There was a time when an insurance agent could make a decent living enrolling individuals, families and small groups into health insurance plans. With the advent of the Affordable Care Act and the subsequent downward pressure on commission rates, agents can still earn a living selling health insurance but it is not without its challenges. The level of knowledge and service an agent must provide to his or her clients has increased while the commission revenue per client has declined.

Beginning in 2015, I started posting the revenue or income generated by my activities as a health insurance agent in California. There are a lot of misconceptions about the income of insurance agents and many lies to entice people into selling insurance. Here is my experience…

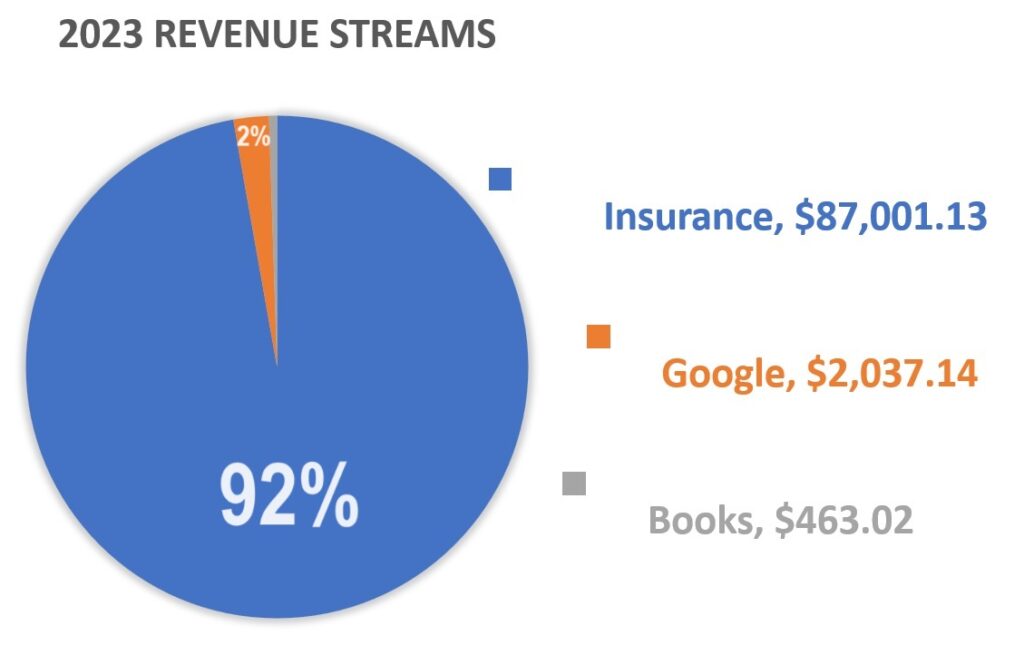

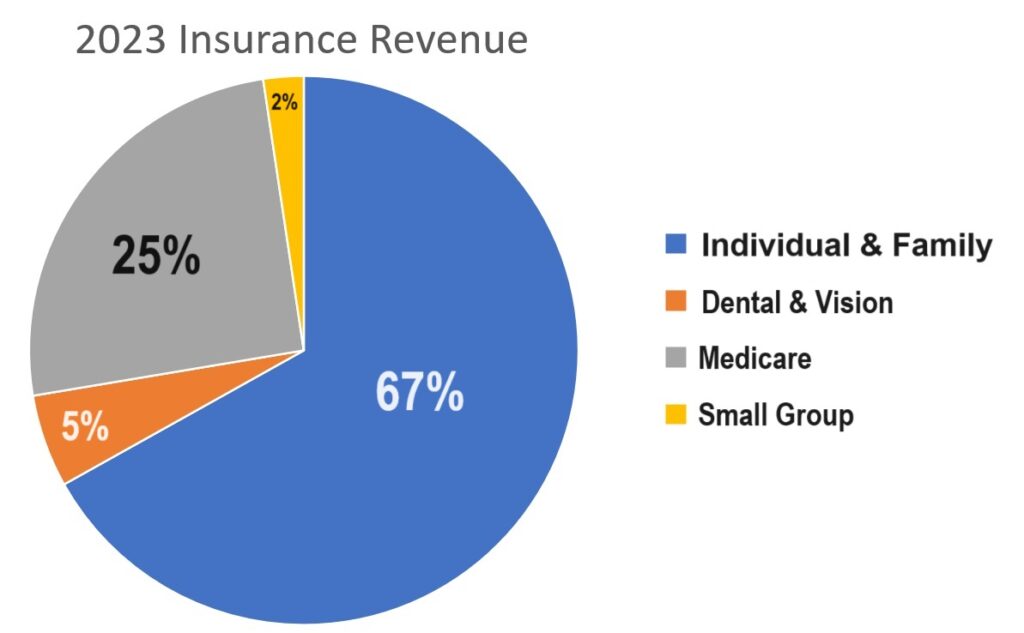

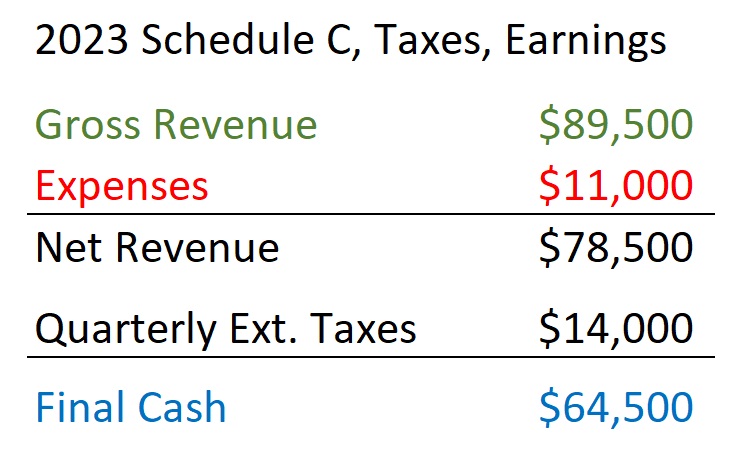

2023 Revenue Slightly Higher Than 2022

It was a fairly flat year for increases in 2023 over 2022. However, I’m not complaining. Insurance commission revenue increased about 4.5 percent. My advertising revenue decreased. The net result was a modest 2.4 percent increase in my overall revenue. Regardless, I will continue as a health insurance agent because I am having too much fun chatting with great people all across California. For a full revenue of the different segments of my revenue you can visit Insurance Revenue Increased by 4.5% in 2023.

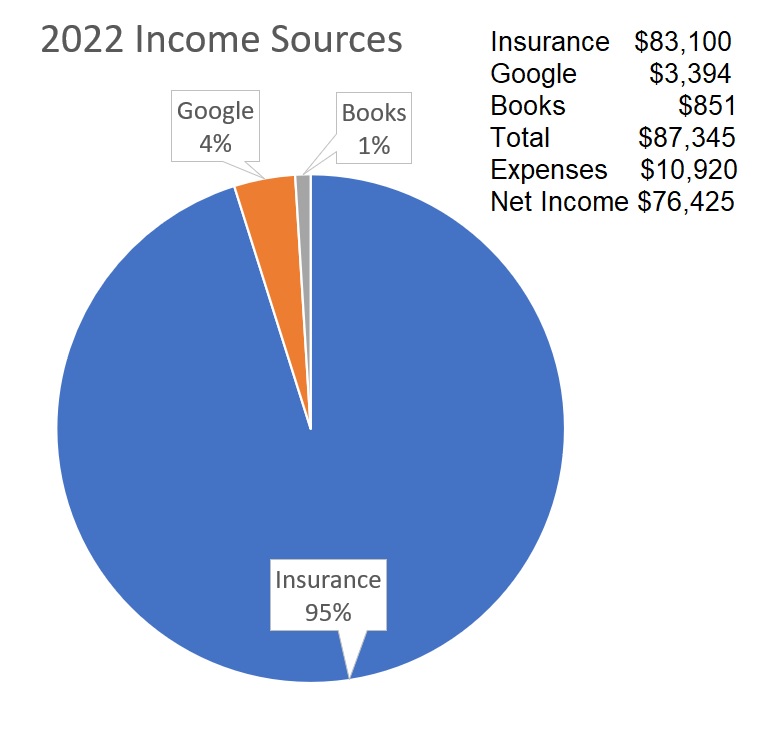

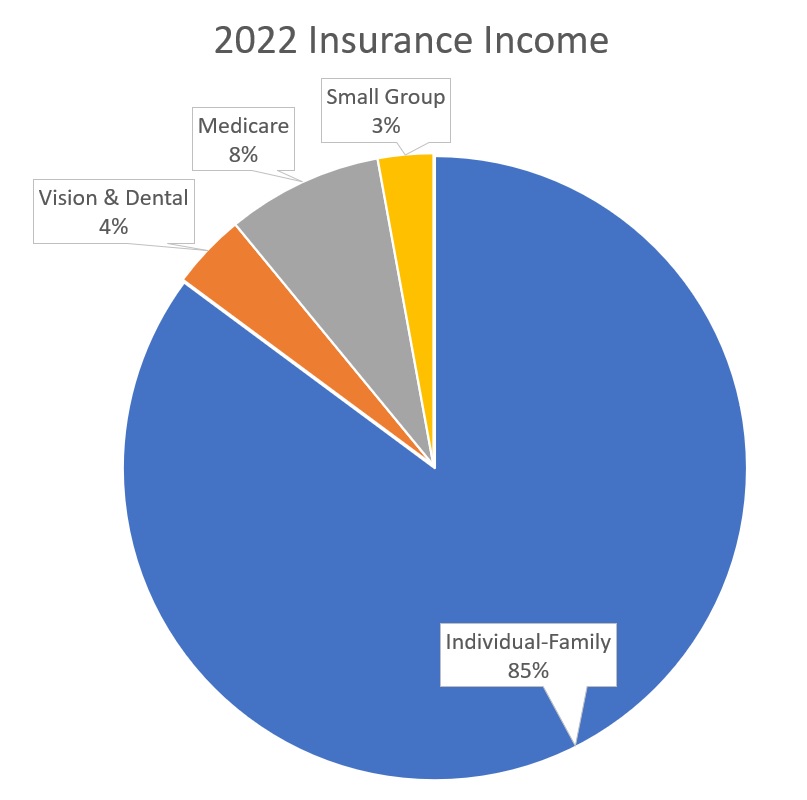

2022 Income for Kevin Knauss

Health insurance commission revenue was up slightly over 2021. Basically, there was little change in either my income or expenses from 2021 to 2022. To read more analysis of my income, please visit 2022 Net Income for Kevin Knauss.

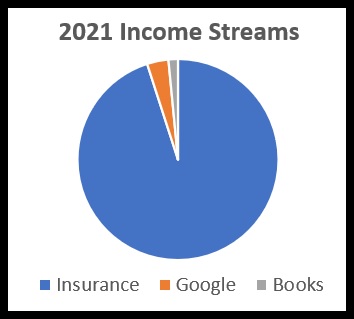

2021 Health Insurance Commission Income

Another year and I’m still paying my bills. For 2021, my different revenue streams that contribute to my overall income maintain similar proportions as the last couple of years. After expenses, my 2021 taxable income should come in at $69,000. The largest part of that income, 95 percent, is from health insurance commissions. Google made up 3.5 percent and book sales accounted for just 1.5 percent of my income.

The increase of taxable from 2020 to 2021 was not attributable to any one source. All of the income streams increased: insurance commissions, Google ad revenue, book sales. Within the insurance business, a modest increase was due to a few more Medicare enrollments as many of my individual and family clients transitioned from Covered California to Medicare Advantage or Supplement plans.

I had a few more book sales as I was able to get back to public speaking after the Covid-19 public gathering moratoriums were lifted. There was also a spike in book expenses as I incurred over $2,000 in expenses to prepare my next history book for publication in 2022.

Considering I had $0 income in the first couple of years of being an insurance agent starting in 2011, I’m relatively happy with my current situation. Just think how much I could make if I really worked at being a health insurance agent. But where would the fun be if I was just another stuffed shirt selling insurance?

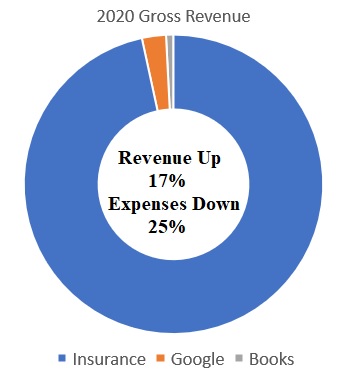

2020 Modest Gains in Gross Revenue

When I compiled my final 2020 revenue and expense figures, my taxable revenue increased over 2019. The 2020 net revenue was $57,745 compared to $47,028 in 2019. Part of the increase was attributable to decline of expenses from $13,456 in 2019, down to $10,954 in 2020. Like most people, I just did not travel for business in 2020 because of the Covid-19 restrictions and I also cut back on advertising.

The decline of advertising nationwide showed up in my revenue. My Google Adsense revenue dropped by 35 percent as advertisers either stopped advertising or reduced what they were willing to spend per ad click. My book sales were cut in half as there were no speaking engagements that are the primary driver for book sales.

Insurance commissions increased by approximately $9,000 in 2020, about 17 percent. The increase of insurance revenue was tempered by losing one of my small group clients and several individual and family clients moving into Medi-Cal. The loss of business was counter balanced by enrolling several families who lost employer group health insurance from Covid-19 lay-offs and Medicare.

For some reason, I had several clients who aged into Medicare in 2020. Both Medicare Supplement and Medicare Advantage commissions are much better than individual and family commissions, which are the bulk of my revenue. I feel I got lucky in 2020. Even though the trend in revenue was down from book sales, advertising, and commissions, I was fortunate to pick up some Medicare enrollments that bridged the IFP commission decline in 2020.

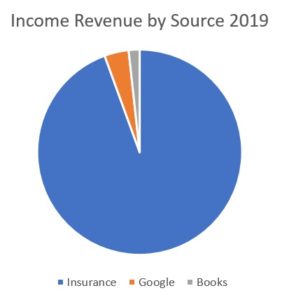

2019 Revenue Drops Thanks to California

I have learned to take nothing for granted when your primary source of income is from insurance commissions in California. My 2019 revenue decreased by 8% from 2018 and my expenses increased 15% in 2019. Gross revenue from insurance commissions, advertising, and book sales was $60,485 for 2019 compared to $65,727 for 2018.

There were two drivers of revenue reduction in 2019. First, California made short-term medical insurance policies illegal in California. (As if trying to provide health insurance for your family was a criminal act.) In 2018, I wrote many short-term medical policies as a bridge until open enrollment for numerous families and individuals. In 2019, people just went without any health insurance protection.

The second revenue retard was Kaiser. For individual and family plans, they pay $100 per person for the calendar year. Renewals are $50 per person. I had a lot of people who reluctantly switched to Kaiser in 2018 because the rates were cheaper and health insurance is too damn expensive. In 2019, the commissions from those 2018 enrollments was cut in half. Covered California keeps saying they are working to stabilize the insurance commissions for agents, but I see no movement in that direction. The commissions paid to agents continues to fall in the individual and family market place.

Online advertising revenue from Google increased slightly in 2019. This was a combination of more daily visitors to my website and some subtle changes to ad placements on my website. I was kind of surprised the ad revenue increased at all. I am very concerned with the viewer’s experience on my website. Consequently, I avoid any intrusive pop-up advertising or gifs that detract from reading or listening to the content. My rule of thumb is, “If I don’t want to see those sorts of ads, then I doubt my viewers want to see them.”

As expected, my expenses stayed relatively flat. While my expenses increased by 15% ($13,456 for 2019 v $11,380 for 2018) there were good reasons for it. There was some inflation for services. The cost of my server for hosting my website went from $1,000 to $1,200 per year and an assortment of applications used on my website – primarily for security purposes – also increased. The biggest category of expense pertained to my latest book. I logged numerous expenses related to the researched and production of “Benjamin Norton Bugbey, Sacramento’s Champagne King”.

In 2019 I also spent more money on some other marketing avenues for my business. But the print advertising and booths at consumer trade fairs yielded no results. A low cost, but labor intensive, marketing effort has been learning to create podcasts. The equipment was only a couple hundred of dollars, but there are hundreds of hours just learning the software, creating the content, then editing final version for publication.

I am not happy with my podcast and video production for either my health insurance or history posts. This means I will probably spend more money to upgrade my equipment for better sound quality in 2020. Preliminary views and comments regarding the podcasts and videos have been positive, so I will probably at least try to create a few more posts. Thus far, I have my online content has led more people to call me than the tradition print or in-person marketing efforts.

2020 was the year I was hoping to replace my 2002 CRV with 285,000 miles on it for new hybrid car. I don’t feel particularly optimistic about any significant revenue gains in 2020. While I picked up some new clients for 2020, I also lost just as many who have decided that health insurance is just too expensive.

What is my strategy for 2020? Follow my gut. I am not good at tracking what marketing efforts generate leads and enrollments. I do have a very global picture in my mind from reviewing commission statements, Google Analytics, and talking to people on the phone. By far the most numerous unsolicited comment from people who contact me is, “…I was reading your website and wanted to ask a few questions…” My gut tells me to stick with the partner who brought me to the dance, which is the world wide web.

ACA meant larger market for health sales

The ACA increased the overall market for health insurance by making it affordable to more individuals and families with the tax credits along with the removal of denying a person health insurance based on pre-existing conditions. That was good for agents. There are more people who want, qualify and can afford health insurance. The downside for agents is the four-fold increase in knowledge they need to have to properly navigate the health insurance market exchanges.

Health insurance agents must know more than just insurance

Whereas before the ACA the most daunting challenge an agent faced enrolling people into an individual and family plan were the five pages of health questions a client had to answer before submitting the application. Now there are no more health questions, but agents must be knowledgeable concerning the different conditions that make a household eligible the ACA tax credits such as citizenship documentation, definition of a household, and what is to be included in the Modified Adjusted Gross Income. This is if the individual or family enrolls through an exchange like Covered California. Off-exchange plans don’t require that expertise and some agents have decided to only sell off-exchange plans.

Expert in enrollment website problems

Another layer of necessary knowledge involves learning the application and enrollment software of the Marketplace exchange such as Covered California. Every month seems to bring a new wrinkle, page, or process to some of these enrollment websites as the exchanges update the software to fix glitches or add functionality. Then an agent also needs to keep abreast of all the provider and health plan changes that the health insurance companies make throughout the year. Of course, all this knowledge is in addition to the basics of health insurance like understanding deductible, copayments, coinsurance, PPO, HMO, EPO, HSP, and the new pediatric dental and vision benefits.

Health insurance commissions are dropping

While the overall work of the health insurance agent has increased, along with the potential market for new clients, the commissions paid by the health insurance companies and health plans has decreased. This is true in both the individual and family plan and small group market. Commission structures range anywhere from 1% to 5% for individual and family plans and 5% to 7% for small group plans. Many carriers have also instituted a declining commission structure such that the commission decreases after the initial enrollment year. The commission structure is regardless of whether the client enrolled through Marketplace exchange or off-exchange directly with the carrier.

Carriers play games with commission structures

If the commission structure is based on a percentage of the premium, it is calculated on the full monthly health insurance premium amount and not the tax subsidized amount the client pays. Some carriers also pay a higher commission for some plans like a Bronze or Silver and a lower percentage on Gold or Platinum plans. Part of the reasoning is that the premiums for the Gold and Platinum plans are higher- resulting in higher commission payments -, and these plans also have higher utilization rates. In other words, individuals purchasing higher benefit plans tend to use more health care services making them less profitable for the carriers. In 2014, one carrier just stopped paying commissions on new enrollments of the higher benefit plans to discourage their sale.

Flat rate compensation

Some carriers have abandoned a percentage based commission structure and moved to either a flat amount per member per month (pmpm) or a flat dollar amount for the initial enrollment. One carrier starts out paying $18 pmpm for the first year, and then drops down to $12 pmpm for all subsequent years. Another carrier pays a $100 one-time-payment for the entire year and $50 upon renewal in the following years. There are instances when the flat rate beats a percentage commission structure. One percent on a $800 monthly premium yields an annual commission of $96.

2018 Health Insurance Commissions

Health Net announced they were changing their commission structure of approximately 2% on IFP to a flat $14 per member per month. There explanation was that their new parent company Centene’s computer program can’t handle commission percentages. Blue Shield announced they were dropping their PPO plan commissions from 2.5% down to 1.4% for new members and 1% for renewing member. The HMO products would be 2.4% for new members and 2% for renewing members. Anthem Blue Cross, who has left most of the state for 2018, announced they would drop their compensation to $9 per member per month for both new and renewing members.

The health plans pay Covered California a 4% fee on the total premium amount for all enrollments that go through the Covered California enrollment system.

Be your own boss

Independent insurance agents, such as myself, are considered self-employed. I receive 1099s from the different carriers who paid me commissions throughout the year. Even though many agents have complained they didn’t get paid all their due commissions from enrolling individuals and families through Covered California, my less-than-perfect bookkeeping indicates that I received 99% of the commissions owed to me. The one exception is a small group I have through Covered California’s SHOP where I only received three months of commission in 2014. As of April 2015, I’m still waiting to be paid the balance of 2014 and commissions for 2015.

I earned over the federal poverty line for income

I have a small book of business relative to other independent agents. Most of my clients are individuals and families (approximately 180 households) and a few small groups. Less than 5% of my health business is from Medicare Advantage or Supplement plan enrollments. Total commissions from all lines of my health insurance business in 2014 were $29,823. In addition, I had another $2,000 of income from contract work where I write blogs for other websites. After I subtracted all the expenses, my 2014 Schedule C business income listed on my tax return was $23,524. The Self-Employment tax I had to pay was $3,324, or 14%, on my net business income.

Some health agents are earning good money

From the calculations I did in 2014 I estimated that the health insurance companies and health plans were paying about $9 million dollars in agent commissions per month on individual and family plans. Obviously there are some agents making a lot more money than I am as a health insurance agent. And that is just fine. Your income is proportional to the amount of effort invested. My primary marketing vehicle is my website. Agents with a general agency that has a store front, use direct mail advertising, or have other lines of insurance such as home and auto, most likely have a larger book of business and commissions than I do.

Health insurance, work smart and hard work

From my perspective, I feel like I have worked very hard to earn the commissions I received. First, I invested innumerable hours developing my website and then producing quality blogs that attracted readers. Those readers turned into clients. Secondly, I spent a tremendous amount of time working for clients to make sure they received the tax credits they were entitled to. Finally, there is far more work than most people realize when it comes to supporting and advocating for the client in terms of billing or provider problems at the insurance company level.

I need to diversify

I am not complaining. Health insurance has been good to me. I’m able to really help people and make a little bit of money doing it. There are careers that are far more lucrative. And the better path is to diversify so that as an agent you sell not only health but other lines like home and automobile as well. (Commissions on the property and casualty side are quadruple that of health insurance). If you decide to tackle health insurance be prepared for a substantial amount of time providing client service on issues that have nothing to do with the actual insurance.

2018 Knauss Income

2018 did not see a big increase in my overall income. The health insurance market commissions stayed relatively low. As in years past, the bulk of my income came from individual and family enrollments through Covered California and off-exchange enrollments. I saw a slight up tick in small group enrollments, but Medicare Supplements and Medicare Advantage enrollments were flat.

My total gross revenue was $66,230 for 2018. Of that amount, $62,460 was directly from commissions on health and life insurance enrollments. The remaining amount was split between book sales and advertising revenue generated by my website. My expenses were $11,400 for a net taxable income amount of $51,060. Of the expenses, I spent $2,000 on marketing such as sponsorships for an LGBT Senior Expo and advertising in a LGBT Sacramento newspaper, Outword.

The other large expense category was maintenance of my website and online communications. The server alone to host my website is $1,000 per year. The remaining costs were associated applications and security software to encrypt communications (HIPPA compliance). At this point, I don’t see my income or expenses dramatically changing in 2019, but only time will tell.

2017 Insurance Commission Income

2017 was my best year yet for commission income from health insurance enrollments. I realized $53,000 from commissions paid on IFP, small groups, Medicare, dental, and vision enrollments. Approximately 80% of the commission income was from the IFP market and the rest split between small group and Medicare. The revenue from advertisements on my website increased and I actually made a little bit of money on a book I published in 2016.

My Schedule C net revenue was approximately $44,000. I only had about $12,000 in expenses to reduce my gross income. In 2016 I had the cost of the printing my book to deduct and I purchased some office equipment. I did spend a lot of money in 2017 because I have become so nervous about 2018.

The health insurance companies have further slashed commissions. Blue Shield is 1.4% on PPO IFP plans. Blue Cross pulled out of most of California and they dropped their commission rate to $9 pmpm for 2018. I did not really increase my book of business as new clients replaced other individuals and families who left for employer sponsored health insurance, Medicare, or Medi-Cal.

IFP health insurance does not pay. The commissions are too low and trying to service just a couple of clients with problems with Covered California or the carrier eats up so much time that you are going backwards. Fortunatley, I’m writing another book so maybe I can get away from insurance commissions as my main source of income. 2018 looks thin and 2019 could be even worse.

2016 Insurance Agent Income

2016 was a slightly different year in that I did try and diversify my income. I published a book of local history in August of 2016. However, the expenses to publish the book far outstripped the revenue I was able to generate in Q4 of 2016. My gross health insurance commissions from individual and family plans, small group, Medicare, dental, and vision insurance was approximately $43,900. I incurred $13,800 in expenses directly related toward the health insurance business for a net taxable income of $30,100 for 2016.

Without doing a analysis of the proportions, I’m guessing that 80% of the commissions were for individual and family plans, and the remainder was from small group and Medicare enrollments. the 2016 commissions were up about 15% from 2015. The open enrollment period allowed me to realize a net increase in clients. I lost some families to Medi-Cal and others picked up group insurance. There was also a noticeable shift from Anthem Blue Cross to Blue Shield plans. This will most likely help my gross compensation as Blue Shield pays a percentage of the total premium for the commission whereas Blue Cross has a set per member per month amount.

I have no idea what Trumpcare will look like of if the carriers will even have the insurance agent marketing channel. But I’m working on another history book to further diversify my income.

October 2015 updated

Since I wrote this post back in April the compensation landscape for agents has continued to deteriorate. It wasn’t a big surprise, but Covered California will not renew the token $58 per person compensation that agents used to receive for assisting with the Medi-Cal determination for individuals. Anthem Blue Cross announced they are dropping their per member per month agent compensation from $18 to $16 for the first year. They are keeping renewal compensation at $12 per member per month. (They pay Covered California $13.95 per member per month for each individual enrolled in a Blue Cross plan through Covered California.) Cigna informed agents that they will not pay any commissions on new Silver, Gold, or Platinum enrollments for 2016. Bronze plans will receive a 5% commission. Western Health Advantage told agents that they are splitting their commission structure. Agents who enroll consumers in WHA plans through Covered California will receive $22 per member per month. That same individual enrolled in the same plan off-exchange, or directly with WHA, will receive a 5% commission.

2015 Commission Income

Over the long New Year’s holiday I was able to do some preliminary calculations of my earnings as a health insurance agent for 2015. Income from health insurance commissions will be approximately $38,177. That includes IFP, Small Group, Medicare, Medi-Cal compensation and a little bit of commission from dental plans. I had another $3,000 of income from a combination of website traffic and payments for writing content for other websites. My estimated expenses for 2015 are approximately $6,562 which includes E&O insurance, website costs, mileage, marketing, office supplies and telephone bills. This nets out to approximately $31,615 for 2015, this may change after I complete my schedule C later in 2016.

While a net income of $31,615 for 2015 looks like a big jump from the $23,524 of 2014, I have to remember that Covered California finally paid me back commissions they owed me for 2014. (See Covered California SHOP fails to pay commissions). On this net income I paid $5,875 in estimated quarterly tax payments to the IRS.

Even though the commission structures are being eroded down to minimum wage levels, I think 2016 will be very similar to 2015 if not a little bit better. I’m starting to pick up a few more dental plans and small groups that help take the edge off of the declining commission rates for individual and family plans. Regardless of any increase I receive in commissions for 2016, I wouldn’t recommend a career of representing health insurance companies to anyone. Agents are destined to be replaced, not by choice but by design, with online enrollment portals and call center staffers who know very little about how health insurance actually works.

The future of agents

As I expressed to the Board of Covered California at their October meeting I’m most concerned about the deflation of agent commissions. The health plans and insurance companies are slowly forcing agents out of the market. These are the same folks who are responsible for over 40% of the enrollment through Covered California. For every consumer who enrolls directly with a carrier or through Covered California without the assistance and support of an agent saves the health plans money. No one cares that without agents, consumers don’t have an advocate to sort through the confusing mazes known as Covered California and health insurance.