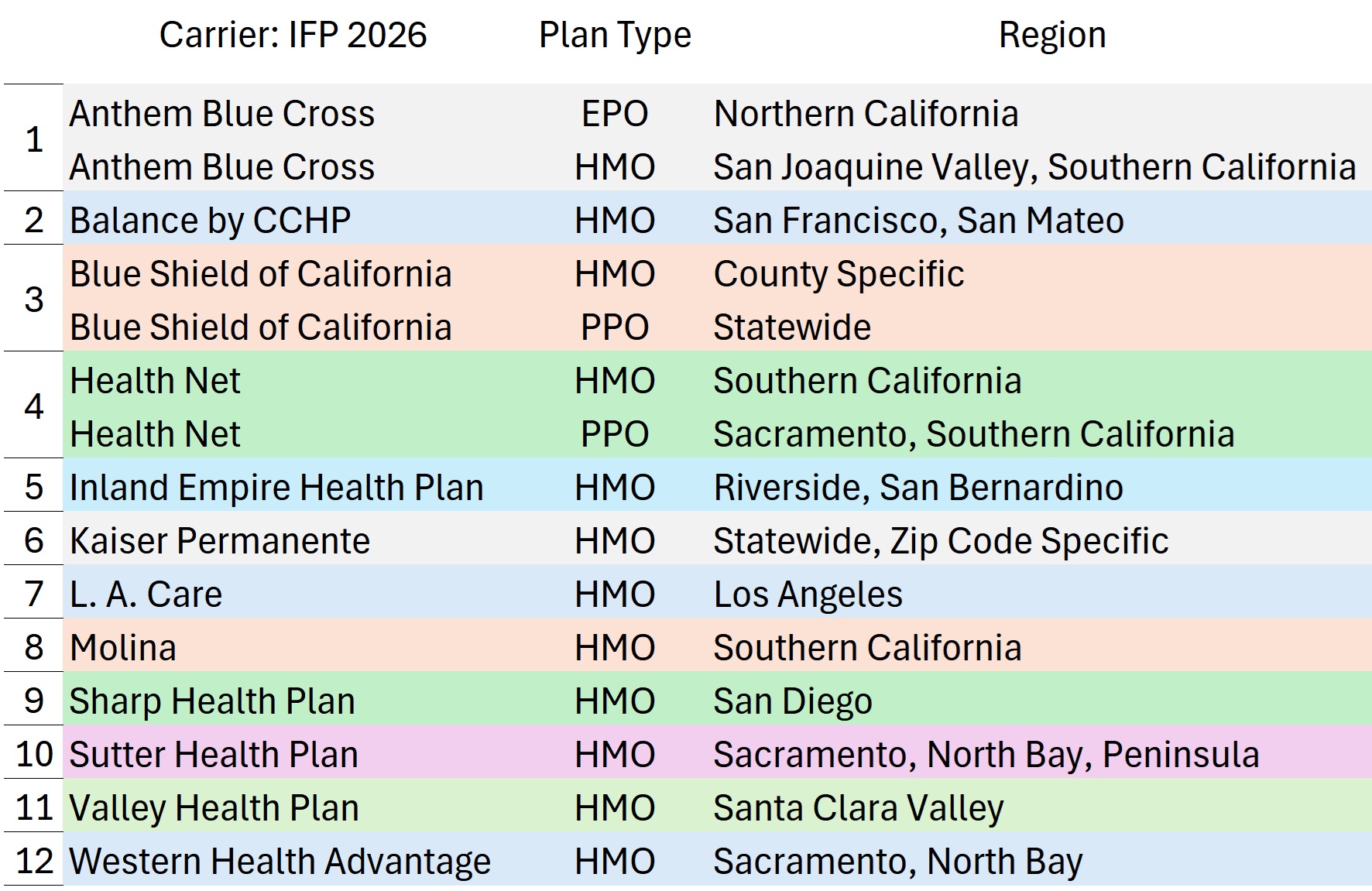

There are 12 different carriers offering several plan types of EPO, HMO, and PPO plans.

Anthem Blue Cross offers their EPO product in Northern California and their HMO product in San Joaquin Valley and Southern California, they don’t cross over. Balance by CCHP offers their HMO plan in San Francisco and San Mateo Counties.

Blue Shield of California has an HMO plan that is not statewide. It is offered in specific counties, so you need to check to see if it’s available to you. Blue Shield of California PPO is the only health plan that is truly statewide from Crescent City all the way down to the Imperial Valley. Health Net of California offers an HMO in Southern California and a PPO in Sacramento and Southern California.

Inland Empire Health Plan offers an HMO plan only in Riverside and San Bernardino Counties. Kaiser Permanente is kind of statewide, but it’s very zip code specific. For instance, if you’re in Placer County, you might have access to Kaiser, but if you go up Interstate 80 towards Lake Tahoe, you may be too far away, and Kaiser is not available.

L.A. Care is only in Los Angeles County. Molina, is in Southern California and some of the eastern counties. Sharp Health Plan is only in San Diego County with their HMO product. Sutter Health Plan is an HMO in Sacramento, the North Bay, and the Peninsula areas of Northern California. Valley Health Plan is only in Santa Clara Valley. Western Health Advantage is in the Sacramento area and the North Bay. Covered California, which represents most of these carriers does a good job with their shop and compare tool.

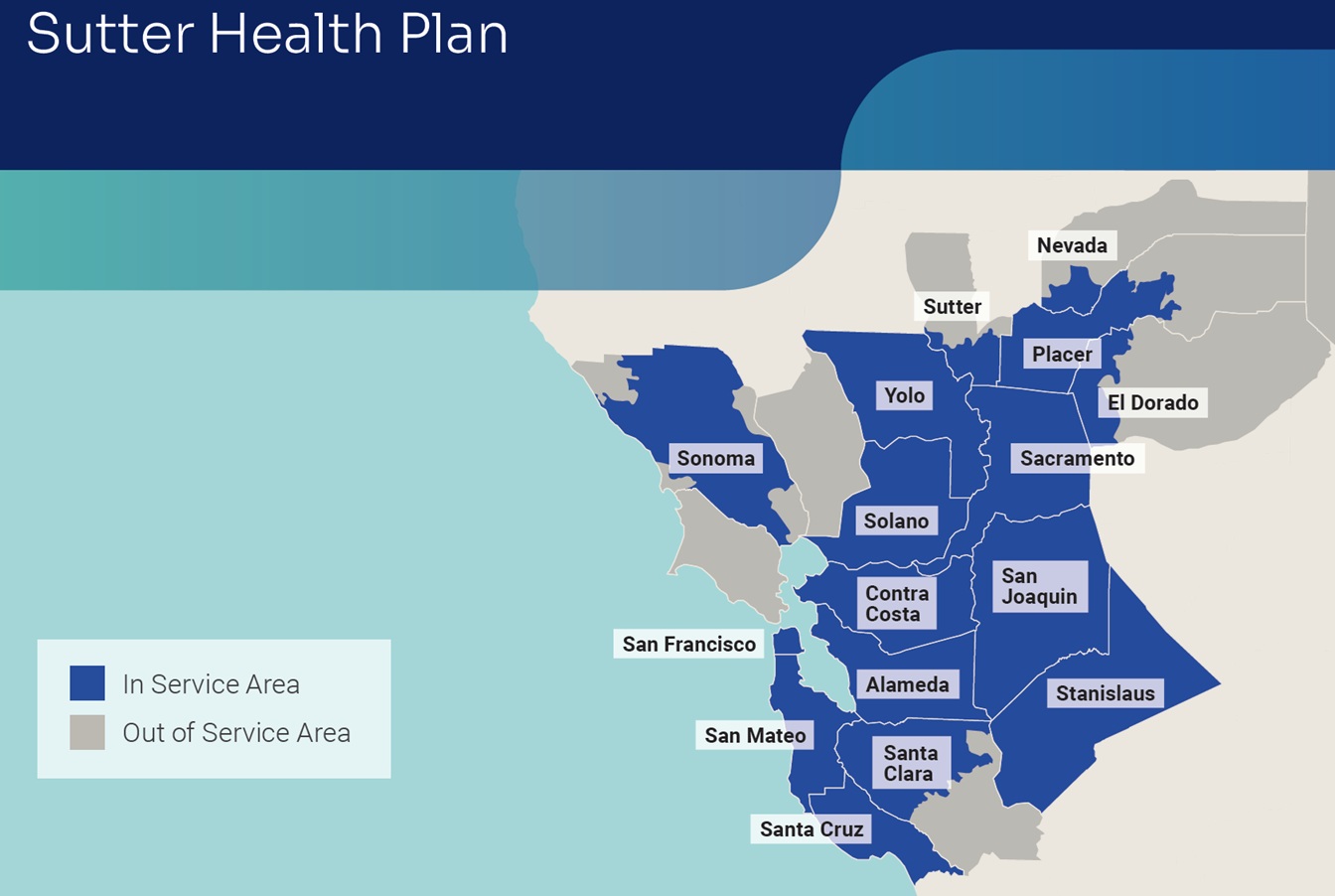

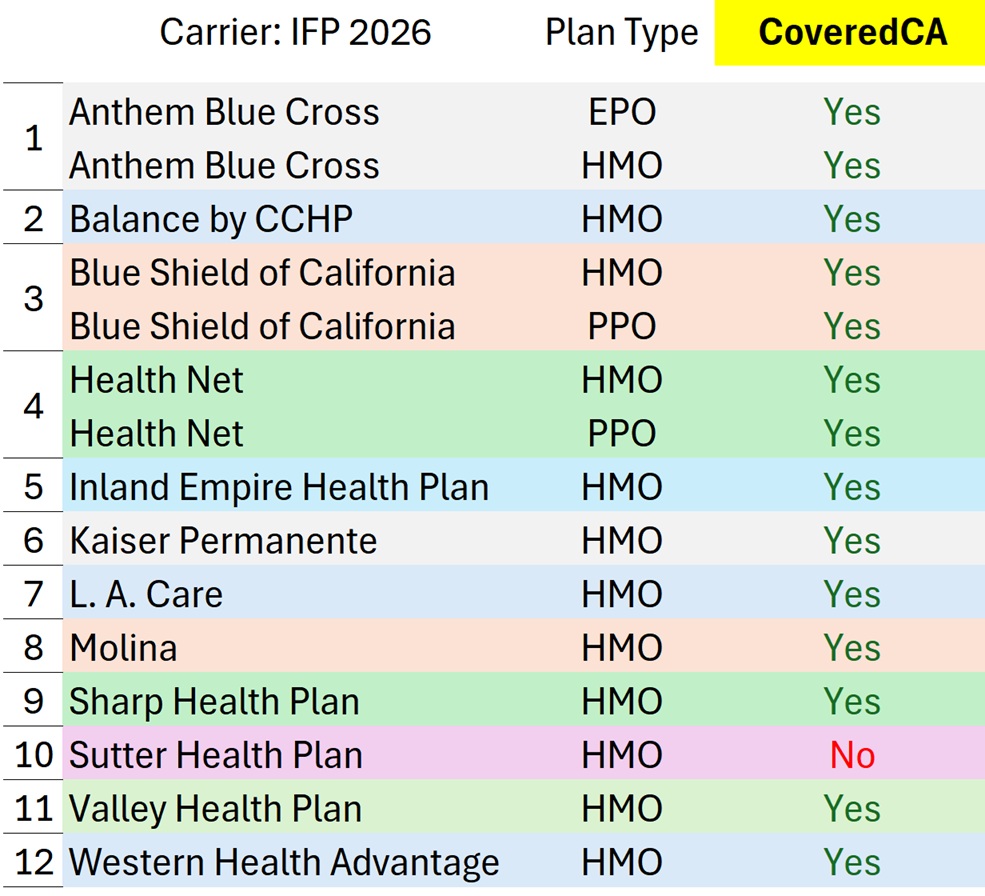

Covered California develops a statewide map showing where all the carriers offer their respective health plans. But you will not find Sutter on there because Sutter does not sell their health plans through Covered California. They are only off-exchange, direct from Sutter.

Sutter Health Plans cover parts of Nevada County down into Stanislaus, over into the East Bay, down to Santa Cruz, up San Francisco, and Sonoma.

Off-Exchange Health Plans

If you are eligible for a health insurance subsidy, you will want to go through Covered California to enroll. If your income is low enough, you may be eligible for the cost-sharing reductions. You can also enroll in all of the plans off-exchange direct from the carrier with no subsidy.

You would want to go off-exchange if you want a Silver 70 plan and you’re never going to be getting a subsidy, because the Silver 70 plans are about 5% less expensive if you go direct to the carrier. The provider networks for these health plans off Exchange are exactly the same as if you went through Covered California, so you don’t have to worry about that.

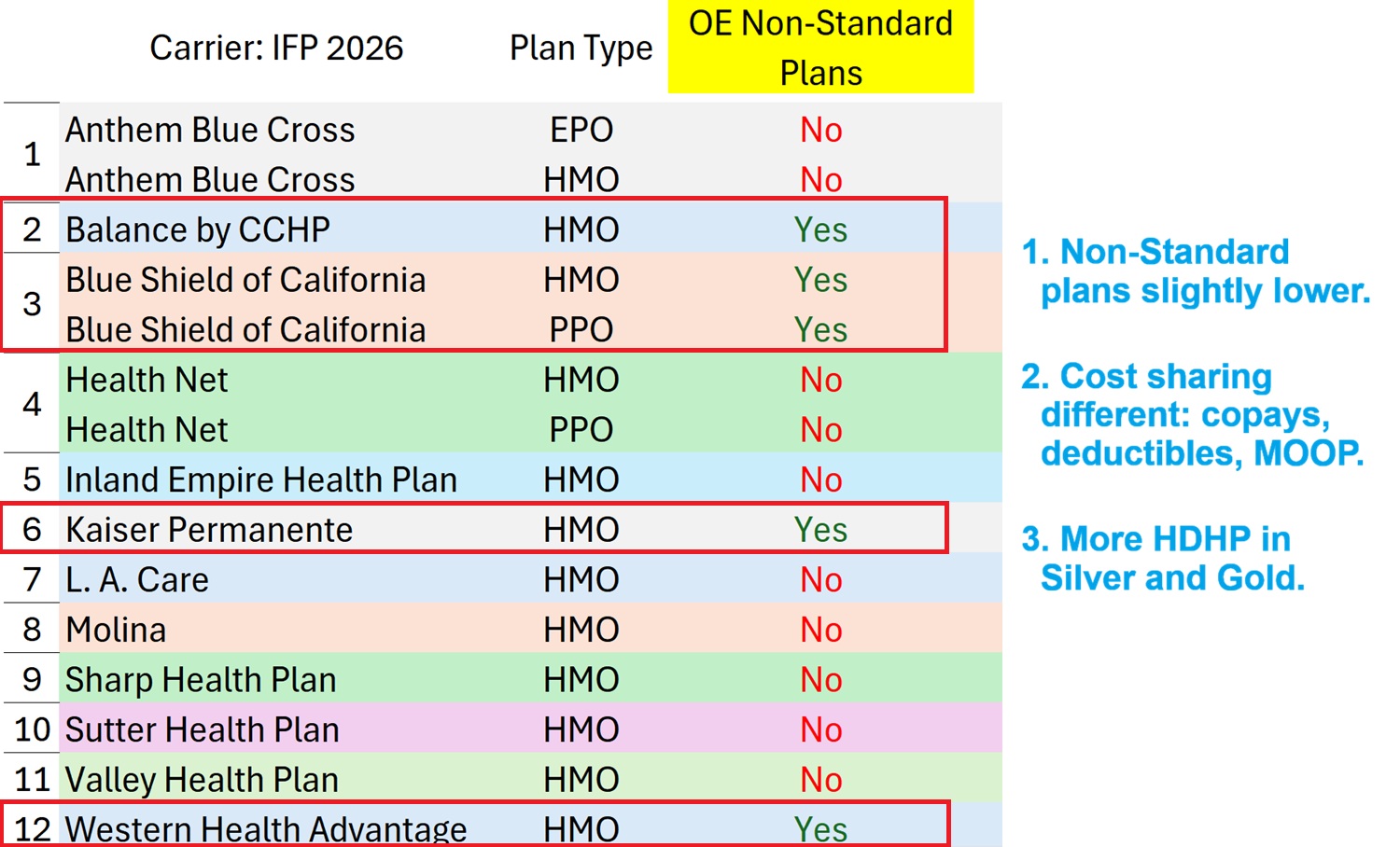

When you go off Exchange, many of the carriers will offer what we call non-standard benefit design plans. Covered California only offers what they call standard benefit design plans, but the carriers can offer non-standard benefit design plans off Exchange, and they can be slightly less expensive than going through Covered California, which may be a benefit if you’re never going to receive a subsidy.

The cost-sharing copays and the deductibles, max amount of pocket may be slightly different. You have to really carefully analyze the plan to make sure that you’re not getting yourself into a pinch and having to pay more for healthcare services or prescription medications with a non-standard benefit plan. They all have the same provider network, whether it’s a standard benefit design plan or non-standard.

Mobile Applications

Virtually all of the carriers will have some sort of mobile application maybe tied to that My Health Online. The medical group app is where you can see upcoming appointments and lab tests and things of that nature. But it isn’t telling you about your actual health plan such as if you are late making the premium payment or you want to change your payment method.

Mobile apps let you see other information about healthcare billing, evidence of billing statements, etc. Carriers with a dedicated health plan mobile app are Anthem Blue Cross, Blue Shield, Health Net of California, Kaiser Permanente and Molina.

Health Plan Ratings

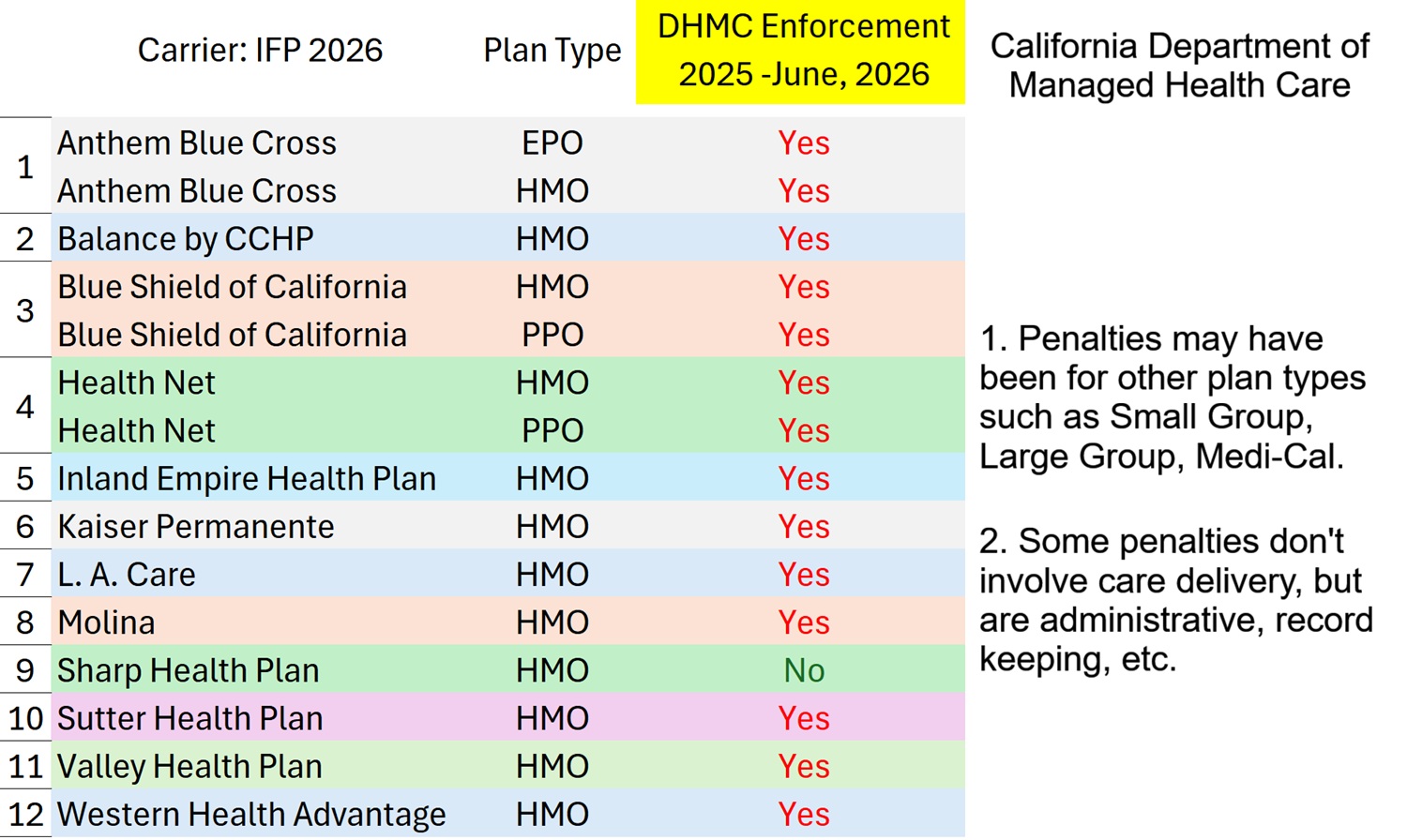

These carriers are regulated by the California Department of Managed Healthcare (DMHC). If there is a problem and they investigate it, the plans can be fined. From January 2025 through June 2026, every carrier had an enforcement action from DMHC except Sharp Health Plan.

Sometimes the enforcement actions aren’t necessarily for individual and family plans. They might be for small groups, large groups, Medi-Cal plans also offer in California. The penalties don’t always involve the delivery of health care. There can be penalties levied surrounding record keeping or customer service. But all of these enforcement actions underscore the complicated regulatory environment that these health plans must operate in from local, state, and federal levels.

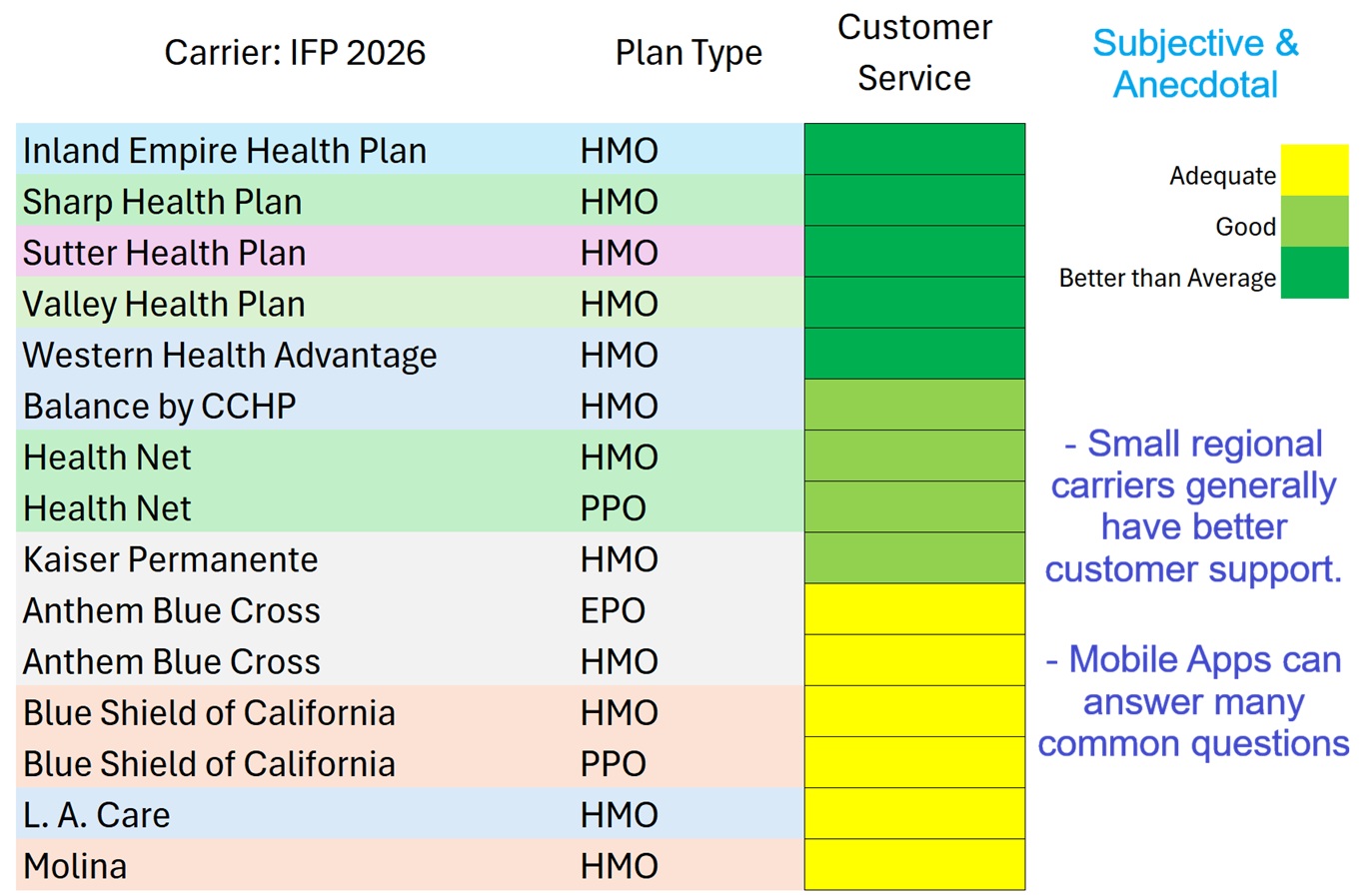

Customer Service

My customer service ratings are subjective based on my interaction with the carriers and reports from clients. What you will notice is that potentially those smaller regional carriers are going to have better than average customer service. Why? They’re smaller. Generally, the customer service staff is in California. It’s not offshored, so you’re usually talking to an individual when you can get through and actually talk to someone.

Health Net, has really improved their customer service over the last couple of years. Kaiser seems to have had some real issues in 2026 and 2025 related to an update to their billing system. Blue Cross and Blue Shield are okay, but a lot of times their customer services is offshored, and that’s where the mobile app can really come in handy.

Online Provider Search Tool

The online provider tools generally are pretty good for HMO plans because you have a very set network. However, just navigating the online system can be very difficult. Issues that complicate and create challenges are carriers that have multiple types of plans. You have to select the correct individual and family network.

Blue Cross and Blue Shield, can be complicated because of their multiple plan offerings like small group, large group, Medi-Cal, etc. The Health Net online provider search tool needs a complete overhaul. It is very complicated and user friendly. You need to make sure you have the correct internet browser to be able to interact with the tool.

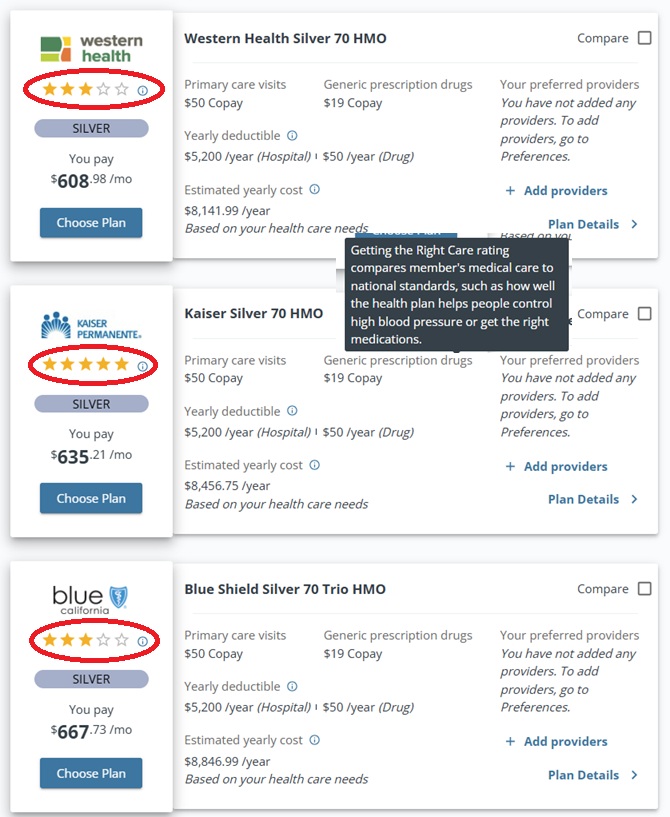

California publishes a health plan report card, but I’m not sure how applicable it is. It seems to aggregate data from all the different products (IFP, small group, Medi-Cal, etc.) not specifically individual and family plans (IFP). In addition, health plans are not delivering healthcare services. Health plans authorize care and they pay claims. Blue Shield doesn’t hire doctors to deliver care to you. I wonder if people are conflating the Kaiser Medical Group from Kaiser Permanente. Kaiser Permanente is the health insurance.

Covered California does put out their own scores. They have a separate survey, different metrics, and methodology. Still, the health plans are not delivering the healthcare service. Covered California is focused on what they hope the health plans are doing such alerting people to vaccinations and the preventative services.

Bottom line, I get the feeling the consumer reports on the health plans have an implicit bias. Sometimes it is difficult for a consumer to set aside their ill feelings to the care they received from the operation of the health plan.

YouTube video on health plan overview.