The Social Security Administration uses several different calculations to arrive at your monthly benefit deposit. There is your historical earnings record, revising past income upwards, and then bending your average monthly earnings into a benefit amount. I will use my own earnings record to illustrate the various steps to arrive at my estimated Social Security monthly benefit of $2,744.

Steps to Calculate Your Social Security Benefit

The age of 62 is the magic number because it is considered the retirement age. The year we turn 62 cements some of the dollar amounts used in the benefit calculation. These set numbers are the indexed historical earnings and the bend points. Even if you don’t file for Social Security until you turn 70 years old, the foundation of the income is based on the year you turn 62 years old.

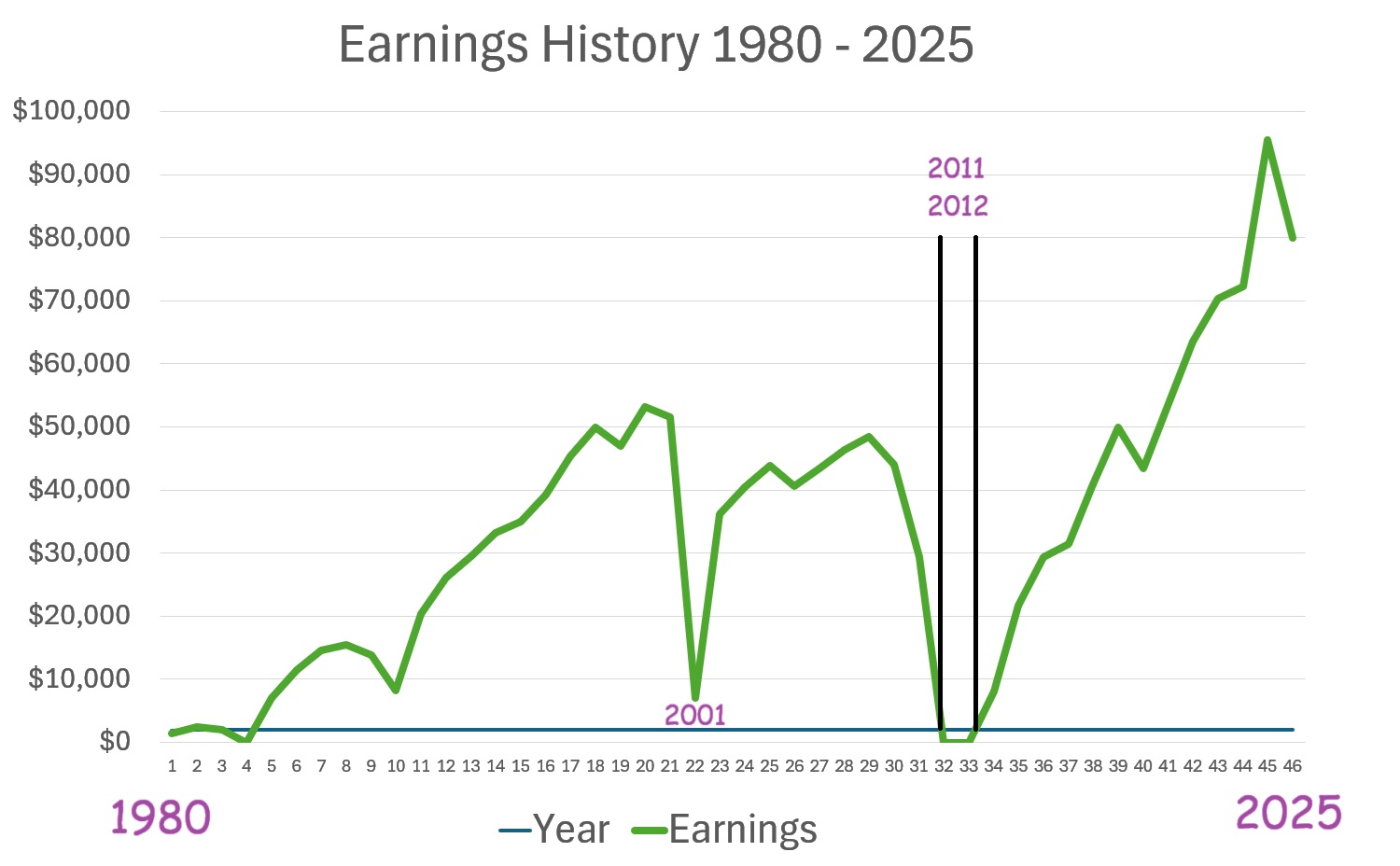

The first step the Social Security Administration (SSA) takes is adjusting your past income. For me, my first reported income on a federal income tax return was 1980. Some years I had no income. Regardless, all the past earnings need to be adjusted or indexed upwards.

Indexing Historic Earnings

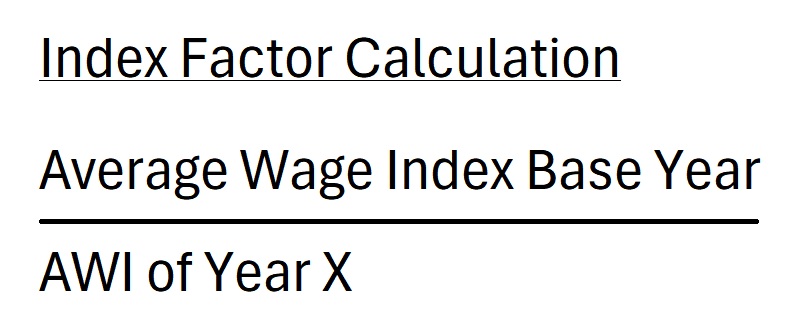

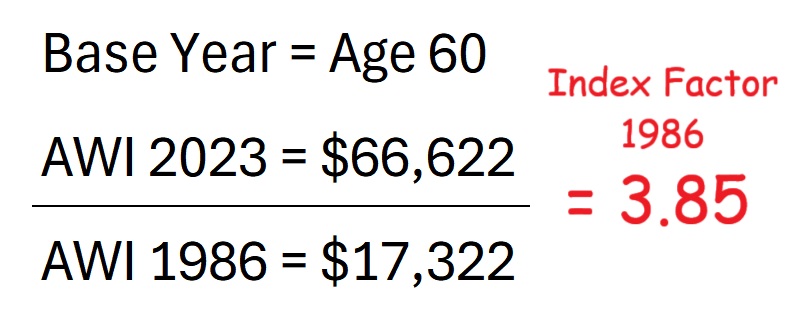

SSA uses the two years prior to your 62nd birthday as the base year. I turn 62 in 2025. I turned 60 in 2023. My base year is 2023. The SSA uses the National Average Wage Index for your base year divided by the Average Wage Index for the year that needs to be adjusted.

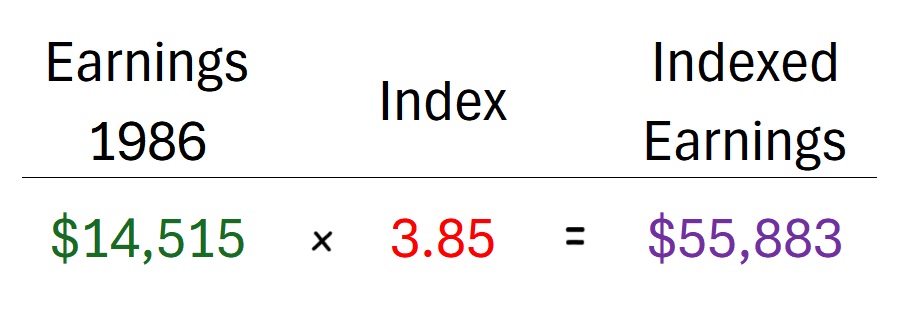

For example, the Average Wage Index (AWI) for 2023 is $66,622. The Average Wage Index for 1986 is $17,322. The base year divided by the specific AWI for the year in question yields the index factor. In the case of 1986, the index factor is 3.85.

That means that whatever my income was in 1986, it is multiplied by 3.85 to get the indexed earnings. My $14,515 income of 1986 is converted – indexed – to $55,883.

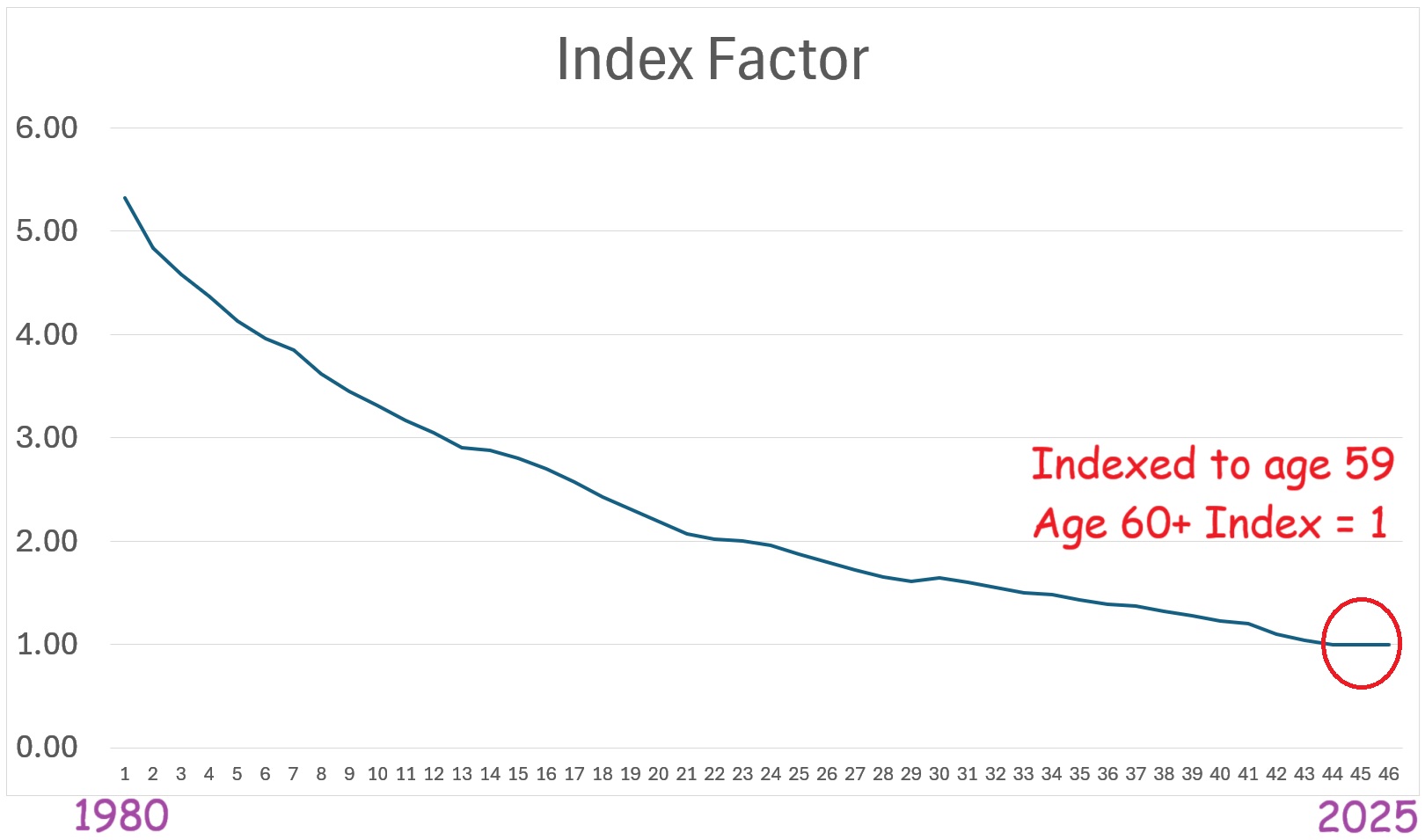

The index curve decreases, the index number gets lower, as you approach the base year. The base year and all future earnings have an index factor of 1, meaning they are not adjusted upwards. However, they will be adjusted for inflation before you file your claim.

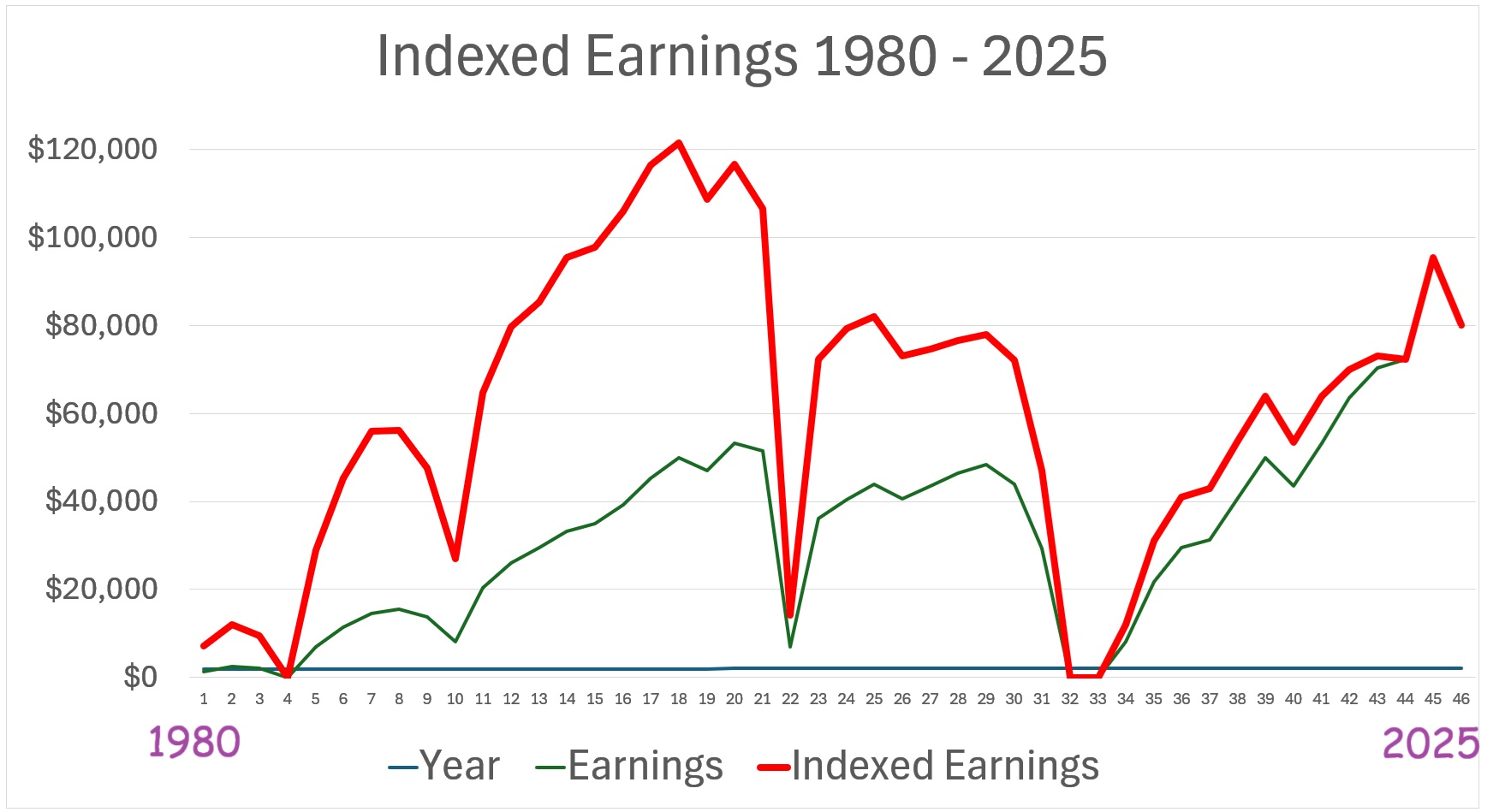

You can see how my historical earnings were boosted by the index factor. Note how the last couple of years have very little upward adjustment as the index factor approaches 1.

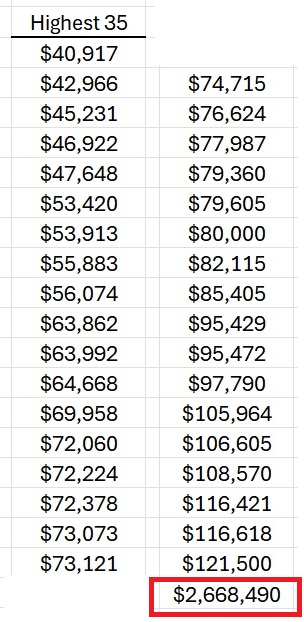

The next arbitrary step in the SSA process is to find the highest 35 years of indexed or adjusted earnings. Oddly, some of my highest indexed earnings occurred from 1990 through 2000.

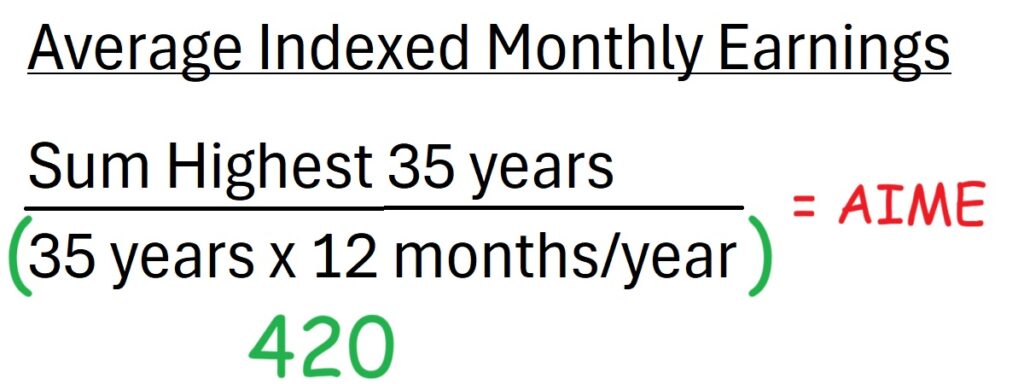

Calculating Your Average Indexed Monthly Earnings

Finally, SSA totals the highest 35 years of indexed earnings and divides the sum by 420 (35 years x 12 months/year) to get the Average Indexed Monthly Earnings (AIME.)

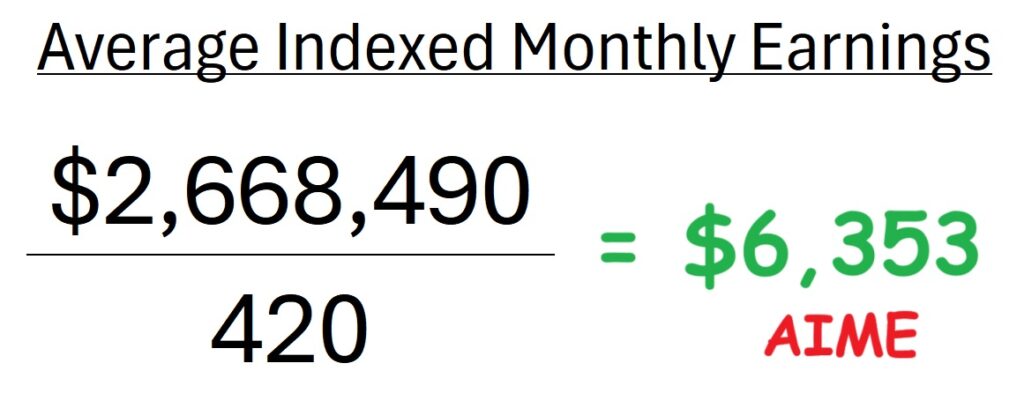

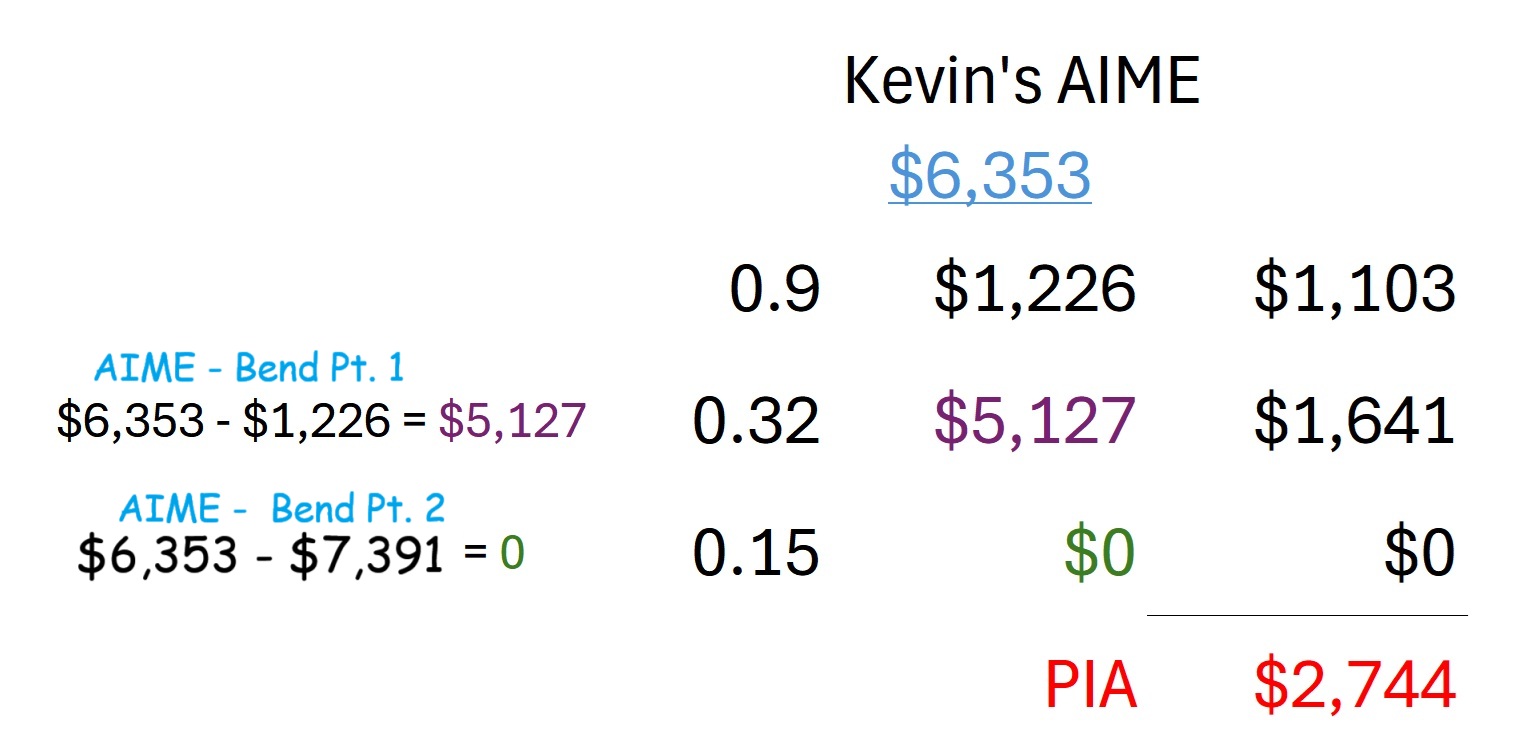

My 35 years of indexed earnings total $2,668,490. When divided by 420, my Average Indexed Monthly Earnings is $6,353.

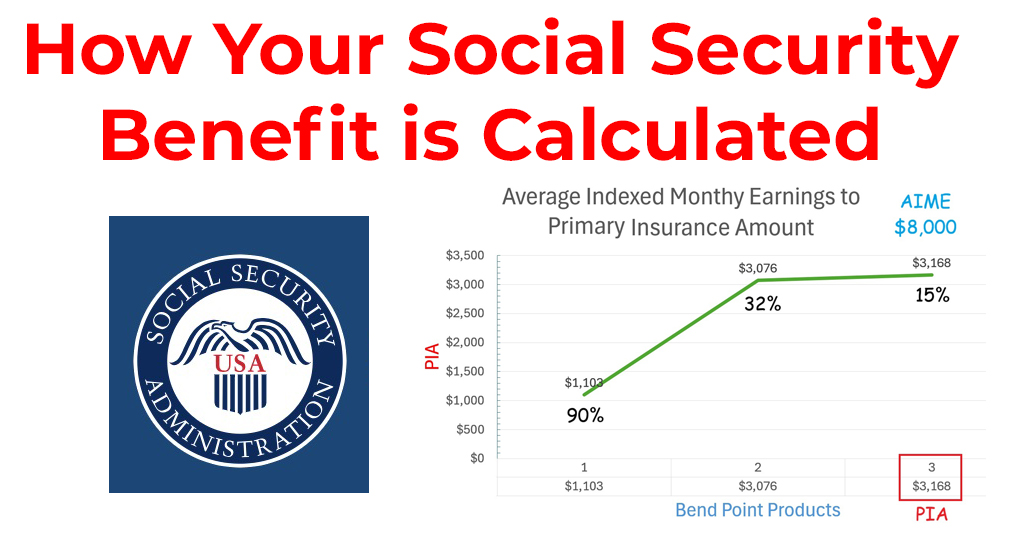

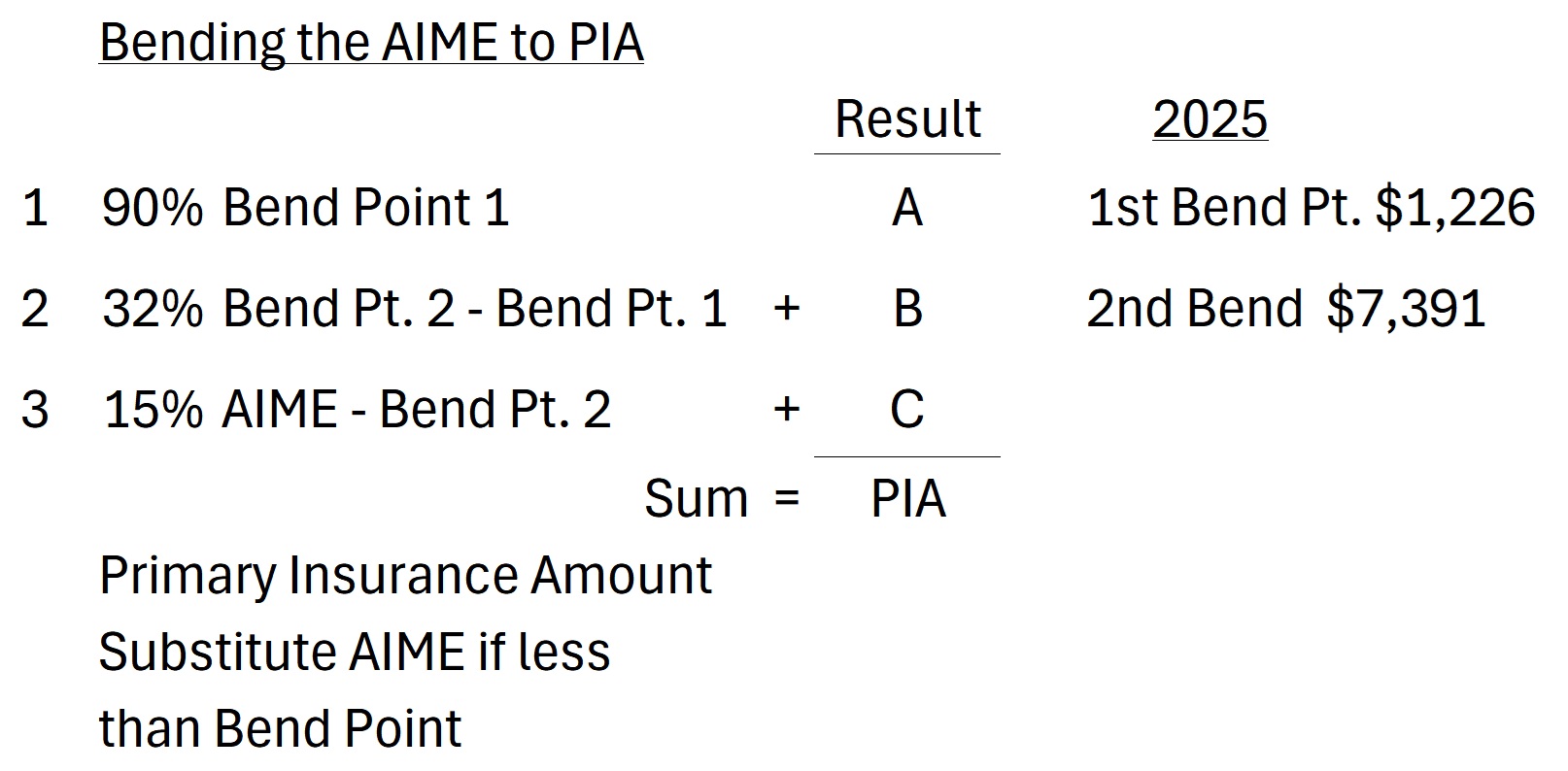

The next set of calculations are truly mind bending. The SSA has to bend your AIME into a Primary Insurance Amount (PIA.) The PIA is what you will receive at your Full Retirement Age, 67 if born in 1960 or later. The AIME is bent lower by a series of calculations using Bend Points. The specific Bend Points are from the year you turn 62.

Bend Points to Reduce Your AIME

My Bend Points are $1,226 for the first point and $7,391 for the second point. If your AIME is lower than the Bend Point, it is used instead of the set point. The three-step calculation applies 90%, 32%, and 15% to the Bend Point and AIME. When the three products are total, the result is the Primary Insurance Amount.

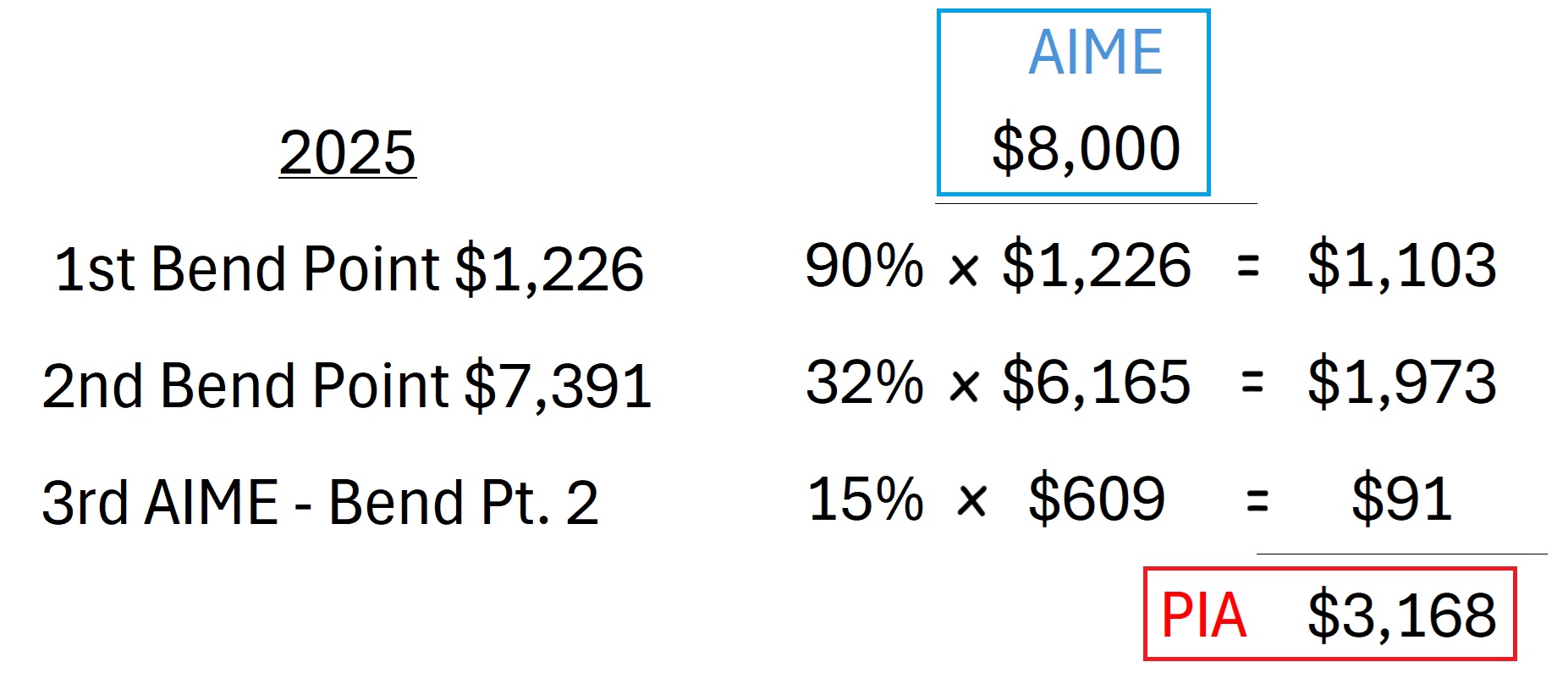

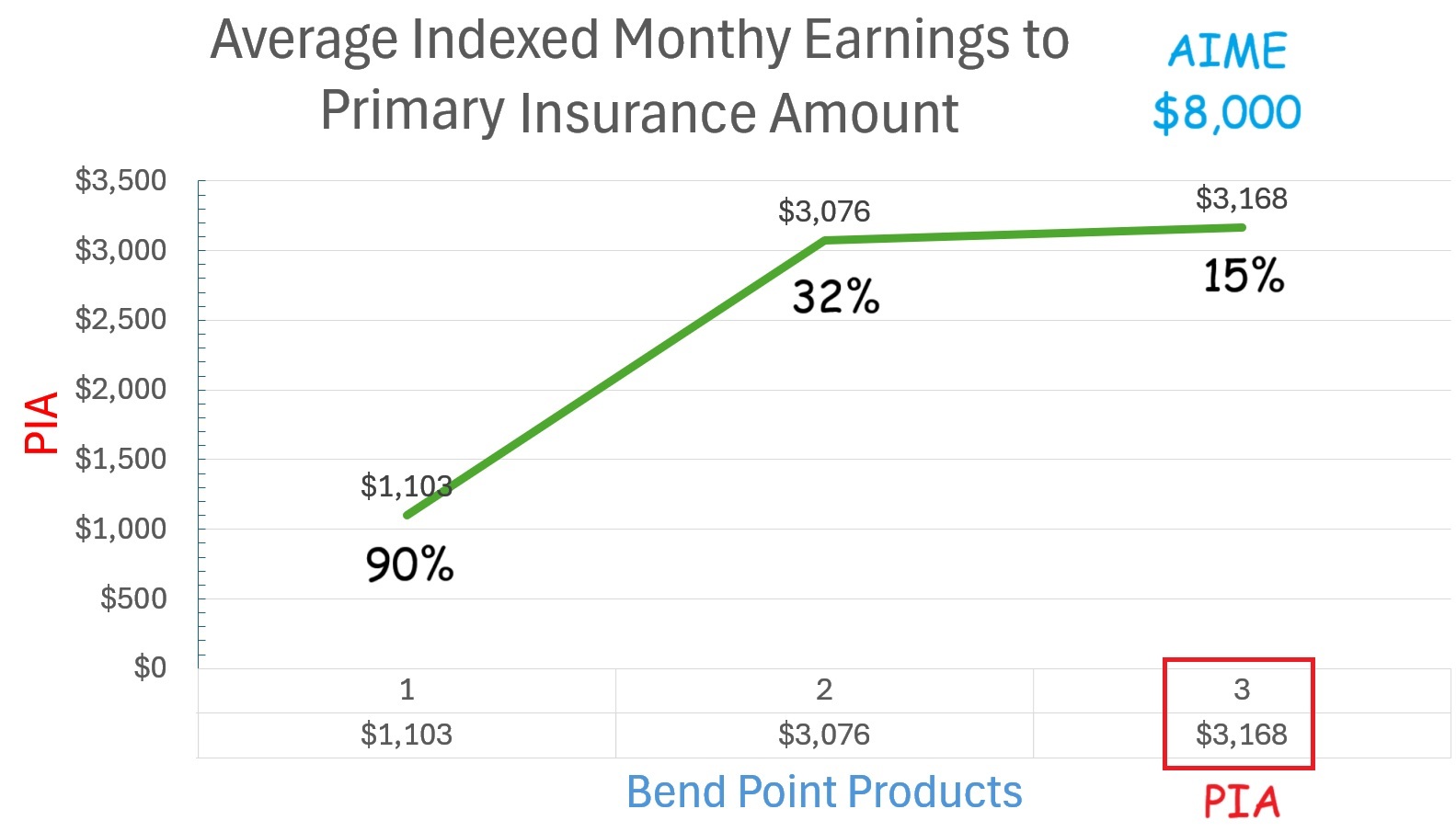

For example, if your AIME was $1,000, less than the first Bend Point of $1,226, the SSA would use $1,000 times 90% for a product of $900. In the example below, an individual has an AIME of $8,000. When you go through the math, the result is a PIA of $3,168.

Graphically, this chart shows how the $8,000 AIME is bent down at the various points to yield the final $3,168 Primary Insurance Amount.

My AIME is only $6,353. I get the full 90% of Bend Point 1, $1,103. Because my AIME is less than the second Bend Point of $7,391, the second step is my AIME minus Bend Point 1. Multiplied by 32% another $1,641 is added. I have no third calculation because my AIME minus Bend Point 2 is zero. When it is added up, my PIA is $2,744.

How to Increase Your Primary Insurance Amount

If I file at age 67, assuming future earnings are not high enough to be added to the AIME, in today’s dollars, I will collect $2,744. If I file for Social Security at age 62, I will receive 70% of my PIA or $1,921. If I wait until I’m 70, I receive 124% of the PIA or $3,402. Again, these amounts are before any Cost of Living Allowance (COLA) or higher earnings.

Of course, if I continue to work, which I need to do, future earnings could bump up my AIME resulting in a little higher Primary Insurance Amount. There will also be COLAs to the PIA. Unfortunately, the COLAs reflect inflation and may not result in any increased buying power for the higher monthly Social Security deposit.

YouTube video where I explain the Social Security benefit calculations as the ocean waves crash in the background.