It was not a big surprise when we received the letter from our homeowner’s insurance company that they were cancelling our coverage. We took a few simple steps to learn about the non-renewal of coverage, performed some maintenance, and the insurance company said they would rescind the cancellation.

We live on the edge of a high wildfire danger zone. Many other homes in the community have had their coverage cancelled. There are lots of towering grey pine and oak trees throughout the community. The trees combined with the open space created by the State Park and climate change, make the insurance companies focus on how they can reduce their exposure to catastrophic wildfire losses.

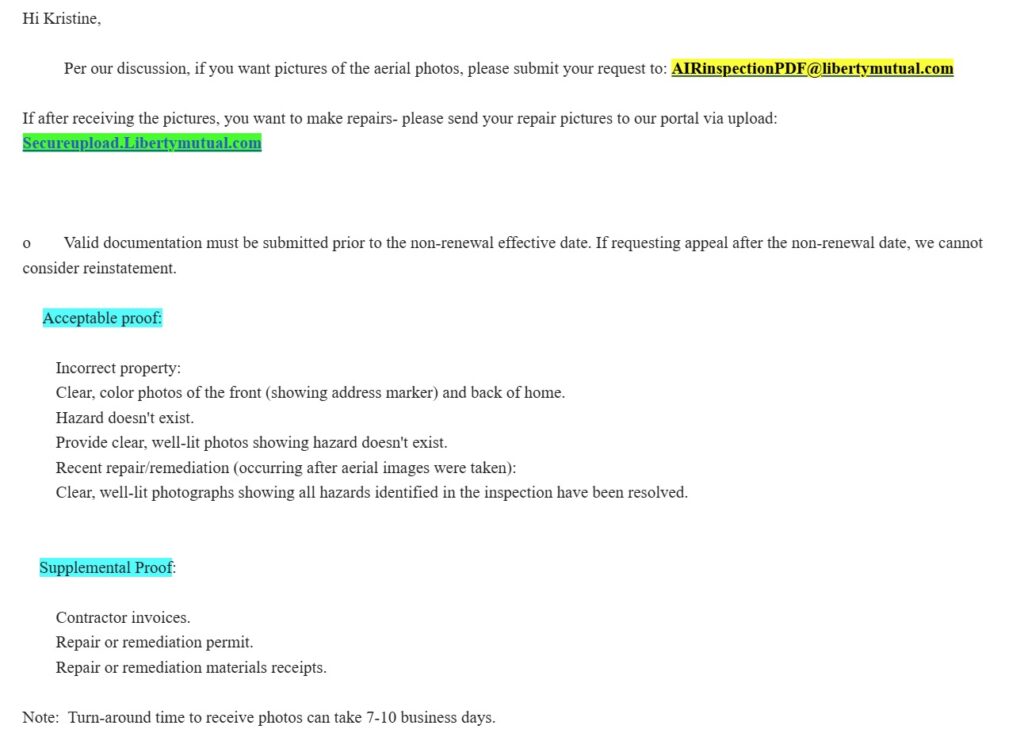

Contact Insurance Company to get the Risk Report

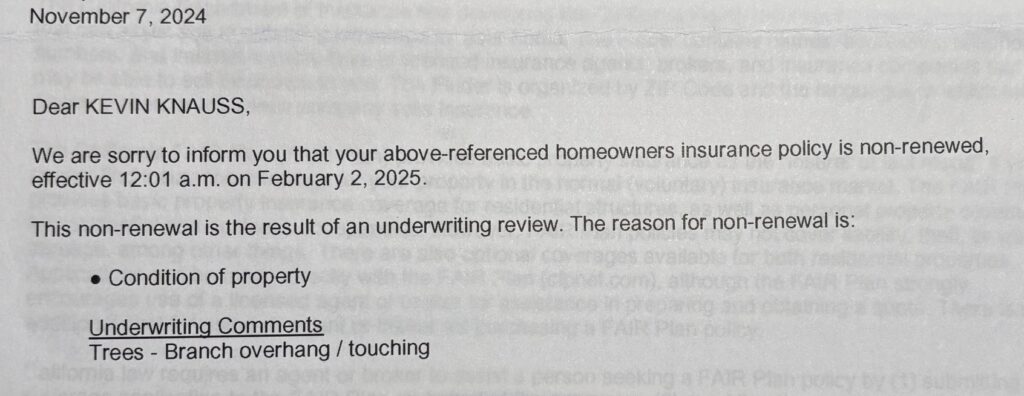

When we received the notice of non-renewal, we took action to learn how the insurance company determined not to renew the homeowner’s policy. The first step was to contact the insurance company and request the report, with images, that the underwriter used to determine non-renewal of coverage.

Technically, there is a difference between a cancellation and non-renewal. A non-renewal means the carrier has decided not to renew the policy at the end of the annual term. A cancellation is usually for non-payment of premiums or misrepresentation.

There is another hazard. Our house sits in a 100-year flood zone. We also have FEMA flood insurance on the property.

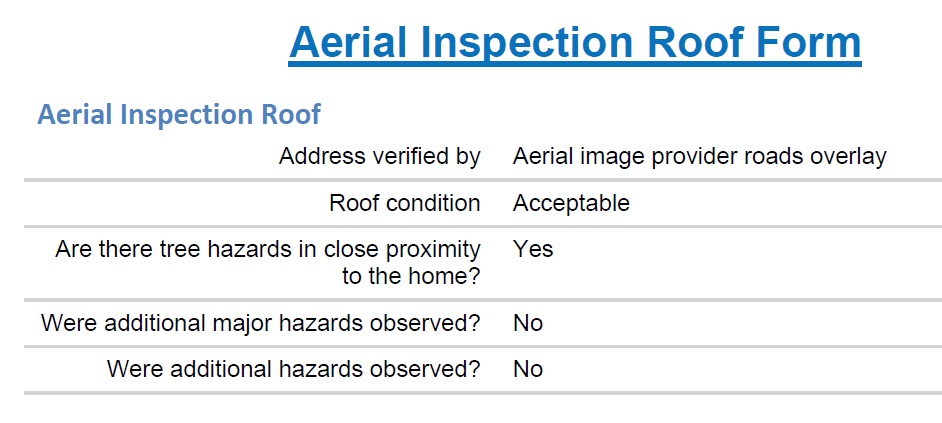

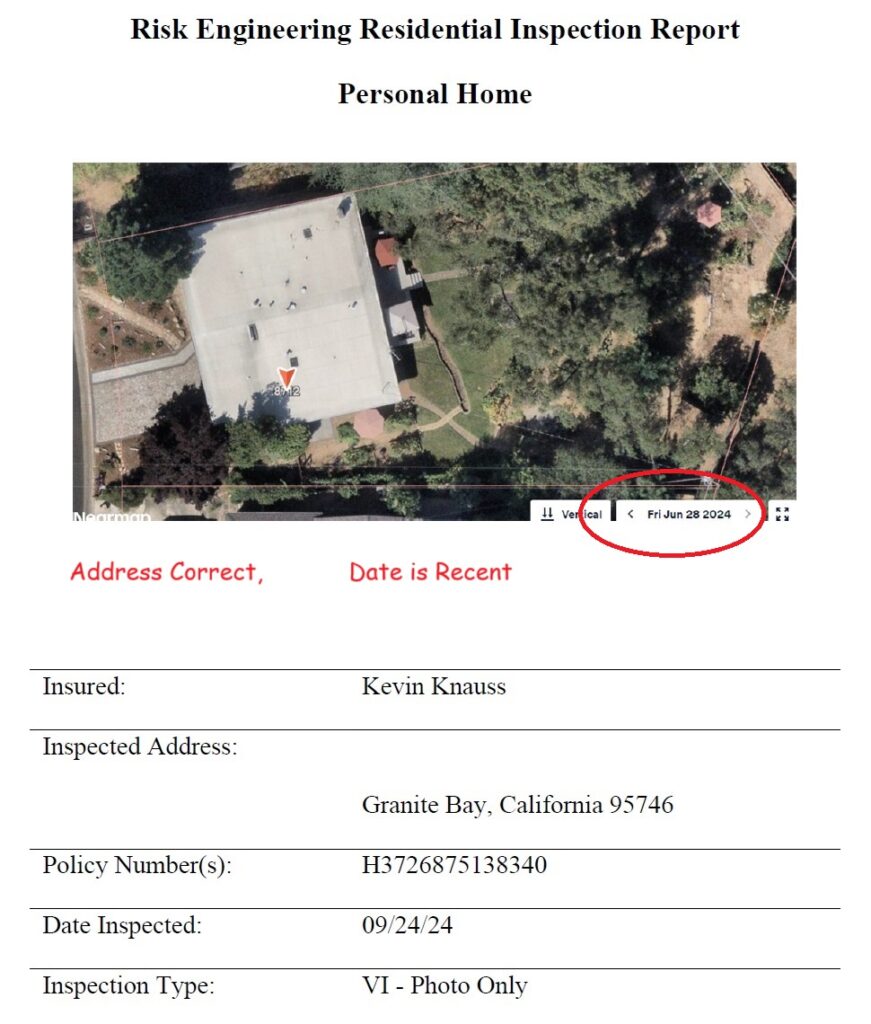

You need to request the report to make sure that the property in question is your home. Maybe they were looking at the wrong house. The images may show a condition that you have already addressed. When I received the risk assessment report, I knew the address was correct and it was my house.

The date on the aerial image was June 2024, a fairly recent picture. The images did show some of our trees had grown and the branches had either broken or droop down and were touching the roof.

The next step is learn who you contact to appeal the decision – maybe it is not your house – or provide documentation that you have addressed the condition. In our situation, everything was good except for the trees overhanging or touching the house. The only way to mitigate the condition was to severely trim the trees.

Remove Hazards That Led to Non-Renewal

We spent the weekend after we received the report trimming tree branches. I was surprised that all the trimming generated over eight cubic yards of green waste that cost me $400 to have hauled to the dump. I took pictures of the trimmed landscape showing no tree branches touching the house. I uploaded these images to a secure server along with a short description of the work, the property address, and homeowner’s policy number.

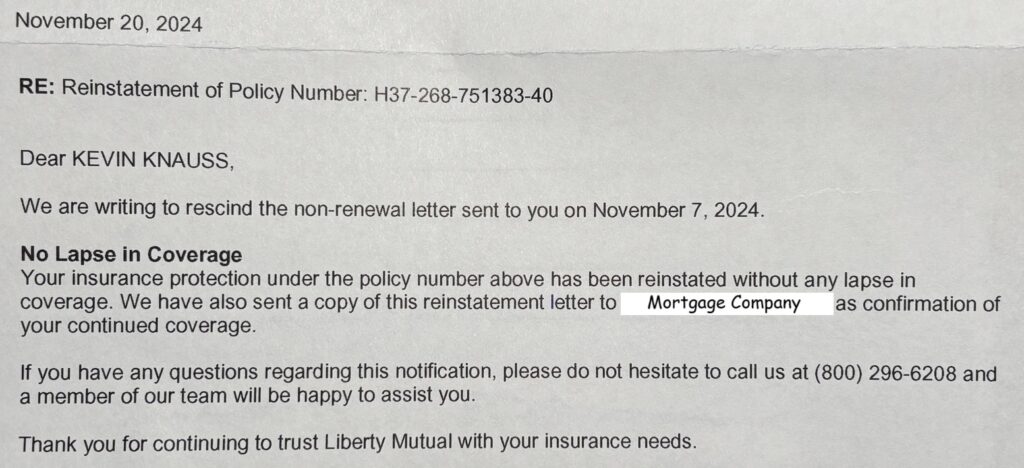

Success! Non-Renewal Rescinded

A couple weeks later, we received a letter from the insurance company stating our work was satisfactory and they were rescinding the non-renewal notice.

I don’t know if the rates will increase. We had been paying approximately $2,000 per year for the policy. When we received the cancellation notice, I called Vanasek Insurance in Chico (vanasekinsurance.com) and they got me a quote for a similar replacement policy at approximately $4,000 annually. I figure if our current carrier increases rates up to $4,000, then that is the best I can do.

YouTube video showing the work we did to address the tree hazard that led to the policy non-renewal.