Health insurance companies have a new way to deny coverage; they restrict the plans and the providers. Always three steps ahead of any government regulation, health insurance companies in California have sought to protect themselves from unexpectedly high claims from new members in Covered California health plans by creating “light” provider networks and introducing Exclusive Provider Organizations. However, the Affordable Care Act helps shield health insurance companies from excessive claims with special provisions such a reinsurance and risk corridors.

Restricted networks are the new underwriting guidelines

The hard cruel fact of the new guarantee issue health insurance is that health insurance companies have rigged the plans to help contain their costs. The first rope around new members was learning that the doctors they have seen for years weren’t included in the new provider networks. This has led people to scramble to find new doctors or begin switching to a health plan that does include their physician. Either the physician wouldn’t accept the new reduced reimbursement rate for office visits or the insurance company cut them out because the doctor was associated with a high cost hospital.

Preventing out-of-network claims

Residents in the Bay Area and Southern California are finding they no long have access to a Preferred Provider Organizations (PPO) but are only offered the Exclusive Provider Organization (EPO) plan type. Similar to the HMO model, the EPO has no out-of-network coverage. Unlike a PPO plan where the member could go out-of-network and pay a different deductible and coinsurance rate for health care services, the EPO restricts the member to only the selected doctors and hospitals in the new network.

I bill for a solo OB/GYN in one of the new Anthem EPO counties in Southern CA (we were previously contracted with Anthem as In-Network for PPO). I was just advised by an Anthem/Wellpoint rep over the phone that we were not invited to join the new EPO plans because the hospitals which we provide services at are not Tier 1. The problem is that all of the hospitals we’re near in our part of the county aren’t Tier 1, either, so a new Covered California plan Patient has to go into the city to find an In-Network provider, as well as a Tier 1 hospital. They can’t use any of the providers or hospitals in their backyard, because they’re not Tier 1. And, because it’s an EPO, there’s no Out-Of-Network benefits, either. – Shilo Stigen, Comment from Anthem Blue Cross tiers networks to save costs

Inconsistent rules between carrier networks

This is further complicated by how the different carriers have designed their EPO networks. Blue Shield of California has a separate network of only EPO providers that is separate from their PPO network. Anthem Blue Cross allows EPO members to see any “network” doctor, but created a tiered facility network where the member pays more if they choose a tier 2 hospital.

EPOs coral members in the pool

The common threads between the Bay Area and Southern California are a population with a higher average income and more “high cost” or prestigious hospitals. Families with money will seek the best and most expensive care even if it is out-of-network and the prestigious hospitals and clinics are willing to accommodate them. If someone is diagnosed with cancer what concern is the $9,350 maximum out-of-pocket amount when the treatment might cost $100,000 at a world renowned cancer center?

Restricted networks reduce claims expense for health plans

It’s the other $90,650 that the health plan has to pay that the insurance company is hoping to avoid. While they may not be able to side step paying for cancer treatment, they want to hedge their bets by excluding any hospital, clinic or doctor who can command their own price based on their reputation. Hence, we get tight networks, tiered networks and a gate on seeking health care outside the network with the EPO.

ACA provides for risk reduction

In addition to the cost containment of restricted networks, the Affordable Care Act further shields insurance companies from the exposure of shouldering unexpected claims. Written into the ACA are the three R’s: risk adjustment, reinsurance and risk corridors. The Kaiser Family Foundation produced an excellent Issue Brief on the three parts to stabilize insurance premiums and reduce risk for the insurers. (Download the KFF Issue Brief at end of post.) Each one of these federal provisions is meant to keep health insurance premiums stable and reduce the risk of excessive claims from individuals and families that have health challenges and may need expensive treatment.

The ACA’s risk adjustment, reinsurance, and risk corridors programs are intended to protect against the negative effects of adverse selection and risk selection, and also work to stabilize premiums, particularly during the initial years of ACA implementation. – Kaiser Family Foundation Issue Brief on ACA risk adjustment, reinsurance, and risk corridors.

Risk Adjustment, Reinsurance, Risk Corridors

The temporary and permanent rules are similar to revenue sharing that professional sport leagues employ. Similar to major market teams sharing their media revenue with smaller market teams to keep them competitive, the new rules have insurance companies sharing premium revenue from plans with a low incidence of claims with health plans experiencing higher than expected claims from new members.

Leveling the risk pool of members: Risk Adjustment

Risk Adjustment is a permanent provision within the ACA applying to all non-grandfathered plans in the individual and small group market. The membership pool of each health plan will be evaluated for its potential to generate higher or lower claims expenses based on the members health status. For example, if the membership pool of one Silver plan (Silver plans expect to cover 70% of the member’s health care expenses) is estimated to only have to pay out 65% for all their members, that plan will transfer money to a Silver plan that might be expected to incur 75% in claims expenses.

Avoid marketing to attract only healthy people

The disparities of the membership pool, and their associated health care expenses, can easily be created based on geography and demographics. Health plans sold in regions that may have an older population base will likely have more expected health care expenses than the exact same plan sold in a community comprised of families with young children. The risk adjustment is meant to allow insurers to focus on the the value of their health plans to new members as opposed to marketing to younger healthy prospects.

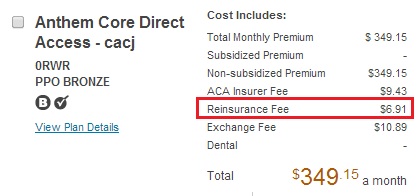

Back stop to wildly high claims: Reinsurance

The reinsurance program is a temporary provision that will run from 2014 to 2016. Reinsurance is the “back stop” for health insurance companies having to pay unexpectedly high claims for any one member. The reinsurance provision only applies to individual and family plans that for the first time in 2014 can not deny coverage or increase the premiums for people with pre-existing conditions. Small group plans have, for the most part, always been guarantee issue regardless of the health status of the applicant.

All plans pay into the reinsurance pool

The reinsurance, or insurance for insurance companies, is funded by all insurance companies contributing to the program. Individual and family plans that experience health care costs exceeding between $45,000 in 2014 and $70,000 in 2015 will be eligible for a payment from the fund. The goal of the reinsurance is to remove the unexpected claims expense prediction from the the formula for setting the premium rates.

Helping keep health plans stable: Risk Corridors

The final provision to help insurance companies keep their rates low is the temporary risk corridor provision. The risk corridor works in conjunction with the Medical Loss Ratio regulation that states that individual and small group plans must spend 80% of their premium revenue on patient care and quality improvement. The corridor is plus or minus 3% on either side of the 80% amount the insurance company is obligated to spend on health care expenses.

Some plans will pay and receive no payments

For example, if a health plan realizes claim’s expenses of less than 77% it will pay a portion of the difference between its projected and actual expenses into a fund to be distributed to health plans that experienced claims greater than 83% of its projected claim’s expense. If a health plan experiences claims between 77% – 83%, the risk corridor, they pay nothing and receive nothing.

Members pay twice: tight networks and reinsurance fee

Reinsurance fees should not restrict doctor networks.

When the insurance companies are having their risk for unexpectedly high health care expenses subsidized they should not have the luxury of creating tight doctor and hospital networks. The restrictions on network providers for cost containment purposes is exceptionally irritating when it is the plan members that are helping fund part of the risk reduction provisions by having to pay for the reinsurance fee on qualified health plans. Restricted networks and new EPOs are just a “work around” solution to allow health insurance companies to selectively limit health care like they have done in the past.

[wpdm_package id=172]