Can Covered California and the individual and family market survive the repeal of the individual mandate?

There is more than the IRS penalty at stake with the repeal of the individual mandate. When Trump said Obamacare had been repealed with the removal of the individual mandate penalty in the 2017 tax legislation, he was partially correct. It all revolves around the type of insurance that is eligible to satisfy the requirement of having health insurance in order to avoid the individual mandate penalty also known as the Shared Responsibility Payment from the IRS. If enough consumers enroll in alternative health plans not offered through Covered California or off-exchange, the whole market could collapse and Obamacare would be effectively dead.

In order for tax payers to avoid the individual mandate penalty on their federal tax return they must have been enrolled in a health plan that meets minimum essential coverage (MEC). If they cannot prove they had MEC they will be assessed a Shared Responsibility Payment on their federal tax return. Under the 2017 tax reform legislation, the individual mandate will no longer be applicable and the Shared Responsibility Payment will not be assessed for 2019 – unless congress changes the laws between now and then.

Minimum Essential Coverage

Minimum Essential Coverage can be offered in different forms. A Medicare beneficiary enrolled in Parts A and B of Original Medicare has MEC. An employee at a large corporation can be offered MEC health insurance, which is very bare bones, but it satisfies the individual mandate requirement. For low income individuals and families enrolled in expanded Medicaid, Medi-Cal in California, that health insurance meets the requirement.

Qualified Health Plans

But for people, who are too young for Medicare, are not offered employer sponsored health insurance, and make too much money for Medi-Cal, their only alternative are health plans in the individual and family market. If the family’s income is in the right range (between 138% and 400% of the federal poverty level) they can apply for health insurance through Covered California and receive a monthly tax credit. These plans, that have been designed and approved by Covered California, are known as Qualified Health Plans (QHPs), they meet both MEC and qualifications for a health plan to be eligible for the monthly Advance Premium Tax Credits.

These QHPs are also offered off-exchange directly from the health insurance company at the exact same rates with no tax credits. In addition, many health insurance companies offer alternative MEC health plans off-exchange. These plans have all the mandated elements for health insurance to meet the ACA requirements for MEC and are actuarially equivalent to plans offered through Covered California. (The off-exchange Blue Shield Silver 1850 is actuarially equivalent to the standard benefit design QHP Silver 70 through Covered California.)

Repealing Individual Mandate Could Collapse Covered California

One of the reasons health insurance has become so expensive is the list of benefits and certain rules that must be included in the QHPs. Some of these benefits are mandated by the ACA and others are enhancements added by Covered California. For example, the ACA says QHPs can’t discriminate based on pre-existing conditions and the rates for a 64 year old person can be no more than 3 times a 21 year old individual. Covered California has also included additional prescription drug benefits that cap the cost of expensive drugs on a monthly basis.

The QHPs offered by Covered California are good, but expensive. Without the monthly tax credits most people of modest incomes can’t afford the expensive rates. The off-exchange actuarially equivalent health plans are usually less expensive than the standard Covered California metal tier level plans but still pricey for many people.

The question that arises is why don’t the health insurance companies offer health plans without all the ACA requirements and California enhancements that drive up the rates? The short answer is that the health insurance companies that participate in Covered California have also agreed to sell plans with all the same benefits as the QHPs off-exchange.

The language of the contract between the health plans (contractors) and Covered California would seem to preclude the health insurance companies from offering plans that were substantially different than the QHPs at significantly lower rates.

COVERED CALIFORNIA QUALIFIED HEALTH PLAN ISSUER CONTRACT FOR 2017 – 2019

3.2.3 Offerings Outside of the Exchange

a) Contractor acknowledges and agrees that as required under State and Federal law, QHPs and substantially similar plans offered by Contractor outside the Exchange must be offered at the same rate whether offered inside the Exchange or outside the Exchange directly from the issuer or through an Agent.

b) In the event that Contractor sells products outside the Exchange, Contractor shall fairly and affirmatively offer, market and sell all products made available to individuals and small businesses in the Exchange to individuals and small businesses seeking coverage outside the Exchange consistent with California law.

I could find nothing in the Covered California contract that strictly prohibits the health insurance companies from offering non-QHPs to the public that would not satisfy the individual mandate. However, health insurance companies run the risk of being kicked-off the exchange if for some reason Covered California doesn’t like their business model, plans, or practices. In other words, Covered California is not going to allow a carrier to offer plans off-exchange that don’t meet their standards at lower rates and that might siphon away their enrollments.

Because Covered California can deliver significant enrollments to the participating carriers, there is little incentive to offer only plans off-exchange. Both Assurant and Cigna had offered only off-exchange plans in California, foregoing participation in the exchange. Both of these carriers have discontinued selling individual and family plans in California.

Health Plans May Exit Individual and Family Market

The only health insurance-type products that we have seen marketed outside of the QHPs are the health sharing ministry and short term medical plans. Under certain circumstances, enrollment in a health care sharing ministry can satisfy the individual mandate requirements. But health care sharing ministries are not technically insurance and are therefore not regulated by the state as such. Short term medical plans also don’t qualify to avoid the individual mandate for 2018. Consequently, enrollments in both of these types of health care products have been limited and have not posed a threat to the individual and family market. But that could soon change if the individual mandate truly is lifted.

Association Plans

There is yet another threat to the QHP market with the proposed introduction of association plans. With the introduction of the ACA, association plans where self-employed people could join health plans targeted to their occupation like farmers and real estate agents, were essentially shut down. The Trump administration is working on new rules that would allow association plans to be reintroduced into the market place for 2019. Without the need to offer health insurance to satisfy the individual mandate, these association plans, like short term medical plans, could be much less expensive than the QHPs offered by Covered California.

The U.S. Department of Labor has released the proposed rules for the small group association plans. Read more at: Labor Department Proposed Rules For Small Group Association Health Insurance

Short Term Medical Plans

Already in the market place are short term medical plans that do not meet the QHP or MEC requirements. These plans are meant to bridge the gap between the termination of one heath plan and when a new one becomes effective. This happens when a person might lose their group health plan and the individual and family plan may not start for a couple of months. Short term medical plans don’t cover pre-existing conditions, there is limited prescription drug coverage, and there is usually a cap on how much the health plan will pay toward medical expenses. Because of these restrictions short term medical plans don’t meet the criteria for a QHP or MEC to avoid the current individual mandate.

The Obama administration had limited the enrollment period of short term medical plans to a maximum of 90 days. The Trump administration is working to overturn that rule and let people enroll in short term medical plans for 12 months. To be clear, enrolling in short term medical insurance will not alleviate the Shared Responsibility Payment of the individual mandate for 2018.

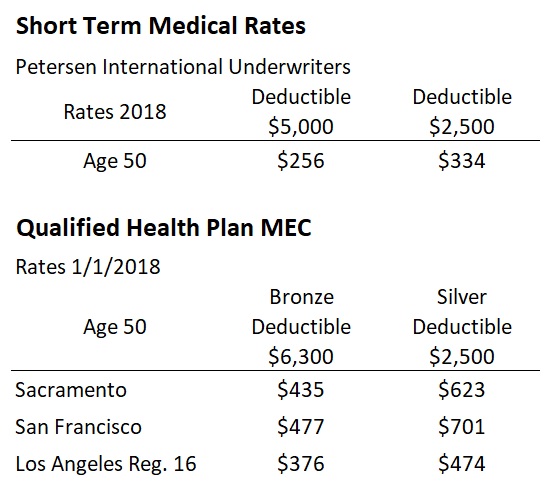

You can’t honestly compare short term medical plans to qualified health plans because of the numerous differences in benefits and coverage. Some people believe that short term medical plans are horribly inadequate. Conversely, others will argue that QHPs are over stuffed with benefits that few people use making them very expensive. The bottom line for many people is the monthly cost. If you are over 50 years old and earning more than $50,000, which make you ineligible for the Covered California tax credits, then the rates of the short term medical plans are really attractive. This makes short term medical plans an attractive substitute to QHPs offered through Covered California or off-exchange.

A 50 year old person can save over 50% on the monthly rate by enrolling in a short term medical plan versus a QHP. Of course, people need to carefully review the limits and conditions of short term medical plans. But from the number of people I’ve talked to during open enrollment for 2018, there is a sizable percentage who would ditch the QHP in favor of the short term plans if the individual mandate was not an issue. The rational is that the $3,000 to $5,000 savings per year with a cheaper short term plan means the consumer can pay for medications or doctors who might not be covered under the short term medical plan. It’s a trade-off some consumers are willing to accept in order to save thousands of dollars per year.

2018 short term medical rates versus the least expensive Bronze and Silver plans by region for a 50 year old individual.

The existence of short term medical plans with enrollments up to 12 months coupled with the repeal of the individual mandate will surely eat into Covered California enrollment. People will consider the short term medical plans even if they are receiving the monthly tax credit subsidy from Covered California. As long as the short term medical plans are slightly less expensive, there will be consumers who leave Covered California and the perceived intrusive bureaucracy of qualifying for the subsidy.

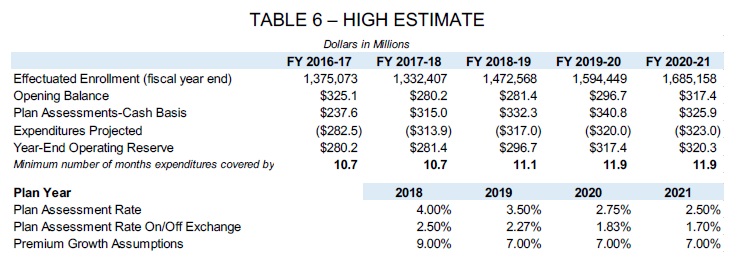

Covered California has developed a high estimate for enrollments in their individual and family plans of 1.47 million individuals for fiscal year 2018-19. They estimate that those enrollments will generate $332 million dollars based on 4% commission fee for 2018, dropping to 3.5% in 2019. The fee is assessed on the full amount of the premium rate, not on what the consumer pays monthly, and is paid by the health plan. The impact on the consumers leaving Covered California isn’t so much the total number, as the premium value is represents. The consumer most likely to leave the exchange is the older person subject to high health insurance rates.

Covered California budget high estimate of enrollments with assessment rate percentages.

If a 50 year old in Sacramento with a Bronze plan opts for a short term medical plan, based on 2018 rates, Covered California will lose $17.40 per month ($435 x 4%) or $208.80 per year. The rates for a person over 60 in a Bronze can easily be $700 to $900 per month. Losing just one of these individuals is like losing the revenue for 3 young adults for Covered California.

According to Covered California’s September 2017 enrollment data, over 50% of their membership were over the age of 45. Approximately 17%, or 56,900, of those consumers were not subsidy eligible and were therefore paying the full premiums for their health insurance. This is the group who is looking for less expensive health insurance and could potentially drift away from Covered California and the QHPs.

However, Covered California is in good financial shape. If they see a significant drop in enrollments they can easily adjust their budget. How? One third of their 2017-18 budget, $111 million, was dedicated to marketing for the 2018 open enrollment period. Covered California could cut the marketing budget in half and still be spending 5 times more than the federal government spends on Healthcare.gov.

But it’s not just Covered California who stands to lose enrollment, the carriers will see declining membership as well in both on- and off-exchange plans. Any loss of individual enrollment in the QHPs will shrink the pool of all healthy adults in those health plans. This threatens to destabilize the entire market. This destabilization is the bigger threat to the market for QHPs.

While the threat of significant erosion to enrollments through Covered California is real, the greater problem is the overall stability of the individual and family plan (IFP) market. The addition of association plans, expanded short term medical plans, along with removing the individual mandate adds tremendous uncertainty for the current carriers. Even before any of these threats surfaced, Anthem Blue Cross pulled out of most of the IFP regions in California for 2018 citing uncertainty in the market place.

A stable insurance market is dependent on products that create value for consumers through the broad spreading of risk and a known set of conditions upon which rates can be developed. Today, planning and pricing for ACA-compliant health plans has become increasingly difficult due to shrinking individual market as well as continual changes in federal operations, rules and guidance. – Anthem adjusts Individual health plan offerings in California for 2018

Covered California Preparing For Chaos

Covered California has recognized this existential threat to the market in a December 20, 2017 document addressing state-based high risk pools or reinsurance issues.

It is highly likely that in the absence of strong mitigating policies, such as well funded and properly implemented state-based invisible high risk pools or reinsurance, many states will have no carriers willing to participate in the individual market in some counties or will face very substantial premium increases in 2019. The reasons for the impending individual market challenges include: (1) the removal of the “individual mandate” penalty; (2) uncertainty for insurance carriers related to potential changes in the individual market resulting from the forthcoming Executive Order; and, (3) for federal marketplace states, lower enrollment in 2018 and the prospect of continued underinvestment in marketing.

In his Executive Director’s Report to the Covered California Board on December 7, 2017, Peter Lee noted certain federal actions were causing uncertainty and instability in the market. Points 4 and 5 of his presentation to the board directly address issues undermining the IFP market.

4. Uncertainty among carriers about federal enforcement of individual shared responsibility penalty.

- Potential consequence: significant coverage losses and exodus of carriers from individual market if replacement policy is not enacted.

- Mitigations in California: added a provision to contracts with qualified health plans to allow multiyear adjustments to their margins. Additional mitigations, to be determined.

5. Executive order on new individual market products (association health plan and short-term limited duration insurance plans).

- Potential consequence: potential harm to risk pool by “siphoning off” good risk; return of low-value “gotcha” coverage.

- Mitigations in California: to be determined.

The mitigations alluded to are legislative actions that might impose a California individual mandate or not allowing the sale of certain types of short term medical or association plans. Because states regulate their own insurance market place, California can pass legislation that would prop up the individual and family market place by reducing alternatives. But without significant reform for carriers to recoup losses or offer health plans with fewer benefits, the rates are likely to remain high and go higher. And it is the increasingly high health insurance rates that are forcing people to look at short term medical plans or drop health insurance altogether.

The real looming threat is the loss of health plans participating in the IFP market. In 2017 three carriers dominated the market with 72% of the enrollments: Anthem Blue Cross 19%, Blue Shield 25%, Kaiser 28%. With the loss of Blue Cross in the major metropolitan markets such as the Bay Area and Southern California, two carriers, Blue Shield and Kaiser, are likely to command over 60% of the market place in 2018. If one of those two carriers determines that offering IFP plans is just too risky in 2018, it could lead to other carriers such as Health Net, Molina, or Oscar also pulling out of the market.

In a sense, the individual and family plan market would collapse in California if health plans started closing their plans for 2019 enrollments. Even the smaller regional carriers like Chinese Community Health Plan, Western Health Advantage, and Sharp might bolt the market place fearing an influx of health challenged consumers. Some counties may be left with no carriers offering any health plans. This would drive people to enroll in short term medical plans, health sharing ministry plans, or association plans if they have not been banned. This would be the proverbial death spiral for the market.

Most likely we would see a surge in small employer group plans if health insurance in the individual and family plan market place is severely diminished. But there would still be hundreds of thousands of families without any viable health insurance option available to them through Covered California with the tax credit subsidy to make the health insurance affordable. Covered California may be reduced to offering subsidized plans only in regions where the population of subsidy eligible households is great enough to support offering a health plan.

We have to remember that most of the carriers are involved in other markets such as small groups, large employer groups, Medi-Cal, and Medicare health plans. Most can survive without offering individual and family plans. I doubt that Blue Shield or Kaiser want to see their IFP business evaporate. But I’m also certain that no responsible carrier would decide to continue offering individual and family health plans if it meant hundreds of millions of dollars in losses.

Healthy people paying for health insurance is the corner stone upon which health plans can offer coverage to people with chronic health challenges. But it is also the healthy individuals who have a smaller tolerance for high health insurance premiums because they see a diminishing utility for the health plan they are paying for. In other words, they can’t see paying high rates for health insurance they never use, even if there is a tacit acknowledgement that a major illness or accident could strike at any time.

At the beginning of 2017 it was inconceivable to me that there would be a set of circumstances that so threatened the existence of Covered California. Now it looks like there is a series of circumstances that could seriously jeopardize not only Covered California, but the entire individual and family market place. The individual and family market place is fragile. It will only take a few small market changes to dramatically shift the demand for QHPs. If the demand shift is great enough through consumers selecting non-QHP association or short term medical plans, the entire market place for ACA compliant health plans could collapse.

December

Proposed Association Health Plan Rules 2017-28103

Proposed rules for association health plans from the U.S. Department of Labor.