If you leave Covered California in the middle of the year and your income increases after you leave, you will have to repay the excess subsidies you received at the lower income estimate. In most cases, the subsidies are not based on the income estimate when you first enrolled in Covered California. They are based on your final Modified Adjusted Gross Income.

Many individuals and families enroll into Covered California for a few months until other health insurance such as employer group plan or Medicare becomes effective. In these situations, the families may not know what their taxable income will be for the year. They enter the current income, which can be lower if future events turn in their favor.

Repaying the Covered California Subsidies AFTER You Leave Enrollment

Many of these families assume the subsidies are based on the income they were receiving during the time of their Covered California enrollment. Unfortunately, that is not the case. If the family exits Covered California and their household income increases, they may be liable to repay part or all the excess subsidies they received.

Because the household is no longer in Covered California, they have no way to adjust their income, receive a lower subsidy, and possibly not have to repay the excess subsidy. In other words, the subsidy paid on their behalf is locked and there is no way to reduce the liability.

There are many reasons why a family’s income may increase after they have left Covered California.

- Higher income from new employment

- Sale of stock or house

- Social Security retirement income

- Win the lottery

A higher Modified Adjusted Gross Income AFTER you leave Covered California does not exempt you from having to repay the excess subsidies.

Consumer Responsibility, Form 8962

The subsidy calculation is based on a formula outlined in IRS form 8962 Premium Tax Credit reconciliation. The derived subsidy from the initial income estimate is advanced by the marketplace exchange Covered California to the health plans.

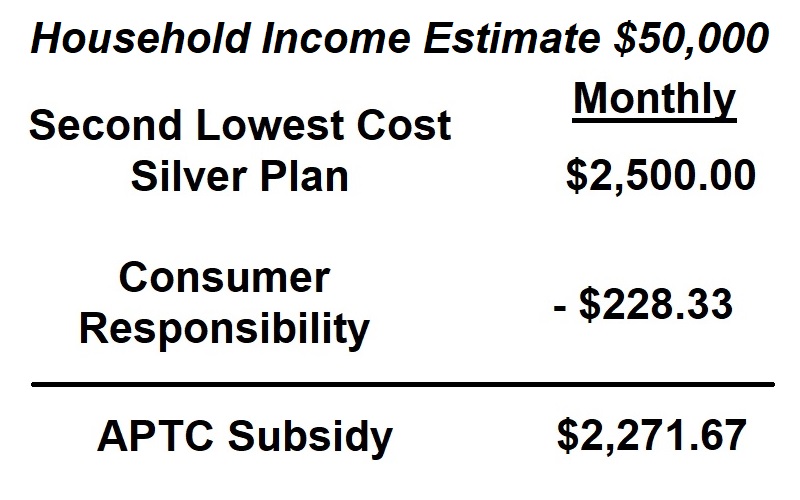

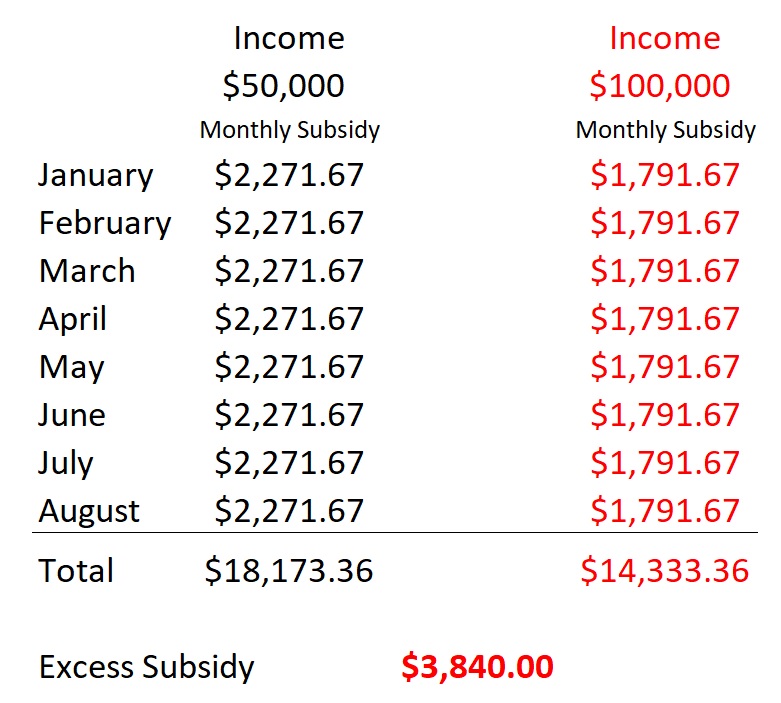

To illustrate how the original subsidy is calculated, let’s take Sue and Bob, who are both 62 years of age living in Placer County, California. When Sue and Bob enrolled into Covered California, they estimated their household income at $50,000 for the year. They left Covered California in September because Bob went back to work and was offered employer sponsored health insurance.

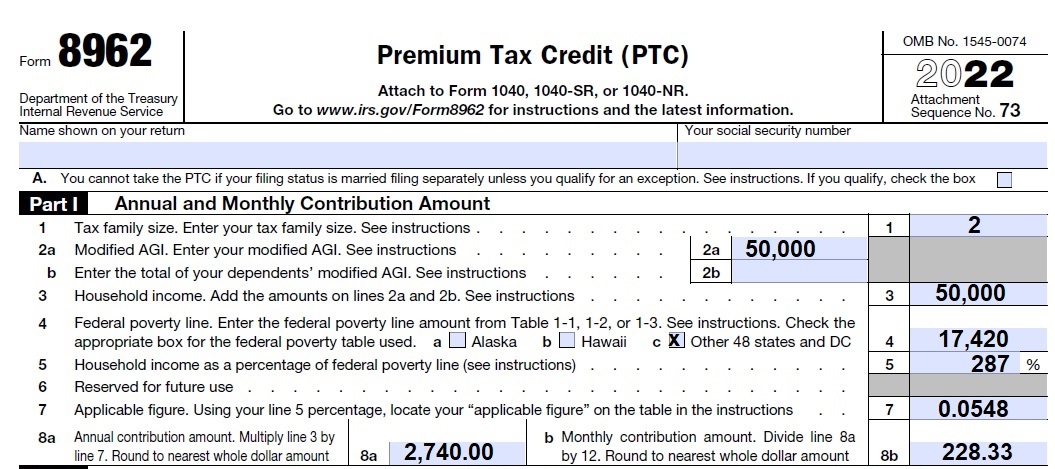

In the period Sue and Bob were in Covered California, they received a subsidy of $2,271.67 each month based on an estimated income of $50,000. That estimated income translated into a consumer responsibility of $228.33. The consumer responsibility portion is derived from IRS form 8962.

The household income of $50,000 is calculated to be 287 percent of the federal poverty level (line 5.) The percentage corresponds to a table in the instructions for form 8962 that indicates a consumer responsibility or applicable figure of 0.0548 or 5.48 percent. The household should spend no more than 5.48 percent of the household income for the second lowest cost Silver plan. In other words, 5.48 percent of $50,000 is $2,700 annually or $228.33 per month. The subsidy, Advance Premium Tax Credit, makes up the difference and is forwarded by Covered California to the select health plan each month.

Higher Income, Higher Consumer Responsibility, Lower Premium Tax Credit

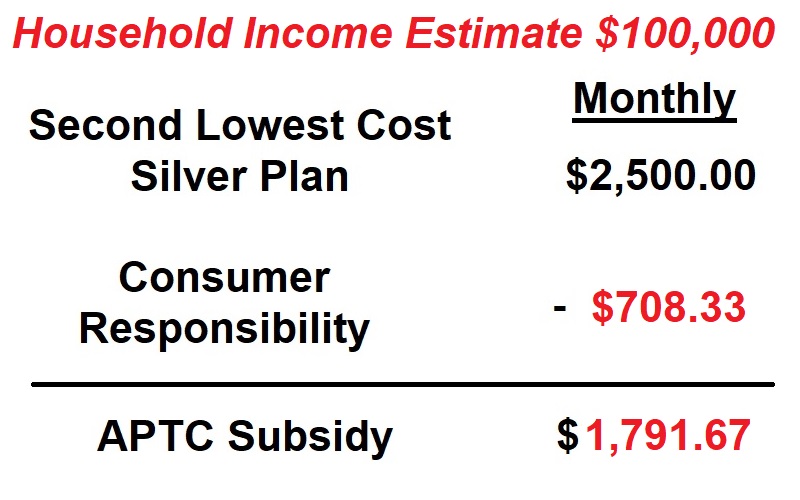

Bob was hired in August with a new employer who offered health insurance. Sue and Bob left Covered California at the end of August. Bob’s new employment increased the couple’s household income at the end of year to $100,000.

When Sue and Bob do their taxes, they must reconcile the health insurance subsidies they received on form 8962. The final Modified Adjusted Gross Income for Sue and Bob of $100,000 was 574 percent of the federal poverty level. Their consumer responsibility for health insurance was 8.50 percent or $8,500 annually, $708.33 monthly.

Calculating Excess Repayment of Health Insurance Subsidies

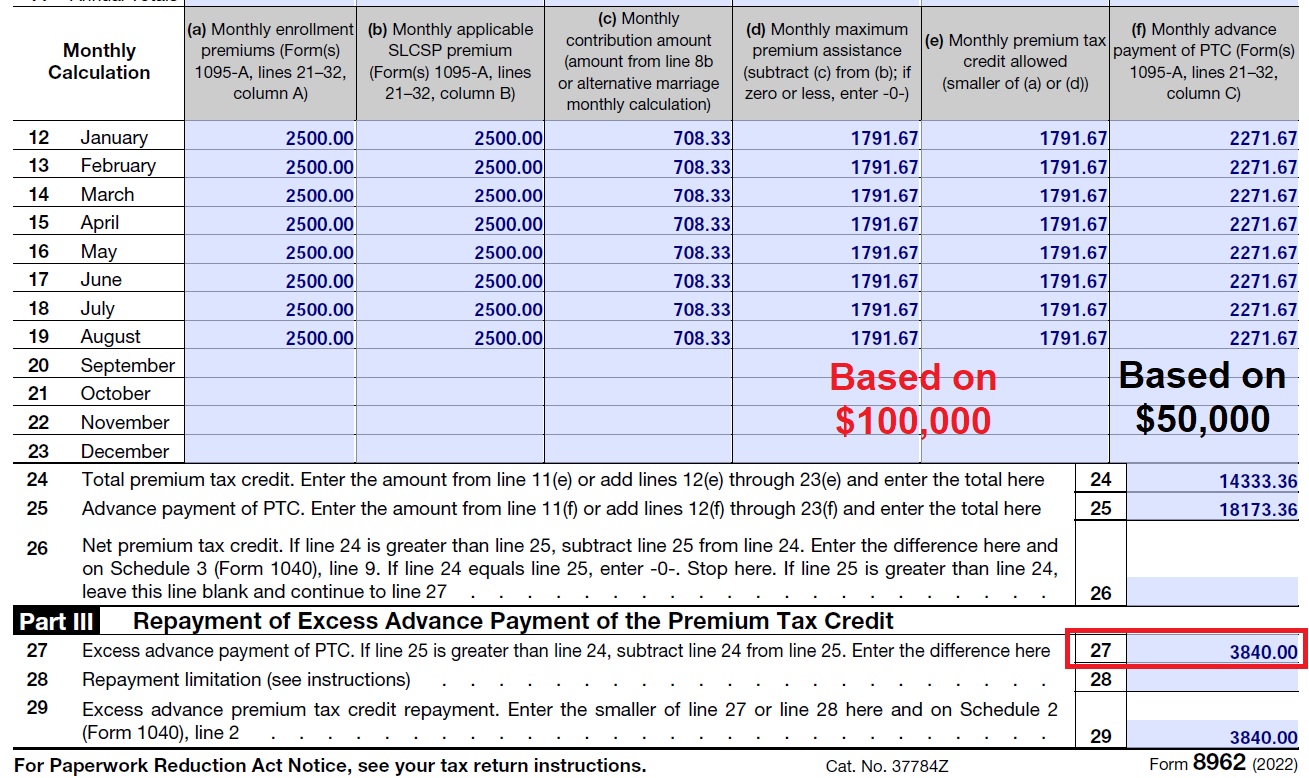

The difference between the subsidies and Sue and Bob received under a $50,000 income estimate and the final income of $100,000 is reconciled on part II of form 8962.

The first two columns reflect the premium of the health plan Sue and Bob enrolled into and the second lowest cost Silver plan. Column c is the monthly consumer responsibility for the health insurance under the $100,000 income. Columns d and e reflect the subsidy Sue and Bob were entitled to after the consumer responsibility of $703.33. They were entitled to a $1,791.67 monthly subsidy ($2,500.00 – $703.33.) The 1095A tax form Sue and Bob received provided column a and b (health plan premiums and second lowest cost Silver plan), it notes the Advance Premium Tax Credit of $2,271.67 monthly (column f.) The $2,271.67 was paid to Sue and Bob’s health plan each month from January to August when they left Covered California.

Sue and Bob received $3,840 in excess Advance Premium Tax Credit for the year. Because their final income is over 400 percent of the federal poverty level, they must repay all the excess health insurance subsidy.

It may seem unfair to have to repay a subsidy you were receiving for health insurance when your income for those months was verifiably lower. If Sue and Bob had stayed in Covered California through the end of the year, they would have had the opportunity to increase their income, lower the monthly subsidy, and potentially avoid a large repayment of excess subsidy. But Sue and Bob left Covered California in September. Their only recourse, because the annual consumer responsibility and subsequent subsidy is based on the final Modified Adjusted Gross Income, is to repay the excess amount.