Covered California consumers may see an increase in subsidies because of Blue Cross exit from market.

Californians who receive the monthly tax credit subsidy from Covered California may be negatively impacted in 2018 because Anthem Blue Cross is leaving the market place for individual in family plans in many regions of California. This is because the monthly subsidy individuals and families receive from Covered California is tied to the Second Lowest Cost Silver Plan (SLCSP) available to them. If the absence of a Blue Cross plan results in a lower (SLCSP), then the monthly subsidy that all households receive will be lower.

Blue Cross Exit May Impact Tax Credit Subsidy

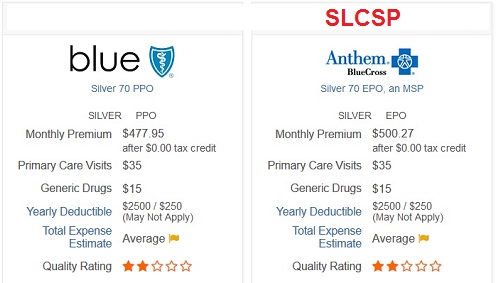

The Advance Premium Tax Credit or monthly subsidy from Covered California is based on making health insurance affordable. Specifically, the Affordable Care Act formula looks at making the Second Lowest Cost Silver Plan affordable for a household’s size and income. In simple terms, if the ACA formula determines a household should spend no more than $300 dollars per month on health insurance, and the SLCSP is $400 per month, then the individual or family is eligible for a $100 monthly Advance Premium Tax Credit to lower the cost of the insurance.

It doesn’t matter if the household selects a Bronze, Silver, Gold, or Platinum plan, if the ACA calculation determines they are only eligible for $100 that is all they get. They can apply the $100 to any health plan in any metal tier, with the exception that the tax credit can’t be larger than the actual insurance rate, which can happen with some Bronze plans.

Age & Overall Rate Increases

There are two forces that contribute to an individual’s rate increasing every year. First, the rates go up every year because we are a year older, with the exception of people under 20 years old. Second, the health plans increase their rates to account for the increased costs of health care, pharmaceuticals, and utilization. In past years, the SLCSP silver plan helped and hurt consumers. For example, some people were helped when the SLCSP had a rate increase larger than the increase due to the increased age of the consumer.

I had several clients who actually saw their monthly health insurance premium decrease in 2017. They had selected the SLCSP that happened to be a Kaiser plan. The Kaiser plans in their region increased 8%, but their age related increase was only 4%. Because the monthly tax credit subsidy was tied to the SLCSP that went up by 8%, which increased their subsidy, the greater subsidy amount offset the increased rate because of their age.

But the reverse can also happen. I have clients where the SLCSP Silver plan only went up by 8%, but their Anthem Blue Cross plan, which wasn’t the SLCSP, increased 15%. When coupled with the increase for their age and the lower tax credit based on the SLCSP, some consumers saw their rates really jump in 2017. The increase was larger than anything Covered California published as the weighted average increase for people in their region.

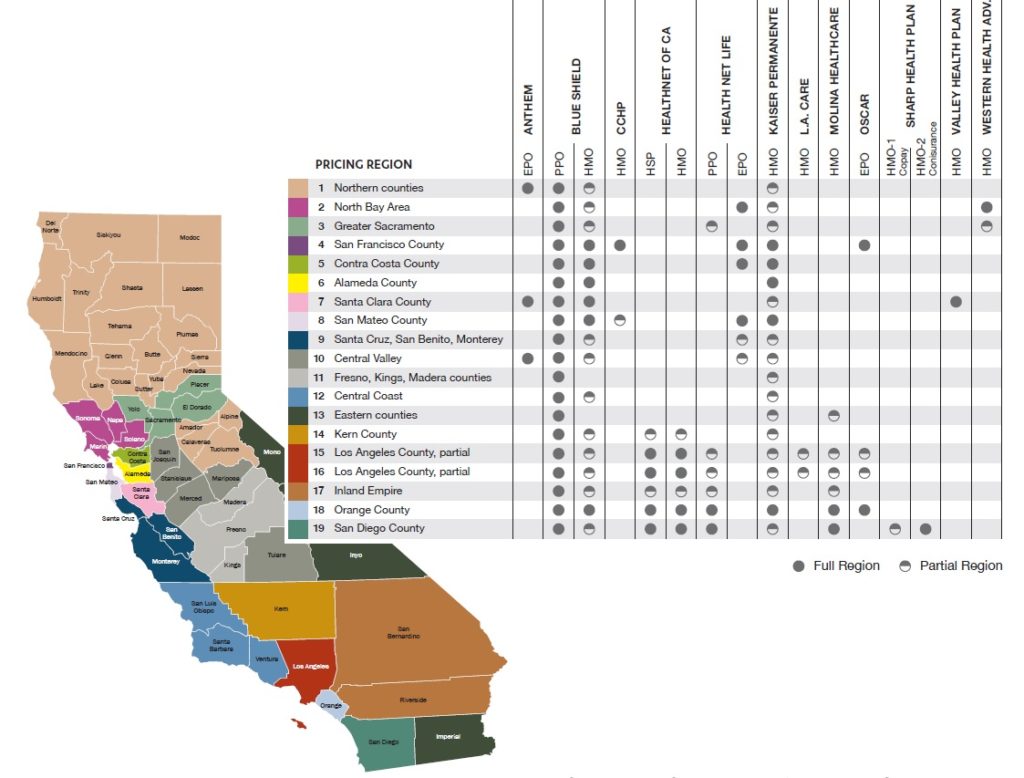

From my experience Anthem Blue Cross was rarely the SLCSP plan in most regions. The SLCSP plan is not based necessarily on region. It is based on the consumer’s zip code. Not all plans are available in all zip codes of a region. This frequently happens when a carrier such as Kaiser only services part of a county. The Covered California chart may show Anthem Blue Cross, Blue Shield, and Kaiser as available health plans. But in some zip codes, where Kaiser is not available, consumers may only have had Blue Cross or Blue Shield as choices.

2018 Covered California regional map with table of individual and family health plan carriers.

If a consumer was in a market where the only choices were Blue Cross and Blue Shield, and Blue Cross was the SLCSP (Blue Shield necessarily being the least expensive Silver plan offered) then these consumers may see their relative tax credit subsidy decrease. This will hold true if the Blue Shield plan, and now the only plan available, continues to have a rate lower than what Blue Cross would have had in 2018.

The Second Lowest Cost Silver Plan determines the amount of monthly tax credit subsidy for ACA.

However, in regions where Anthem Blue Cross will continue to offer plans (Regions 1, 7, & 10) they may become the SLCSP if they significantly raise their premiums. Anthem Blue Cross doesn’t even want to be in the California market for individual and family plans, perhaps the most stable IFP market in all of the U.S. But if Blue Cross really inflates their rates to either make money or dissuade enrollment, that will float up the subsidy for all consumers in that region when the only two choices are Blue Shield and Blue Cross.

Of course, in regions where Blue Shield was more expensive, and is now the only carrier, the SLCSP rate will increase – assuming that Blue Shield doesn’t have a drastic rate reduction. This will provide a greater tax credit – all things being equal such as household size and income. Even though every family’s situation is unique and income changes from year to year, in many instances, the loss of Anthem Blue Cross should not adversely impact the relative size of the monthly tax credit for most households. But where Blue Cross is the SLCSP, with potentially significantly higher rates than Blue Shield, people enrolling in Blue Shield plans will see even lower monthly rates because the subsidies will be higher.