Individual and family plan rates have increased faster than small groups in California.

In the beginning, when the ACA and Covered California kicked off in 2014, individual and family health insurance premiums tended to be lower across the board than small group rates. Over the last several years as individual and family rates have seen double digit rate hikes, small group premiums for the same carrier are generally lower. Sometimes the small group rates from the same carrier for a similar metal tier level plan can be 25% less than individual and family rates.

Small group rates initially spiked up with the introduction of the ACA. The carriers had to add benefits to the plans that were not being offered and they had to make them actuarially compliant with the standard metal tier levels of Bronze 60, Silver 70, Gold 80 and Platinum 90. The higher small group rates with the addition of the Covered California subsidies led many small employer groups to close their plans so the employees could take advantage of the premium assistance through Covered California.

Small Group Rates Lower Than Most Individual & Family Health Insurance Premiums

In 2019 we are seeing small group rates in the market place at levels that are below individual and family plan (IFP) rates offered either through Covered California or off-exchange directly with the carrier. This is in large part because IFP rates have witnessed double digit rate increases over the last several years, whereas the small group rates have been in the single digits. There are also more carriers that offer plans in the small group market than in the IFP arena.

More Small Group Plans With Larger Provider Networks, Lower Rates

Today, employees often times have access to more health plans from carriers not in the IFP market at rates substantially below the lowest cost IFP plan. In addition, the small group plans usually have larger provider networks (i.e. more doctors and hospitals in-network) and other benefits not offered in the IFP market. One example is that Blue Shield offers the BlueCard program for their small group plans but not in the IFP market plans. As the disparity between carriers, benefits, and rates have grown between small group and IFP, I decided to compare the rates for some of my current clients in the small group plans versus offerings in the IFP market.

The metal tier level small group plans do not mirror the standard benefit design of the IFP market as set forth by Covered California. There can be differences between the copayments, coinsurance, deductible, and maximum out of pocket amounts for the same metal tier level. This would lead some people to ascertain that we can’t make a direct comparison between a Silver small group plan and a Silver individual and family plan. And I don’t necessarily disagree.

Comparing Metal Tier Levels

However, what is consistent is the actuarial designation of the plans. The number after the metal tier designation denotes the actuarial value of the plan. Let’s take Silver 70 as an example. The 70 means that in the pool of people enrolled in the health plan, the average person will have 70% of their health care costs covered by health plan. Some people in a Silver 70 will have 90% of their costs covered while another person may only experience 50%. But the average person will have 70% coverage for their medical expenses.

While the small group plans don’t exactly match the benefit designs of the IFP coverage, we can compare the relative cost of the actuarial values. I compared some of my renewing small group clients and recent quotes for small group plans to comparable IFP rates. Because Covered California Silver plan rates are artificially inflated, when necessary, I compared the small group rates to the off-exchange IFP plan rates.

The following rates were pulled from quotes from California Choice small group exchange and Covered California for Small Business for either 4th Quarter 2018 enrollment or 1st Quarter 2019 enrollment. Small group plans can have quarterly rate changes for the groups. IFP rates are generally guaranteed for the calendar year.

Sutter Health Small Group Plans

The first comparison was of two individuals at a Sacramento company enrolled in a Sutter small group HMO Silver plan. The rate for the 60-year-old employee is $838 and $688 for the 56-year-old employee. An IFP Silver plan directly from Sutter Health Plus HMO is $1,115 for the 60-year-old and $958 for the 56-year-old. The IFP rate is 25% and 28% higher than the small group plan at the respective ages. The lowest IFP plan available to these employees in the Sacramento region is a Kaiser Silver HMO plan at $990 for age 60 and $851 for age 56.

Oscar Small Group Los Angeles

The Sutter differential in premium rates seemed to be on the high side for the groups I compared. In Los Angeles County I have a 25 and 27-year-old enrolled in a small group Oscar health plan. Their rates for an Oscar Gold plan are $315 and $322. An IFP Oscar Gold plan at those ages is $381 and $398 representing 17% and 19% higher rates. However, in their region, a L.A. Care Covered Gold health plan would cost $277 and $289 for the 25 and 27-year-old individuals. Of course, when you factor in that the employer is making a 50% minimum contribution toward the employee’s health insurance, they are still better off in the Oscar small group plan.

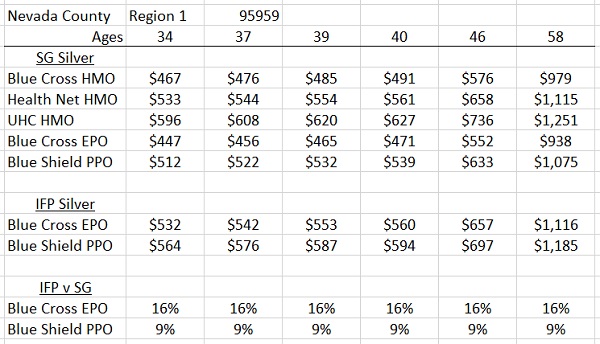

Nevada County Small Group Offerings

Many rural California counties may only have one or two IFP carriers to select from. In the small group there can be many more options including carriers who don’t offer individual and family plans either through Covered California or off-exchange. One of my small groups is in Nevada County where only Anthem Blue Cross and Blue Shield of California are offered. But in the small group market there are also plans from Health Net and United Healthcare.

For this small group, at the Silver metal tier level, only the United Healthcare (UHC) HMO was consistently more expensive than any IFP plans offered in Nevada County. The Health Net HMO Silver rates were remarkably similar to the Blue Cross IFP Silver plan. More than likely, both the Health Net and UHC plans, both of which are HMOs, have larger networks than the IFP offerings. In a comparison of the most similar plans between the small group and IFP – Anthem Blue Cross EPO and Blue Shield of California PPO – the small group rates are less: 16% for Blue Cross and 9% for Blue Shield. This is on top of the fact that both of these blue plans have larger networks than their IFP products in the same county.

Individual and family Silver plan rates are 9% to 16% higher for the comparable small group health plans offered by Blue Cross and Blue Shield in Nevada County.

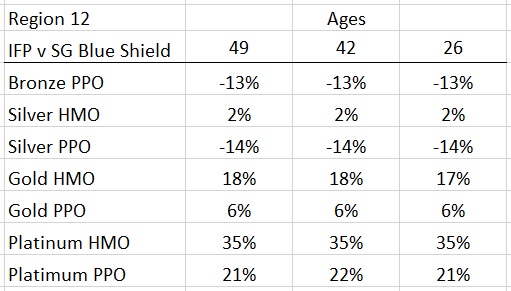

San Luis Obispo Blue Shield Small Groups

The last comparison I did involved a small group in San Luis Obispo. In this particular area individuals and families only have access to Blue Shield plans. On the small group side, there are health plans from Blue Shield, Blue Cross and United Healthcare. The Blue Shield HMO small group plan was the least expensive across all metal tier levels and the Blue Shield PPO plans were the most expensive. Blue Cross and United Healthcare rates fell in between the two. What is interesting is that the Blue Shield PPO IFP Bronze plans are 13% below the Blue Shield PPO small group plan.

Blue Shield individual and family plan rates at the Bronze and Silver PPO are lower than than their comparable small group plans in San Luis Obispo County. While IFP Gold and Platinum rates are much higher than their small group offerings.

The lower IFP Blue Shield PPO rate also applied to the Silver plans which are 14% lower than the small group rates. It isn’t until we move up to the Gold and Platinum metal tiers that the Blue Shield IFP rates are higher than the small group rates. The biggest differential occurred in the Blue Shield HMO IFP Platinum plans that are 35% higher than the comparable Blue Shied HMO small group rates across the compared ages of 26, 42, and 49.

California is broken up into 19 different rating regions for both IFP and small group markets. San Luis Obispo is in Region 12 known as the Central Coast. It can be a difficult region for health plans because limited number of doctors, hospitals, and population densities relative to regions such as Los Angeles, Orange, and San Diego counties. Consequently, it is not surprising to see rates on either the IFP or small group side that don’t necessarily fit a pattern when compared other regions of California.

For individuals and families who earn too much to qualify for the Covered California premium tax credit subsidy the rates are simply brutal. Rates in the small group market still seem high, but they have not increased as fast as rates in the IFP market. The question many people are asking is why is there a 10% to 35% differential between IFP and small group rates? Small group plans, I am told, reimburse providers at higher rates than the individual and family plans and usually have a larger network of providers also. One would then assume that small group rates would be higher than comparable IFP market plans.

If we accept the premise that health insurance rates are primarily driven by current and future member claims for health care services and prescription drugs, we are left speculating that small group members are utilizing the plan benefits and coverage less than IFP members. I have no evidence to support this hypothesis one way or the other.

What is undeniable is that small group rates for actuarially similar individual and family plans are generally lower, sometimes by a lot than health plans offered by Covered California or directly from the carrier. Is this an incentive for an employer to offer a small group plan to their employees? Low and moderate wage employees will still, in most instances, pay less by going through Covered California and qualifying for the premium tax credit subsidy. But if the bulk of the work force is made up of higher wage employees who qualify for little or no subsidy, a small group plan would be advantageous for them compared to them enrolling in off-exchange individual and family plans.