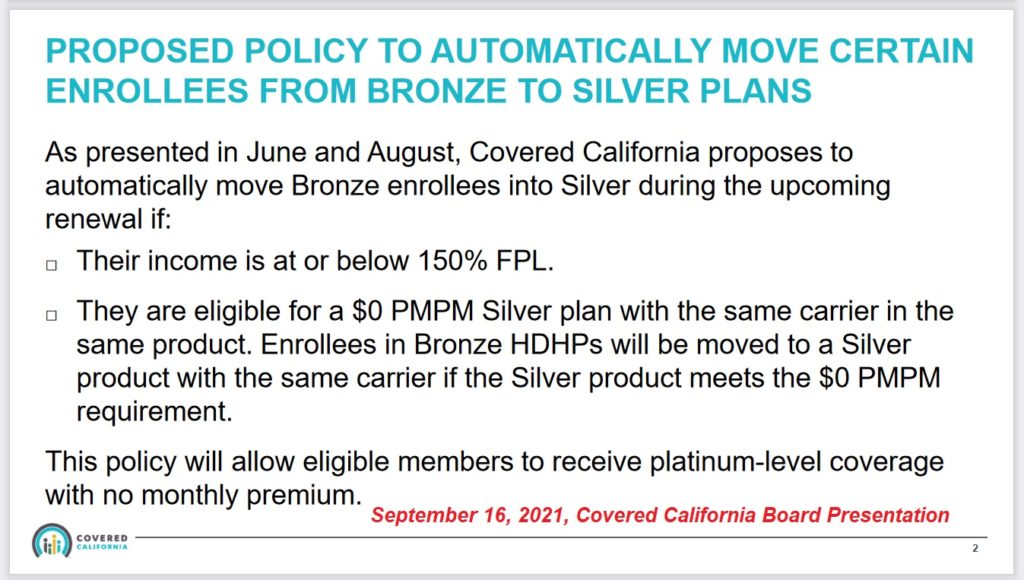

Without your permission or knowledge, Covered California may change your metal tier level plan from Bronze to Silver. At the September 16, 2021, Board meeting, the Covered California Board members affirmed that they know what is good for you and your family by passing the proposed Bronze to Silver plan policy. If this new policy leaves you having to repay a whole bunch of excess subsidy to the IRS, well, too bad.

The unauthorized flipping of consumers from Bronze to Silver plans will follow certain conditions.

- The estimated household income must be at or below 150 percent of the federal poverty level.

- Household members in Bronze plans are eligible for a $0* monthly Silver with the same carrier.

*For 2022, Covered California will credit all consumers $1 to make previously $1 enrollments become $0 monthly premiums.

Bronze to Silver Switch Without Your Consent

For example, an individual has selected a Bronze plan and pays $0 per month. The household’s estimated income is between 138 and 150 percent of the federal poverty level ($17,775 to $19,140, 2021 income figures for individuals.) If the subsidy the individual is eligible for, exceeds the cost of a Silver plan with the same carrier, Covered California will automatically flip that person into the Silver 94 plan. This directive, on the part of Covered California, will also apply to individuals in High Deductible Health Plans (HDHP) that are Health Savings Account compatible.

The move of consumers from Bronze to Silver will occur at the 2022 automatic renewal period. It has the potential to affect several hundred thousand people, but in reality, it will be far fewer. The condition that the Silver plan must be $0 per month means that many consumers will not be flipped out of their Bronze coverage. If the household has chosen a relatively expensive Bronze PPO plan, and the Silver plan from the same carrier would be more than $1 per month, the consumer should not be switched.

Higher Subsidy Liability

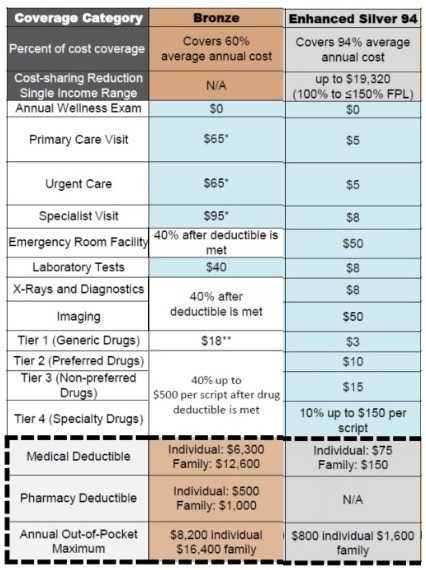

The Silver 94 plans can be very advantageous for people. They have lower copayments, deductibles, and maximum out-of-pocket amounts. The health plans have no disagreement with this flipping scheme because they will be receiving more money for people who rarely seek health care services.

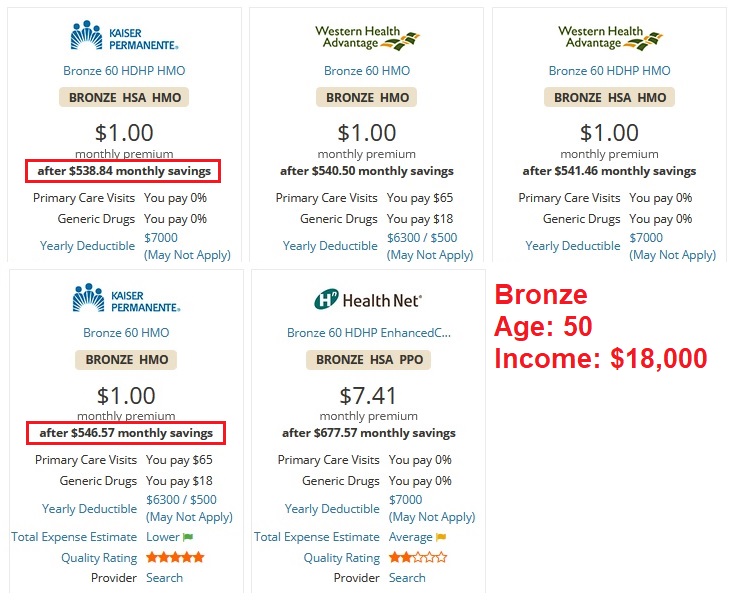

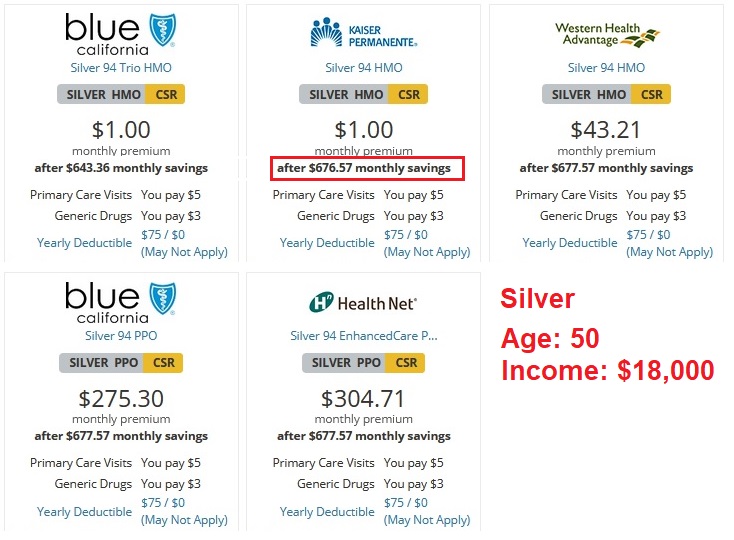

For the Silver plan to be $0 monthly premium, the subsidy must be larger than the rate. For a 50-year-old individual in Sacramento, (using 2021 rates), the difference between a Bronze and Silver Kaiser plan is approximately $130. If the individual estimates $18,000 income, it generates a subsidy larger than the cost of the Kaiser Silver plan. This person would be flipped from a Bronze to Silver Kaiser plan. All Silver plans from the same carrier (70, 73, 87, & 94) have the same rate.

The gift to the consumer is not only a better health plan, but additional subsidy liability. The subsidies are based on the estimate income. If the final income amount is higher when the consumer does their federal taxes, they may have to repay a sizeable portion of the subsidy back to the federal government.

I’m sure many consumers will welcome the passive switch from a Bronze plan to a Silver 94 without having to pay anything more for the health insurance. An equal number of individuals will be perturbed that Covered California assumes they can unilaterally make decisions about a person’s health insurance with no consent from the effected member.