The monthly health insurance premiums for Covered California members may not increase in 2026. Even though some health plans had double digit rate increases, Covered California members are somewhat insulated because of the way the subsidies are calculated. The unknown is if Republicans in Congress will renew Biden’s enhanced subsidy curve or let it lapse for 2026.

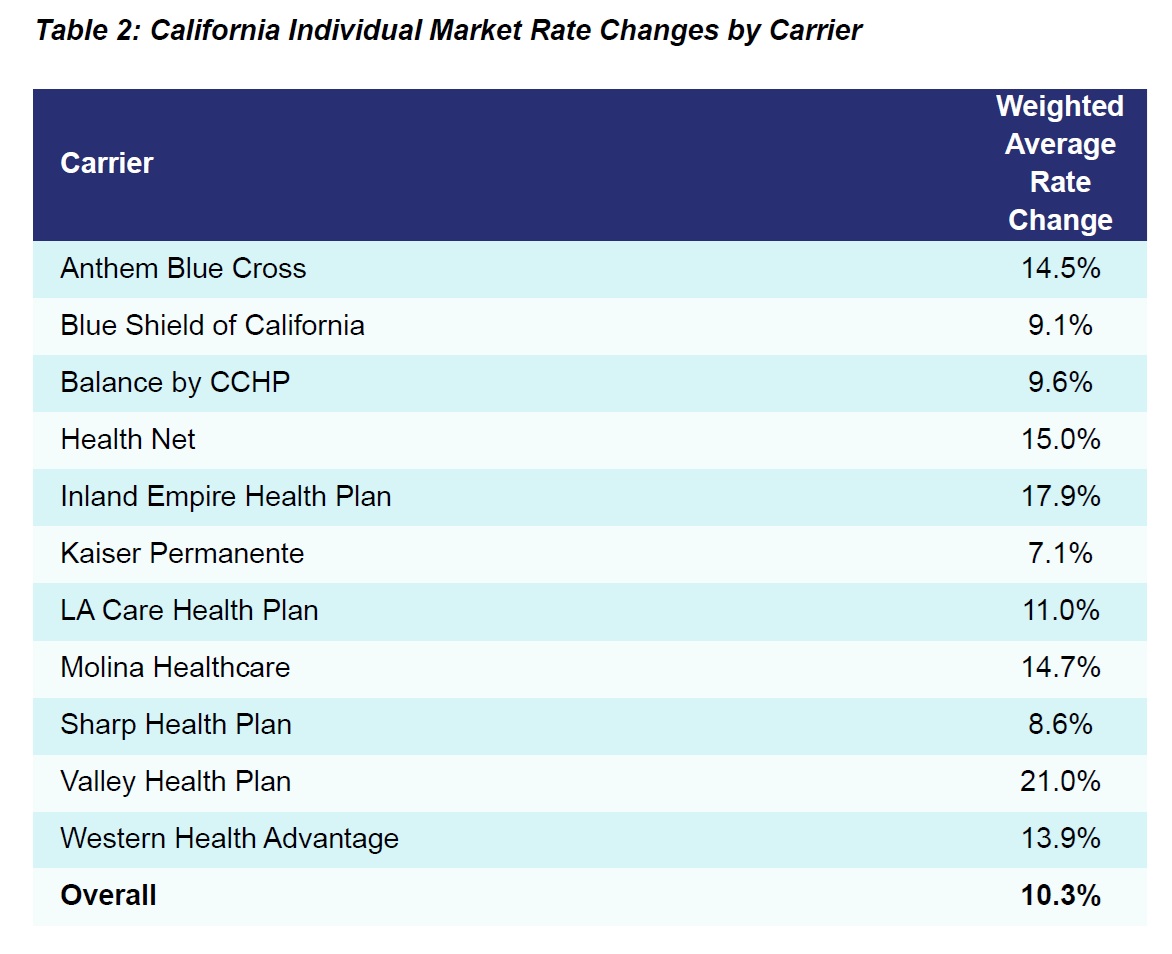

In July, Covered California released approximate health insurance rate increases for 2026 by carrier. The overall increase in 10.3 percent across California. However, unless you receive no subsidy, the final monthly premium increase could be lower or higher than the average.

2026 Health Insurance Rate Increases for Covered California

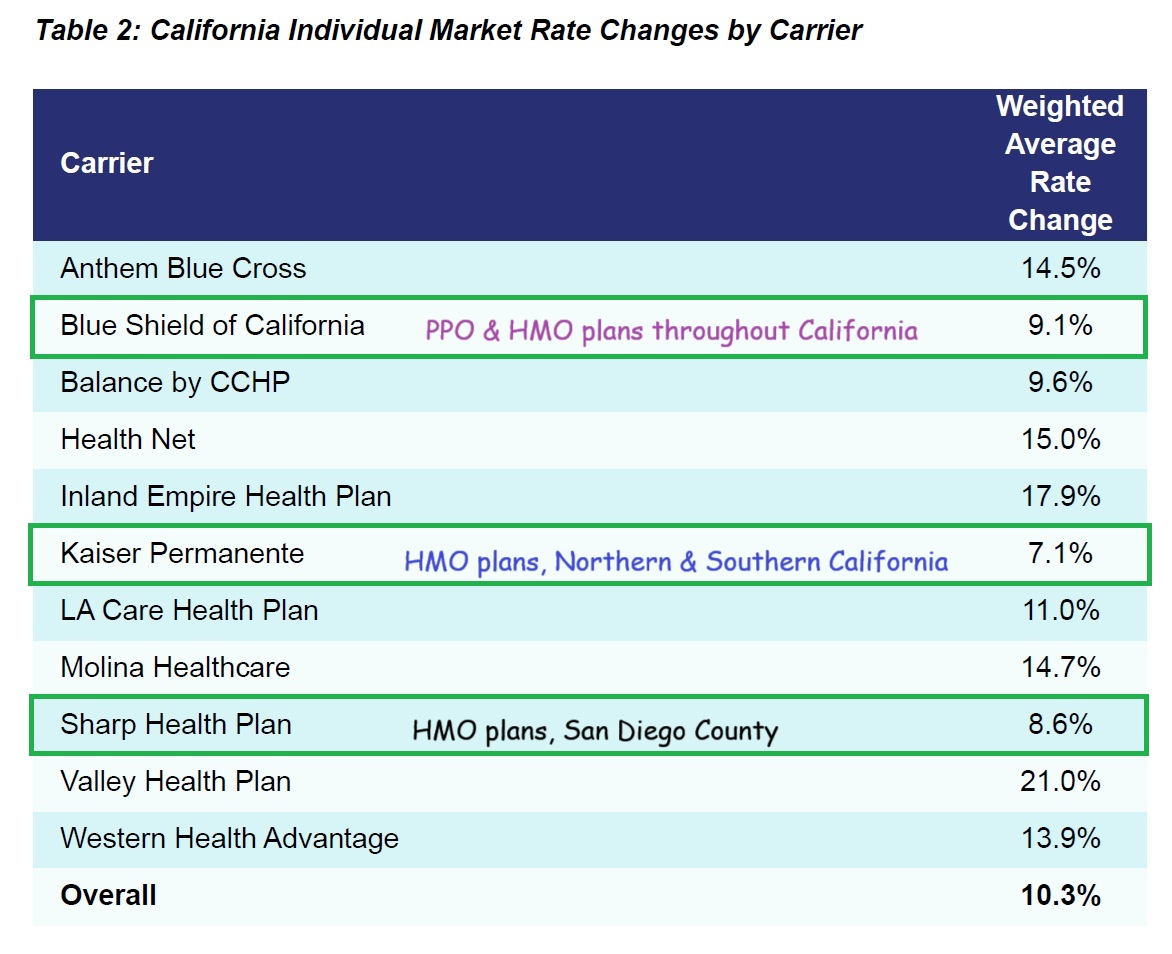

Several carriers have rate increases less than the average. The stated percentage increase is a weighted average because some carriers offer multiple types of plans in various regions. Blue Shield of California, with an average increase of 9.1 percent, offers both PPO and HMO plans, both have different rates throughout California. Kaiser Permanente, with the smallest average rate increase of 7.1 percent, has different rates schedules between Northern and Southern California. Sharp Health Plan, reporting a 8.6 percent increase, only offers plans in San Diego County, but they have two different plan networks, clouding the actual rate increase.

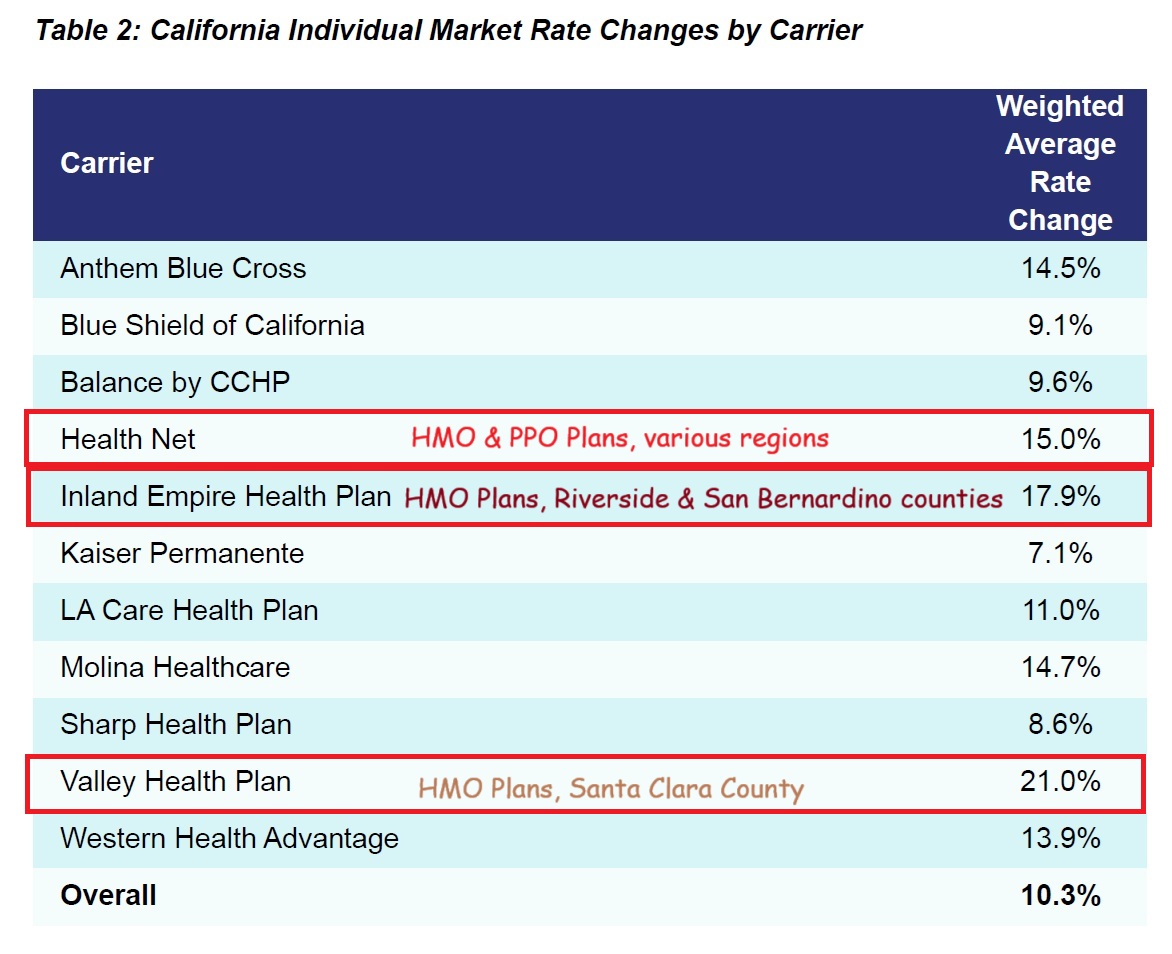

Health plans with the largest weighted rate increase are Health Net at 15%, Inland Empire Health Plan with 17.9%, and Valley Health Plan notching a 21% increase. In general, HMO plans tend to be less expensive than PPO plans. We don’t know if the Health Net rate increase is biased on the HMO or PPO plans. Inland Empire and Valley Health Plan were usually the least expensive Silver plan in their regions. Consequently, they may have greater enrollment in 2025 has individuals transitioned from Medi-Cal to Covered California.

The rate increases are only part of the story. The Covered California subsidy is calculated based on making the second lowest cost Silver plan (SLCSP) offered to you no more than a certain percentage of your household income. This calculation – even with rate increases – can actually lower your premium year over year.

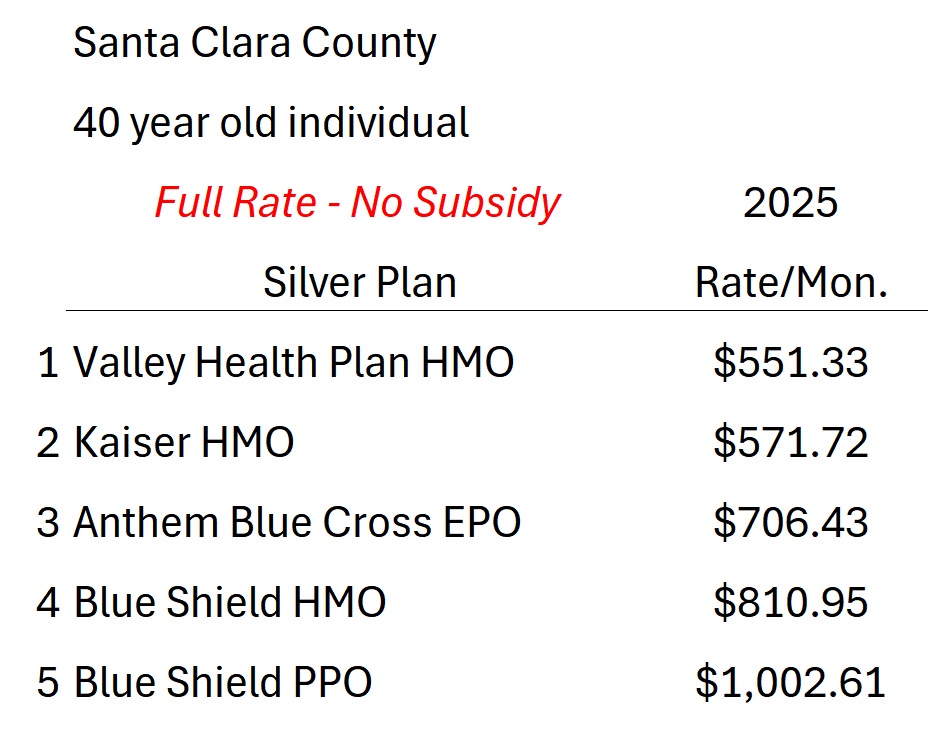

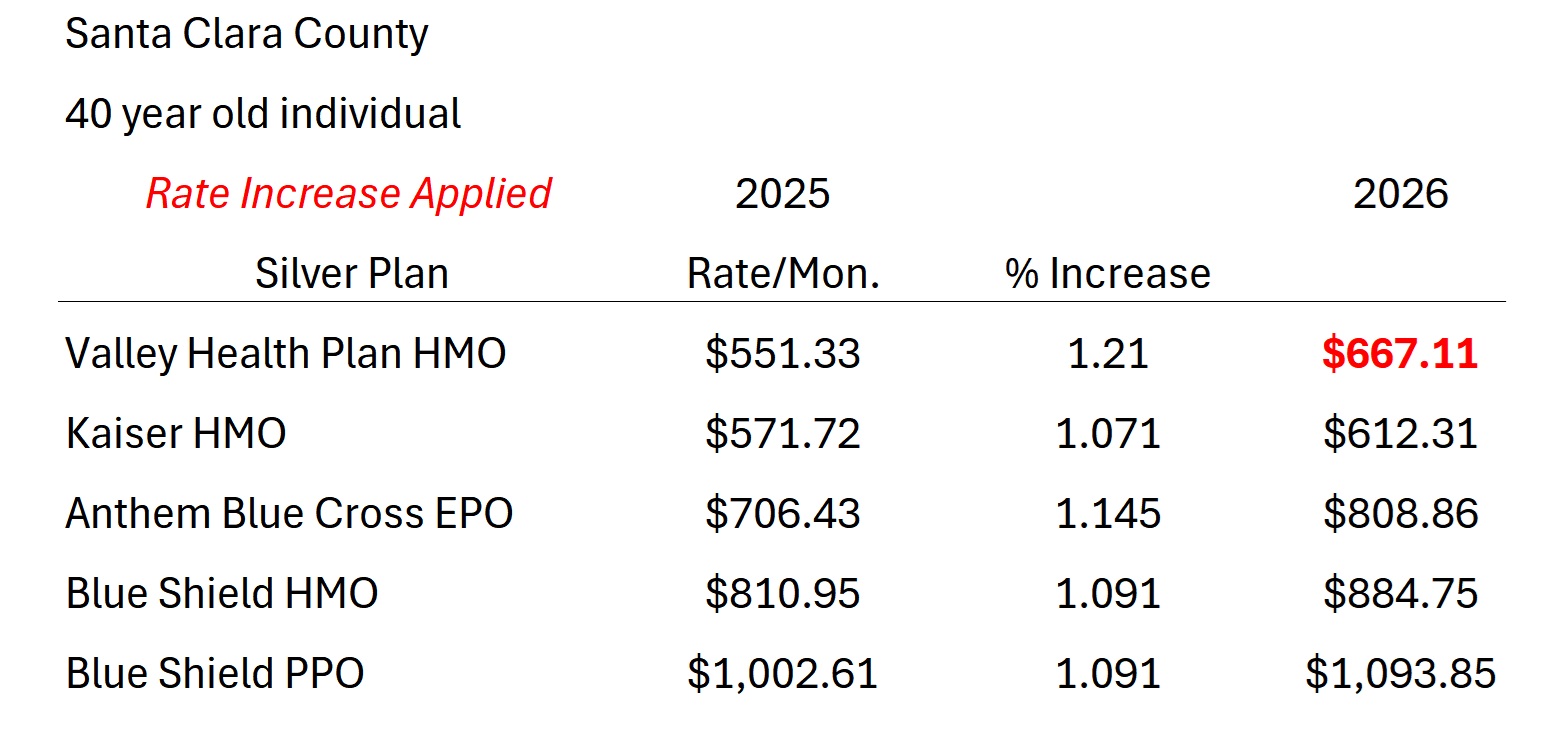

Let’s look at Santa Clara County where Valley Health Plan (VHP) offers their HMO plans. In 2025, for a 40-year-old individual, VHP was the least expensive Silver plan at $551.33, full rate, no subsidy. Kaiser was the SLCSP at $571.72.

Second Lowest Cost Silver Plan

Now, let’s apply the approximate rate increases to the Silver health plans to see what the 2026 rates might look like. With a 21 percent increase, VHP will have a $667.11 monthly premium for a 40-year-old. Kaiser, with a modest increase of 7.1 percent, will have premium of $612.31 for their Silver plan.

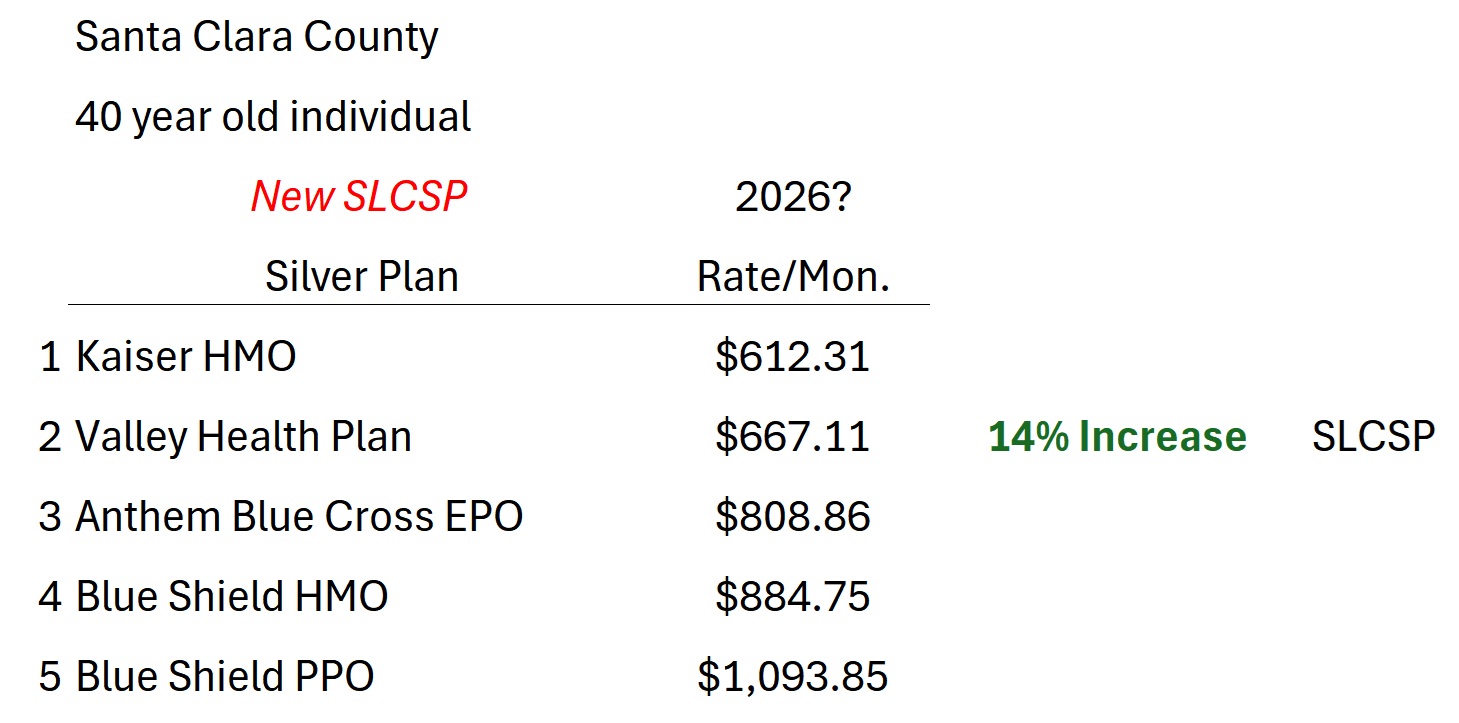

What is significant is the large rate increase of VHP. They displace Kaiser as the SLCSP. Kaiser becomes the least expensive Silver plan. The increase from the 2025 SLCSP to the 2026 SLCSP is 14 percent. This is significant because that means the subsidy will increase 14 percent. If your plan only increased 10 percent, you will receive more subsidy and potentially lower monthly premium, all things being equal.

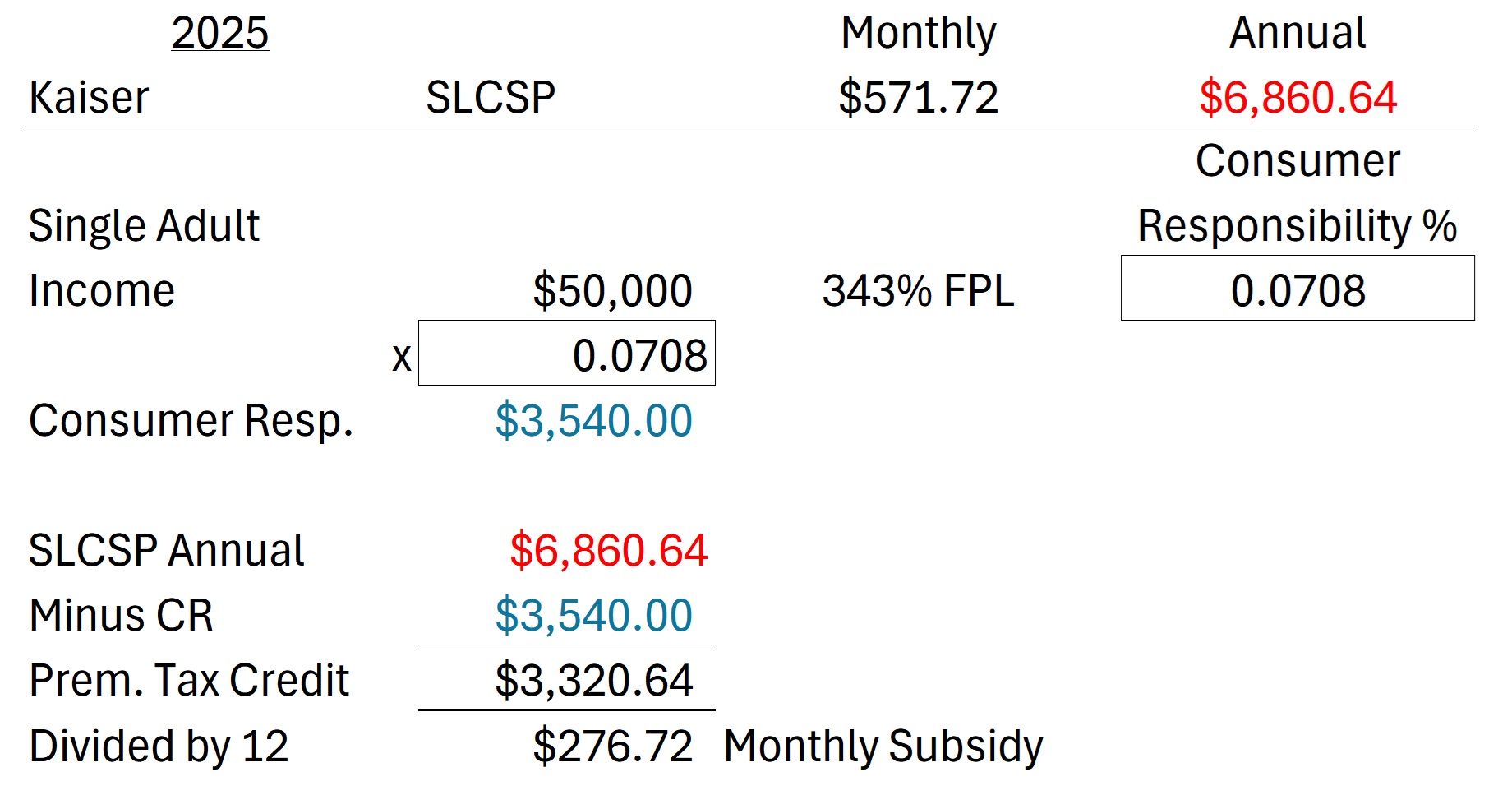

Here is a condensed calculation of subsidy for a 40 year old individual in Santa Clara County with an estimated income of $50,000. For 2025, Kaiser was the SLCSP with an annual full premium of $6,860.64. From the IRS publication Instructions for form 8962 Premium Tax Credit reconciliation, we know that $50,000 is 343 percent of the federal poverty level*. The applicable rate is .0708. In other words, the consumer responsibility for the SLCSP is 7.08 percent*. (*Consumer Responsibility from 2024 IRS form 8962 instructions.)

When the $50,000 income is multiplied by 7.08 percent, the consumer responsibility is determined to be $3,540 annually. We subtract the consumer responsibility from the annual premium for the SLCSP to get the annual Premium Tax Credit subsidy. On a monthly basis, the individual is eligible for a subsidy of $276.72 in 2025 to apply to any metal tier health plan offered.

Santa Clara County Subsidy Increase

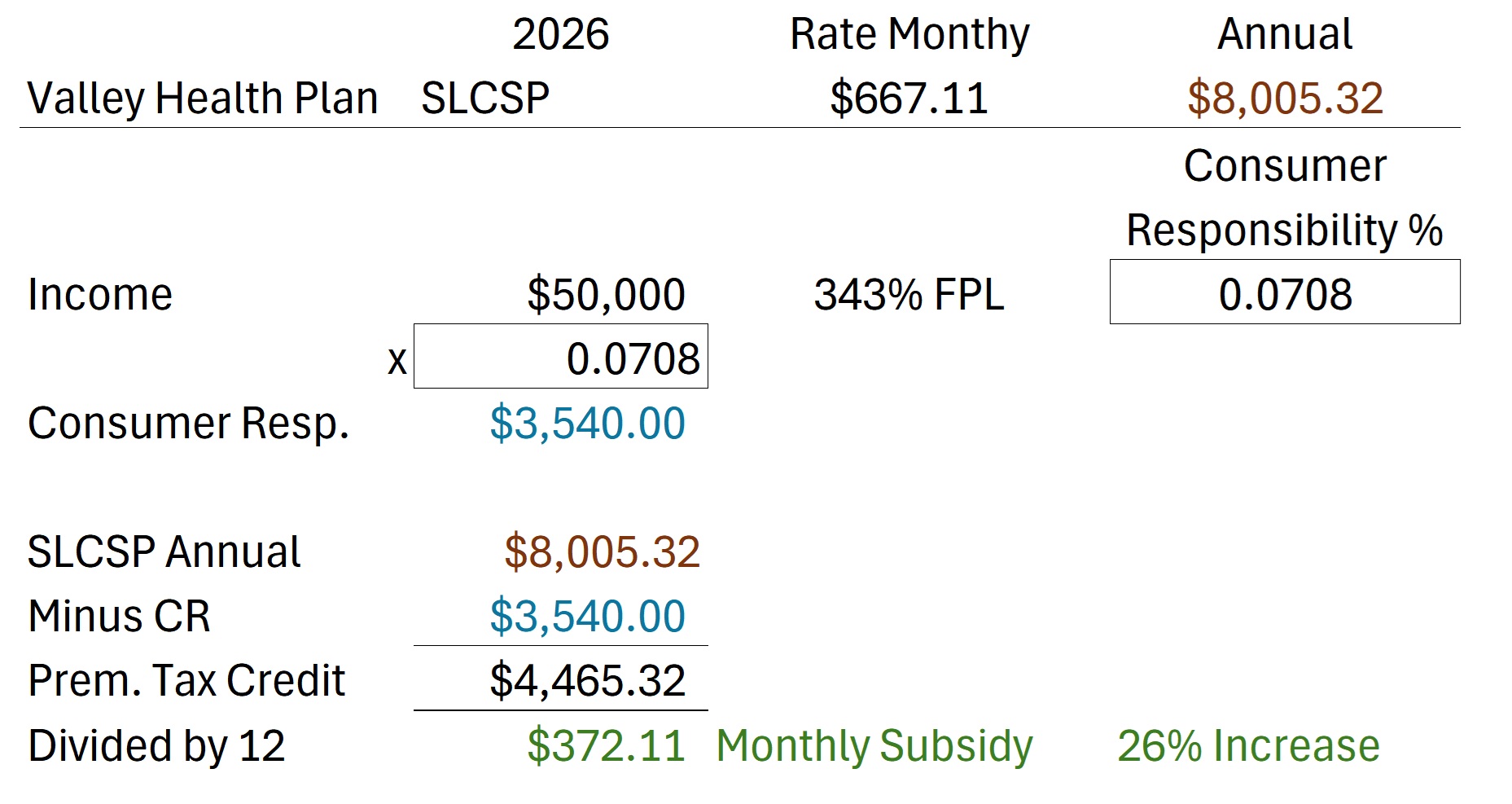

For 2026, if VHP becomes the SLCSP, the subsidy will increase. The annual premium for the VHP will be $8,005.32. The income and consumer responsibility stays the same in this scenario. When we subtract the annual consumer responsibility amount from the VHP annual premium, we are left with a Premium Tax Credit subsidy of $4,465.

Because the SLCSP increased 14 percent, the subsidy for this individual increased from $277 to $372 per month. This represents a 26 percent increase in the monthly subsidy to apply to any metal tier health plan offered. The increased subsidy applies to ALL consumers in Santa Clara County, for any health plan and any metal tier level.

Will Republicans Allow Enhanced Subsidies to Die?

The previous calculations assume that Biden’s Inflation Reduction Act Affordable Care Act subsidy curve remain for 2026. Unfortunately, the odds are long that the Republicans in Congress will extend the enhanced subsidies. Covered California has been messaging consumers preparing them for a reduction in subsidies and corresponding increase in monthly premiums.

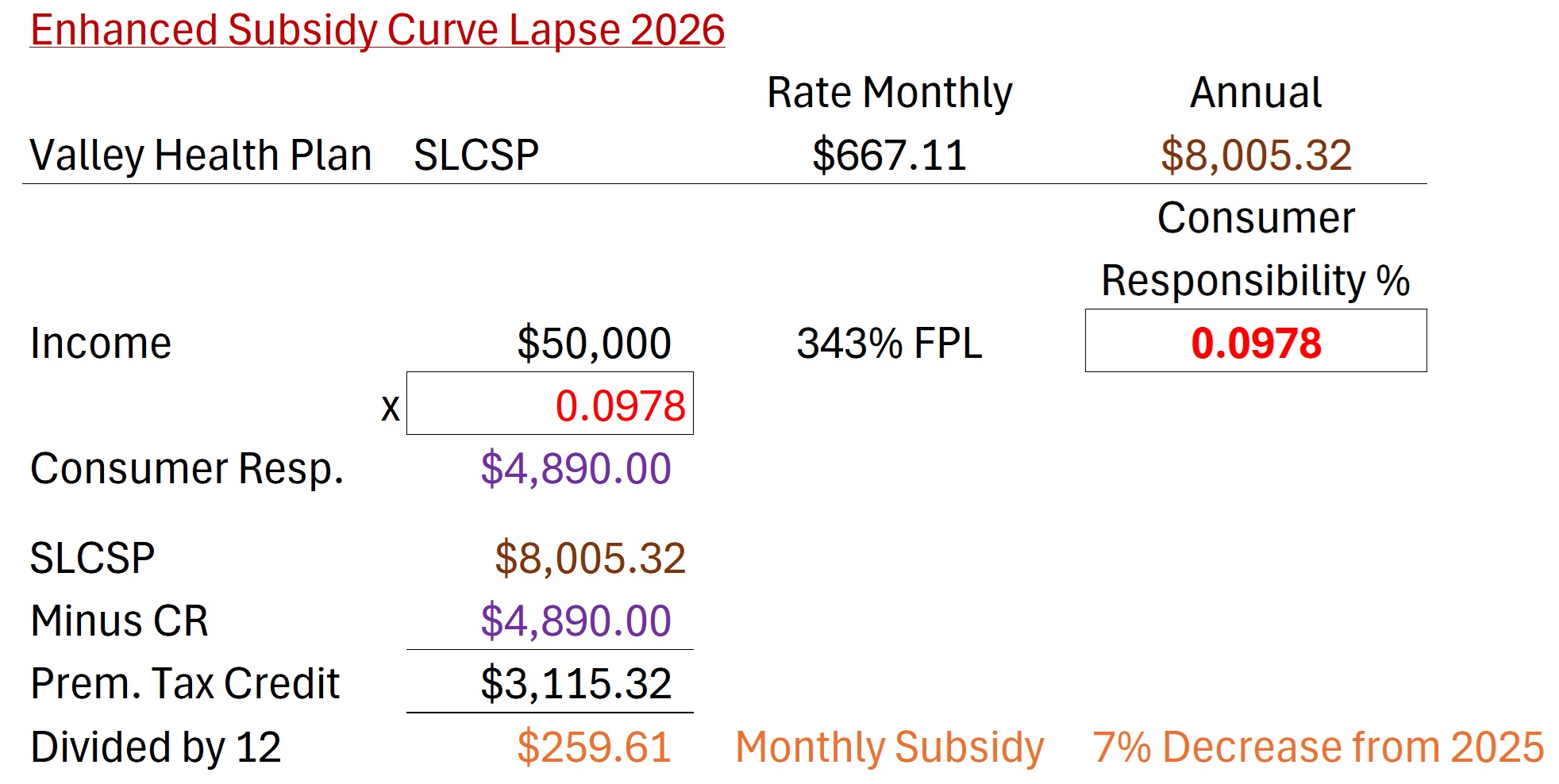

If the enhanced subsidy lapses, and Covered California must return to the pre-2021 subsidy curve, the consumer responsibility for health insurance increases. For the individual estimating $50,000, based on 2025 federal poverty level, they are still 343 percent FPL, but the consumer responsibility percentage increases from 7.08 percent to 9.78 percent*. (*Consumer Responsibility from IRS 2020 form 8962 instructions.)

This means that the consumer is responsible for $4,890.00 for the SLCSP health plan. The VHP is still the SLCSP with annual premium of $8,005.32. We subtract the consumer responsibility from the SLCSP annual premium for an annual Premium Tax Credit amount of $3,115.32. This translates into a monthly subsidy of $259.61 or a 7 percent decrease from 2025.

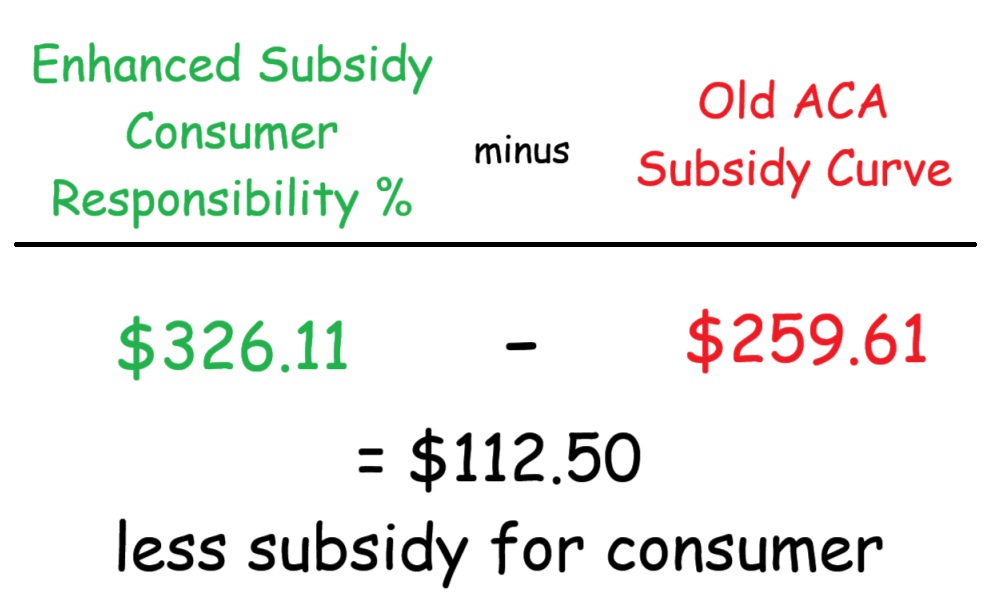

If the enhanced subsidies are not renewed, in this scenario, the 40 year old with an income $50,000 will pay $112.50 ($372.11 – $259.61) more for health insurance if they keep a Silver plan in Santa Clara County. Of course, the higher consumer responsibility, lower subsidy amount, will apply to everyone buying health insurance through Covered California.