While Covered California has announced very modest health insurance rate increases for 2022, some consumers will see premium increases on the order of over 1,000 percent. How is this possible? Households who were granted the extra subsidy for collecting unemployment insurance in 2021 will see that enhanced benefit evaporate in 2022. Plus, many people who had been offered the Silver 94 health plan with very low copayments will revert to the Silver 70 with higher cost-sharing.

Extra Unemployment Subsidy Expires at End of 2021

Under the American Rescue Plan passed in March of 2021, if any household member collected unemployment benefits for at least one week in 2021, and it was reported to Covered California, the household income was artificially lowered to just above Medi-Cal eligibility range of 138.1 percent of the federal poverty level. The act of assigning the very low income to the household did two things.

- The subsidy was based on the lower income and retroactive to the beginning of January 1, 2021.

- The household members were then eligible for the Enhanced Silver 94 health plans with cost-sharing reductions.

Both of these health insurance enhancements will go away on January 1, 2022.

Smaller Subsidy Based on Estimated Income

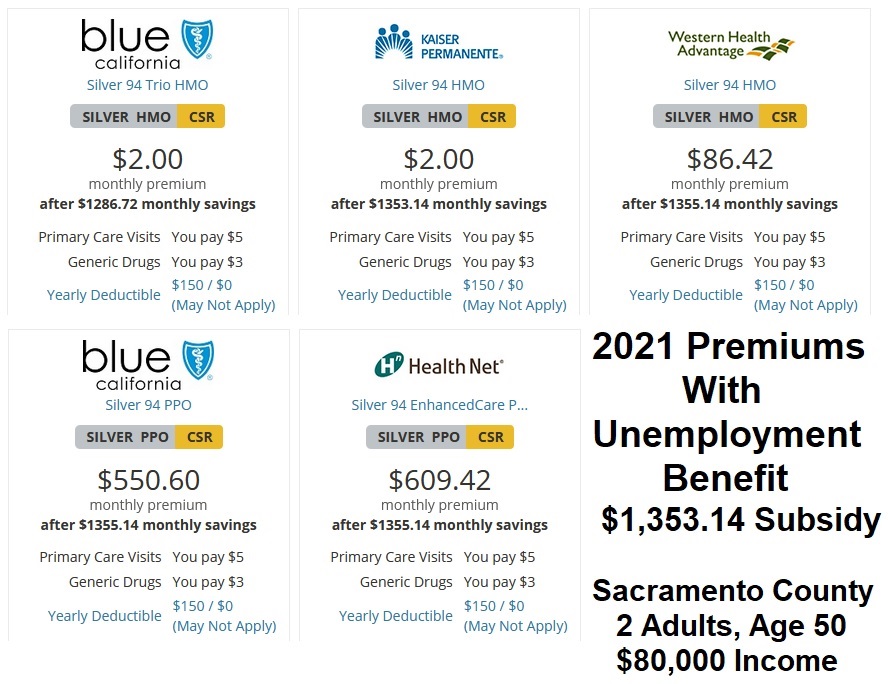

For a household of two adults, residing in Sacramento County, with an estimated income of $80,000, where one of the adults collected unemployment benefits, their subsidy increased to at least $1,353.14 per month based on the rate for the second lowest cost Silver plan. Instead of being offered a Silver 70, the couple could enroll in a Silver 94 with $5 office visit copayments and a $75 individual medical deductible.

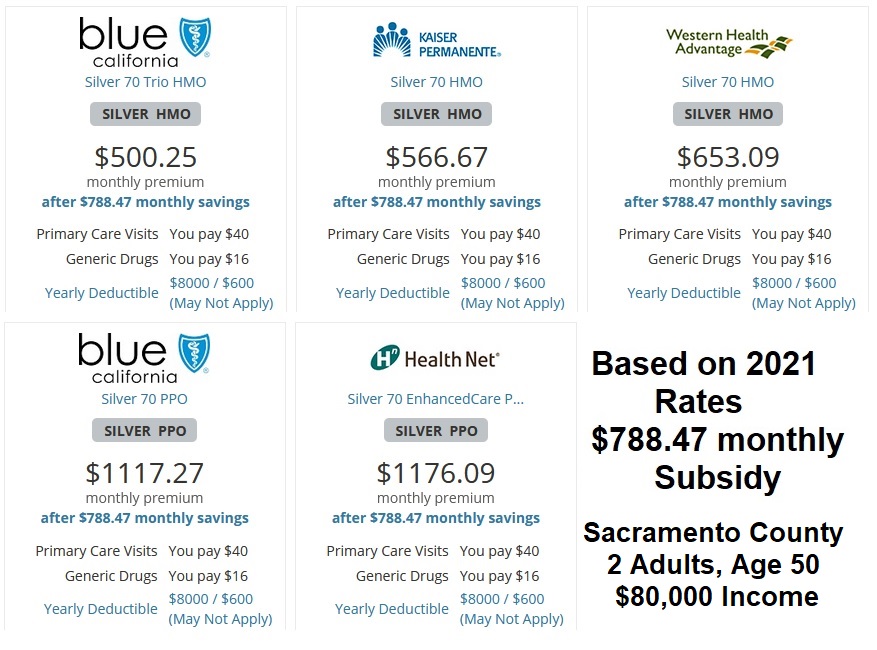

This same couple, based on 2021 rates, would have had a monthly subsidy of $788.47. If the couple were enrolled in the second lowest cost Silver 94 plan at $2 per month in 2021 – with the removal of the unemployment benefit – their new monthly premium will be $566 in 2022, that is a 28,000 percent increase. Plus, they will revert to a standard Silver 70 plan with higher cost-sharing. (For 2022 Silver 70 office copay will be $35 with a $3,700 individual medical deductible.)

The premium increase could be worse for families who selected a higher cost Silver, Gold, or Platinum plan. The unemployment benefit enhanced subsidy was effective January 1, 2021, but not applied until May. The subsidy for the first four months of the year were taken and spread out over the remainder of the year, according to Covered California. The loading of the subsidy in the last three quarters of 2021 will amplify the premium disparity for 2022. In other words, the unemployment subsidy was more generous than most people realized and their 2022 premiums will be larger than they expected.

Loss of the Silver 94 Reduced Cost-Sharing

If the household income was already in the Silver 94 range (138 – 150 percent of the federal poverty level) and the income remains the same for 2022, that family will keep the Silver 94 plan. They may not even see a difference in the premiums between 2021 and 2022. Other households who did not select the lowest or second lowest Silver plan (or higher metal tier) will certainly see a big spike in the 2022 monthly health insurance premium. This is because the subsidies are based on making the second lowest cost Silver plan affordable.

If there is one bright spot is that households who reported the unemployment insurance benefit income to Covered California should not be subject to repaying excess subsidy because their income was significantly higher than they estimated. I increased the income by $15,000 for one family who had unemployment income in the Covered California system and it had no effect on the subsidy. While we don’t know how the IRS will treat this unique subsidy year, if Covered California is any indication, there will be no penalty for earning substantially more than the estimated income.