New IRS rules will allow some family members to enroll in an employer sponsored health plan and other family members, such as a spouse or children, to enroll through an ACA market place health insurance exchange and receive the health insurance subsidies for 2023. These new rules override the problem where a spouse or dependents were ineligible for health plan subsidies because a spouse or parent was offered employer health insurance.[1]

Fixing the Family Glitch; Allowing Employer Coverage with ACA Health Plan Subsidies

Certain conditions and tests must be met in order for the spouse and dependents to enroll in an ACA subsidized health offered through an exchange such as Healthcare.gov or Covered California health plan with the subsidies, while the other parent keeps the employer sponsored health plan.

1. The employer plan must meet minimum value standard, where the plan design is meant to cover 60 percent of the medical services for the standard population. Most employer plans meet the minimum value standard.

2. The family is based on the tax household. This would be the primary tax filer, spouse, and any dependents listed on the federal tax return.

3.The employee offered health insurance is considered separately from the rest of the tax family for affordability. If the health insurance premium for the employee, after the employer contribution, is less than 9.12 percent of the household income (2023), the employee family member is ineligible for the ACA subsidies.

4. If the total premiums for the tax family members offered by the employer plan are greater than 9.12 percent of the household income[2], the spouse and dependents can enroll through Covered California and receive the subsidies.

5. The health insurance premiums are based on the lowest cost health plan offered to the employee and family members, not necessarily the health plan the employee has chosen.

Calculating Health Insurance Affordability for 2023

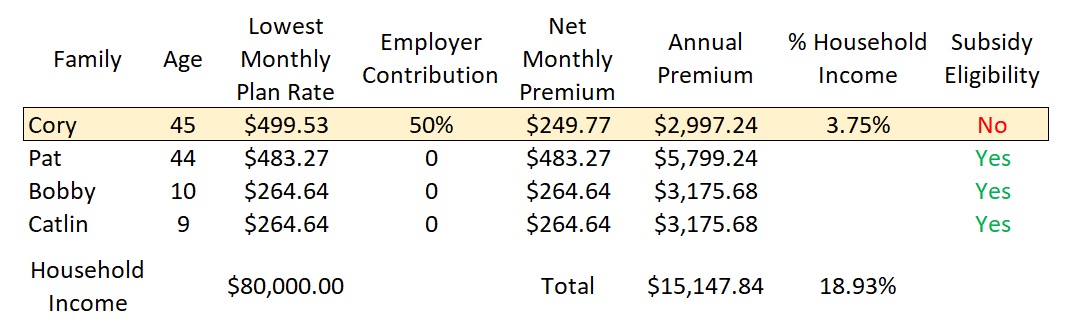

We have a family of 4, two adults and two children. Cory is offered employer sponsored health insurance and it is also offered to the spouse and children. Cory’s employer contributes 50 percent of the health insurance to the employee only. The employer contributes nothing to the spouse or dependents.

The lowest cost health plan offered to Cory (not necessarily the one selected) has a monthly rate of $499.53. After the employer contribution of 50 percent, Cory would have $249.77 deducted from his pay check just for his health insurance. The monthly premium for the lowest cost health plan offered to Cory’s spouse, Pat, has a monthly premium of $483.27. The two children, Bobby and Catlin, are offered health insurance at $264.64 each for that lowest cost health plan. The employer makes no contribution to spouse or dependents.

The annual household income is estimated to be $80,000. Cory’s employee health insurance premium as a percentage of the household income is 3.75 percent. Because the percentage is below the affordability percentage of 9.12 percent, Cory is not eligible for a market place ACA health plan with the subsidies.

The total annual premiums for the entire household are used for the affordability test for the other household members. (This calculation can be made on a monthly basis as well.) The total annual premiums for everyone offered the lowest cost health insurance is $15,147.84 That annual premium is 18.93 percent of the $80,000 estimated household income. Because the health insurance expense percentage is greater than 9.12 percent, it is deemed unaffordable, Pat, Bobby, and Catlin can enroll in a market place ACA health plan with the subsidies.

When Pat, Bobby, and Catlin enroll in the market place (such as Covered California or Healthcare.gov) for the ACA subsidies they will be subject to any Medicaid income thresholds. If the household income is less than 266 percent of the federal poverty level for a family of four, in California, the children would be deemed Medi-Cal and ineligible for subsidies.

On a Center for Medicare and Medicaid Services presentation of the new family affordability rule, the IRS stated that there are safe harbor provisions for a household’s estimated income. In other words, if the market place exchange verifies the household at the time of enrollment, but the income subsequently increases, making the family health insurance premiums less than 9.12 percent of the household income, the primary tax payer will not have to repay all of the subsidies. However, if there were excess subsidies paid during the year, based on the final higher MAGI income, those excess Advance Premium Tax Credits would have to be repaid.

The health insurance premiums for adult children, under 26 years old, that are on the employer health plan, but not in the primary tax filer’s household, are NOT included in the family annual premium calculation. Under certain conditions, when a employer group renews and becomes unaffordable to family members, that may trigger a Special Enrollment Period to enroll in a market place exchange plan with the subsidies. In general, the new affordability rules do not apply to ICHRA or QSEHRA health plan offerings.

The health insurance market places operate under different rules than some of the other government programs. Some of the program rules can come into conflict. We routinely see instances where Covered California determines an individual eligible for Medi-Cal, but the county Medi-Cal department finds the person is not eligible for coverage. The person is left in limbo until Covered California and Medi-Cal can iron out the differences and allow the individual to either enroll in private health plan with the subsidies or Medi-Cal HMO plan.

Gathering Information For Health Insurance Affordability Calculations

To determine if you or your family qualify for the combination of employer coverage and ACA subsidies, you need to gather important information.

- Confirm that the employer plan offered meets the minimum value standard.

- Find the premium rates for the lowest cost employer plan offered.

- Learn the employer contribution to the health insurance for the employee, spouse, and dependents.

- Develop an accurate estimate of your annual income.

- Apply through the market place exchange such as Healthcare.gov or Covered California.

There are a lot of questions and different scenarios that still need to be addressed. The market place exchanges, such as Covered California, are working to put together guidance to address multiple questions and scenarios. But as we enter the Open Enrollment Period for 2023, many families may be able to take advantage of the new rules.

[1] Information presented is based on Center for Medicare and Medicaid Services guidance and the final rule published in the federal register.

[2] The affordability percent is set by the IRS and can change every year.