The Covered California exchange for enrolling in health insurance is fraught with all sorts of frustrating and complicated conditions for enrollment. Aside from the built-in enrollment challenges, Covered California does offer some unique features and benefits to help individuals and families. Two of the features are income protection and the family split.

The only way you can ever receive the Premium Tax Credit subsidy to lower your health insurance premium, either on a monthly basis or when you file your federal or state tax return, is to enroll in a health plan through Covered California. The subsidy can be a form of income protection. In the event that the household has a sudden drop of income in the middle of the year, the Covered California application can be updated with the lower income amount and trigger the subsidy to lower the health insurance premium.

Outside of Covered California, a drop in household income is not a qualifying life event to enroll in Covered California to receive the subsidy. This means if the household income drops, perhaps one spouse loses employment, and the family has a health plan off-exchange, the family must continue to make their health insurance premium payments, regardless of the burden that monthly amount may impose on the family budget.

Income Protection

If you don’t anticipate having a taxable income low enough to qualify for the premium tax credit subsidies, you can still enroll in Covered California. You will pay the full health insurance premium for the health insurance. With the exception of the Silver plans, the standard Bronze, Gold, and Platinum plans offered by the carriers have the same rates either through Covered California or off-exchange direct with the carrier.

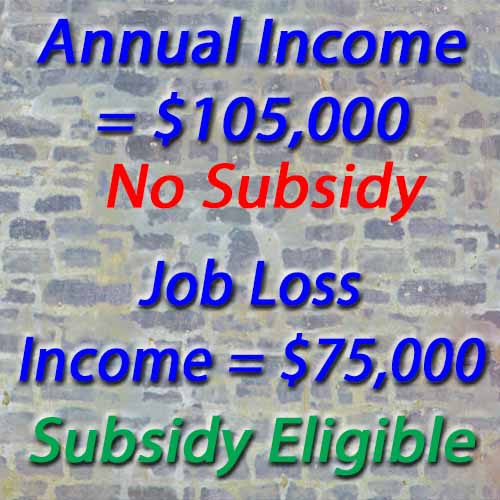

If you enroll in Covered California, under the condition of potentially seeking the subsidy, and your income drops, you can change the income and possibly receive a monthly subsidy to reduce the health insurance premium. For example, a family of four enters Covered California with an annual income of $158,000, too high for any subsidies. In June, one of the parents decides to leave their job and the household income drops to $105,000 for the year. This drop of income would trigger eligibility for a monthly subsidy to reduce the health insurance premium.

The one caveat are the Silver plans on Covered California that are artificially inflated by 10 to 15 percent over their off-exchanged mirrored counterparts. If you want a Silver plan, the off-exchange plans will provide a better rate, but without any income protection.

The Family Split

The next benefit of Covered California is the ability to easily split family members into different health plans. One family member may want a Bronze HMO plan while another household member wants a Gold PPO plan. This is perfectly acceptable within the Covered California system. Not all the household members have to be in the same plan, with the same carrier and metal tier level.

The family split is also another way to save on monthly health insurance premiums. The overall monthly premium for two household members in a Bronze plan and two in a Gold plan will be less than if the entire family was in a Gold plan.

The alternative, off-exchange, is filling out separate health insurance applications with the different carriers for enrollment. While the application is not horrendously difficult, the Covered California account quickly shows which household members are in which plans at a glance. The downside to splitting up family members is potentially losing the family deductible and family maximum out-of-pocket amounts that are usually twice the individual amounts. But if a family can save a couple hundred per month on health insurance premiums by splitting up family members, losing the family amounts may be worth it.