Health care coverage plans for individuals and families who are healthy and maintain a health lifestyle.

I’ve been told by more than one person that they are in tip-top physical condition and they resent having to pay high health insurance premiums when they never go to the doctor. Now there is an alternative to traditional health insurance that is aimed at fitness buffs and gym owners. SHM FIT combines a health care expenses sharing group with a high deductible catastrophic health plan to offer health insurance premiums that may be less than traditional insurance.

Health Insurance For Gym Owners & Trainers

The ideal health insurance plan for most healthy people is one where a short term health challenge has a manageable cost associated with it coupled with a backstop or cap in case of a catastrophic event. Similar to the unexpected dental expense of a root canal or crown, most people are comfortable shouldering a $300 to $800 bill for minor urgent care. Many people who really focus on their health and rarely see a doctor have little use for health plans with low office copayments or drug coverage for expensive drugs for chronic medical conditions they don’t have. What everyone wants is a big backstop to catastrophic health care expenses such as hospitalization because of an accident. Unfortunately, for a variety of reasons, health plans that resemble a moderate deductible coupled with catastrophic cap don’t really exist.

SederaHealth Employer Health Care Sharing Guide

In order to develop health coverage that appeals to folks who are healthy and focused on their health, SHM.FIT has combined SederaHealth, a health care sharing group, with a catastrophic Minimum Essential Coverage health plan.

Minimum Essential Coverage

Under the Affordable Care Act, individuals and families must have health coverage that meets Minimum Essential Coverage (MEC). MEC plans include the mandatory ACA no-cost preventive office visits for men, women, and children. They usually have a high annual maximum out-of-pocket (MOOP) amount between $6,800 and $7,100. Except for the preventive office visits, there is no coverage for any health care services until the member reaches his or her MOOP. Once the member hits the MOOP, the MEC plan pays 100% of all in-network covered benefits. The MEC plans are the catastrophic coverage that many people want without all the frills of more expensive health plans.

If the MEC plan has your back for the catastrophic bills, what about the urgent care visit you need after flipping over on your mountain bike? That is where the SederaHealth comes into play. SederaHealth is a health care expense sharing group. It’s similar to the Christian health care sharing ministries where members help cover the health care expenses of other ministry members. But in place of pledge to lead a Christian lifestyle, SederaHealth requests that it members lead a healthy lifestyle. Members must agree to:

- Practice good health measures and strive for a balanced lifestyle.

- Refrain from the usage of any form of illegal substances

- No driving while intoxicated

Member Responsibility

After an individual or family enrolls in SederaHealth, they are responsible for the first $500 of any health care per incident. Health care expenses over $500 for the specific event are submitted to SederaHealth to be shared by the other members. After three $500 health care expense incidents, the fourth incident member responsibility drops to $300. The health care incidents are within a 12-month period. There is no annual or lifetime limit on the total dollars shared to cover a member’s health care expenses.

Sharing Medical Health Care Expenses

Claims submitted to SederaHealth are reviewed by committee. If the health care expenses are a result of some pre-existing conditions or acts that are not in concert with the health life style pledge, they may not be shared. In other words, the member may not receive any shared reimbursement to cover their medical expenses.

Individuals who come into the SederaHealth sharing group won’t have some pre-existing conditions covered. For example, if someone is recovering from a broken leg, those expenses can’t be shared. Needs resulting from insulin dependent diabetes that existed prior to membership can’t be shared.

Past health care challenges won’t necessarily be excluded from sharing coverage. If a member has been symptom free for over 12 months for some conditions and 5 years for other health issues such as cancer and back problems those medical expenses will be considered for coverage. Maternity needs such as prenatal care, delivery, postnatal, and miscarriage are all sharable expenses. Elective termination of a pregnancy, abortion, is not a shareable expense.

Prescription medications for a pharmacy can be shared for a 120-day supply. Drugs for the treatment of cancer are not limited by the time period. There is no sharing for prescription medications for chronic or recurring conditions such diabetes or high blood pressure. The focus is on short duration medications to help a person recover or drug necessary for someone to battle back from cancer.

People eligible for the SHM.FIT program combining SederaHealth and a MEC plan are gym owners, coaches, personal trainers and anyone who works out regularly. SHM.FIT is a non-profit association who acts as the employer administrator of the plan.

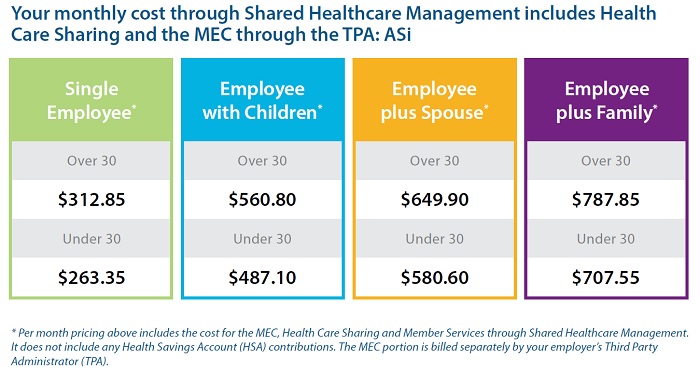

Monthly Premiums For Families, Individuals

The monthly premium rates are broken into eight categories. The first division is age. There are separate rates depending on if you are over or under 30 years old. Next is the household situation: Single, Single with Children, Married Couple, and Married Couple with Children.

2015 SederaHealth SHM_FIT health sharing plan monthly premium rates.

The SHM.FIT SederaHealth combination is not a health plan suited for everyone. There are people with health challenges, or who have children with health challenges, who are better served by traditional insurance. Similarly, people on prescription medications for the maintenance of chronic health condition even though they are very healthy, may be better served with a traditional health insurance plan.

The selection of health care coverage is like playing a game of chess. Your opponent is the probability of future health care challenges and expenses. You need to understand all your options before you make a move. It’s important to remember that if you leave a standard health insurance plan, you cannot go back to it in the middle of the year. You have to wait until open enrollment for the next year before you can regain traditional health insurance. The open enrollment period is also a backup plan. If you don’t like health coverage such as SHM.FIT, you can always drop it and go into a traditional health insurance plan during open enrollment.

One criticism of the Affordable Care Act is that it did not offer enough options or variability of health plans to address different consumer needs. Part of this is the fault of the ACA and part is how Covered California designed and offered their health plans. As smart as the people at Covered California are, they need to understand that they are not the consumer’s mother. Health insurance consumers are adults and make their own decisions. They don’t need to be told that there are only certain types of health plans that will meet their needs.

Health sharing organizations coupled with minimum essential coverage are not for everyone. But it is an option for some individuals and families who are willing to take a little more risk for health care costs in return for lower monthly premiums.

SederaHealth SHM.FIT Brochure

[wpfilebase tag=file id=2118 /]

SederaHealth Member Guidelines

[wpfilebase tag=file id=2117 /]