IRS P5187 guide to the ACA tax credits and penalties.

The IRS has published a taxpayer friendly guide to assist individuals and families with attempting to calculate their Affordable Care Act tax credits. The focus of IRS Publication 5187 Health Care Law: What’s New for Individuals & Families is on the Shared Responsibility Payment (individual mandate penalty) and calculating eligible Premium Tax Credits for 2014. Pub. 5187 is a high level overview of IRS filing requirements established by the ACA with details left to the specific forms to be filed with the federal tax returns. Download p5187 and other forms at end of post.

Shared Responsibility Payment

The Shared Responsibility Payment (SRP) is also known as the individual mandate of the ACA. There are numerous exemptions from having to pay the SRP from membership in a health care sharing ministry, incarceration, to financial hardships. Some of these exemptions can be claimed when filing your federal taxes and others must be granted by the Marketplace such Healthcare.gov or your respective state exchange. Taxpayers who are granted an exemption will receive a certificate number that they must report on Form 8962, Health Coverage Exemptions.

- Read more about filing for exemptions and calculating the penalty at Calculating IRS individual mandate penalty.

Real life: exemptions, penalties and tax credits

Typical of government forms and publications is a lack of real life experience. Undoubtedly there will be numerous individuals and families that face the scenario of being eligible for an exemption, are liable for a SRP penalty, and also qualify for tax credits. In these cases, the primary taxpayer for the household will have to file Form 8965 to report the exemptions and calculate the penalty, along with Form 8962 for reconciling either the Advance Premium Tax Payments from the Marketplace exchange or the tax credit refund on their 2014 taxes. These real life scenarios aren’t really addressed in the publication.

Reconciling advanced premium tax credits

The only way to be eligible to receive the ACA tax credits is to have purchased health insurance through the Marketplace in 2014. You either opted to have the estimated tax credits advanced to your health insurance company to lower your monthly premium or you decided to take the full tax credit when you filed your taxes. Publication 5187 goes through the type and amount of household income eligible for the tax credits. Unfortunately, the ACA has given us one more definition of income to consider – Modified Adjusted Gross Income – which is different from the regular IRS AGI.

A taxpayer’s household income is the total of the taxpayer’s modified adjusted gross income (MAGI), the taxpayer’s spouse’s MAGI if married filing a joint return, and the MAGI of all dependents required to file a federal income tax return.

MAGI, for the purpose of the premium tax credit, is the adjusted gross income on the federal income tax return plus any excluded foreign income, nontaxable social security benefits (including tier 1 railroad retirement benefits), and tax-exempt interest. It does not include Supplemental Security Income (SSI). – Publication 5187, Health Care Law: What’s New for Individuals and Families

Federal Poverty Line and Medicaid

The IRS ACA tax credit guide notes that in most cases taxpayers are eligible for the health insurance premium tax credit if their MAGI is between 100% and 400% of the federal poverty line (FPL). The exception is states that expanded Medicaid coverage. In California, only MAGI over 138% of the FPL is eligible for the tax credits. Incomes below 138% FPL received minimum essential government coverage through Medi-Cal. In addition, family incomes under 266% of the FPL in California automatically enrolled any dependent children in Medi-Cal kids making them ineligible to receive the ACA tax credits.

Employer sponsored group health plans

The issue of families being offered employer sponsored group health plan, making them ineligible for ACA tax credits, is referenced in the Publication 5187. The rules governing the affordability of employer sponsored health insurance are complicated. The IRS guide doesn’t really offer any new information. Many families have purchased health insurance through the Marketplace, either their state or federal exchange, but really aren’t entitled to the tax credits they are receiving because they are being offered employer group insurance.

If only one spouse is enrolled in employer coverage that is not affordable and does not provide minimum value, the non-enrolled spouse may be eligible for a premium tax credit.

An individual is eligible for employer-sponsored coverage for any month the individual is enrolled in the employer coverage or could have enrolled in employer coverage that is affordable and provides minimum value. – Publication 5187, Health Care Law: What’s New for Individuals and Families

Form 8962 Premium Tax Credit

Before you can start filling out Form 8962 to reconcile any advance premium tax credits you received with your final Modified Adjusted Gross Income you need to receive Form 1095-A from either the federal or state exchange you purchased the health insurance through. The 1095-A will list the total amount of the tax credits advanced on your behalf to your chosen health insurance company. If you opted NOT to have any tax credits applied to reduce your health insurance premium, it is unclear if you will receive a 1095-A.

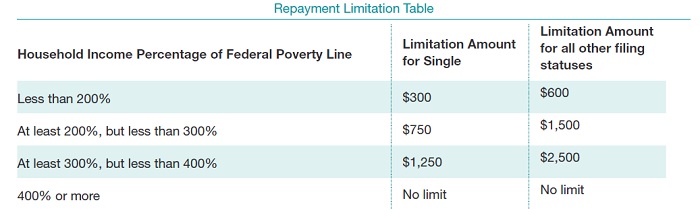

Limited repayment of ACA tax credits

The IRS guide lists a Repayment Limitation Table for households who had more income than they expected and received more Advance Premium Tax Credits (APTC) than they were entitled to. However, if the MAGI exceeded 400% of the FPL for the household size, indications are you will have to repay all APTC that was forwarded to your health plan. The only way to determine any applicable tax credit or repayment is to complete Form 8962. While the online tax preparation sites should be able to handle all of the information for the ACA tax reconciliation, they may not be able to easily handle all the different situations.

IRS ACA tax credit repayment limitation table.

Married, Divorced, Dependent

Some of the different situations noted in the IRS Publication 5187, listed as unusual situations by IRS definition, are for taxpayers who get married, divorced, or claimed as a dependent on someone else’s taxes. Even though the IRS qualifies these as unusual situations, they are part of normal life. Taxpayers who got married or divorced during 2014 will have additional work to reconcile any APTC with the new MAGI income for Married Filing Jointly, Single or Head of Household filing status.

No EZ filings

If you didn’t earn enough to file a federal tax return you can still file and claim the tax credit. However, regardless of whether you took advance tax credits or decided to take the credit when you filed your taxes, you won’t be able to use the 1040EZ form according to the IRS.

Premium tax credit. You may be eligible to claim the premium tax credit if you or your spouse enrolled in health insurance through the Health Insurance Marketplace, but you must use Form 1040A or 1040 to do so. You may also be eligible to claim the premium tax credit for any dependent you claim on Form 1040A or 1040 who enrolled in health insurance through the Health Insurance Marketplace.

Advance payments of the premium tax credit. Advance payments of the premium tax credit may have been made to the health insurer to help pay for the insurance coverage for you or your spouse. If advance payments of the premium tax credit were made, you must file a 2014 Form 1040A or 1040 and Form 8962. If you enrolled another individual in insurance coverage, advance payments of the premium tax credit were made for that individual, and no one else is claiming the personal exemption for that individual (for example, by claiming the individual as a dependent), you must file Form 1040A or 1040 and Form 8962.

Form 1095-A. If you or your spouse enrolled in health insurance through the Marketplace, you should have received Form(s) 1095-A. You may also have received Form(s) 1095-A if you enrolled another individual in health insurance through the Marketplace. If you received Form(s) 1095-A for 2014 for yourself, your spouse, or an individual you plan to claim as a dependent, file Form 1040A or 1040. Save any Form 1095-A you receive. It will help you figure your premium tax credit. If you received a Form 1095-A for an individual you do not claim as a dependent, you should provide a copy to the taxpayer who is claiming the personal exemption for that individual (for example, by claiming the individual as a dependent). If you did not receive a Form 1095-A, contact the Marketplace.

Instructions for 8962

As of the end of December 2014, the IRS had not released a final version of the instructions for Form 8962 Premium Tax Credit. Listed below are the draft instructions. As soon as they post them I’ll update this post and probably do a new blog post on the instructions for claiming the ACA tax credits.

[wpfilebase tag=file id=382 /]

[wpfilebase tag=file id=375 /]

[wpfilebase tag=file id=118 /]

[wpfilebase tag=browser id=64 /]