IRS Publication 974 gives all the details for reconciling 2014 ACA premium tax credit calculations.

Publication 974, released by the IRS in March 2015, is a fairly comprehensive review of the ACA health insurance premium tax credit rules. Its release is long overdue as many Americans have struggled to understand how the Advance Premium Tax Credits (APTC) afforded by the ACA interact with their federal taxes. Publication 974 addresses many different topics from calculating APTC with a marriage or divorce to the circular reference faced by self-employed individuals.

Download 974

[wpfilebase tag=fileurl id=624 linktext=’Premium Tax Credit Publication 974′ /]

Publication 974 premium tax credit guidance

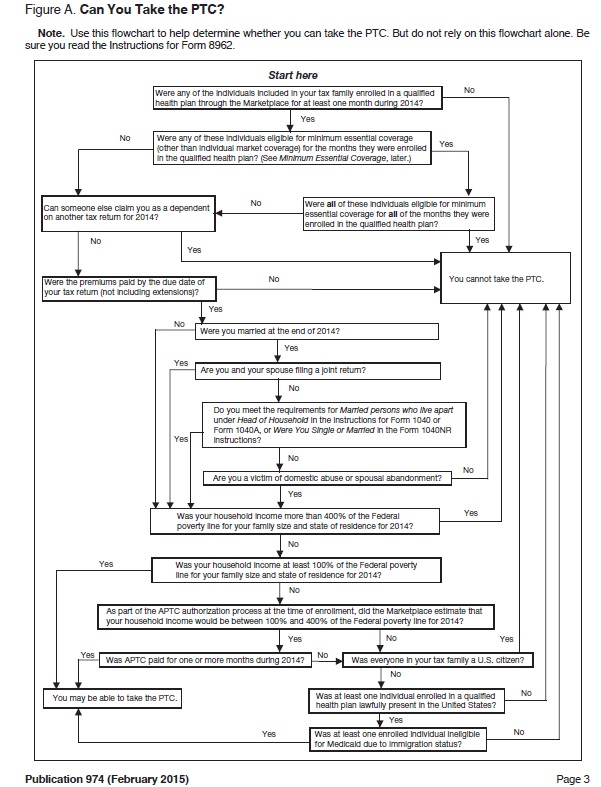

The complicated nature of the ACA Premium Tax Credits (PTC) is illustrated in the flow chart of Pub. 974 on page three. While the flow chart does a nice job of simply outlining whether an individual or household is eligible for the PTC, it assumes the reader has an understanding of Minimum Essential Coverage and the federal poverty lines. The publication makes every effort to explain many of the terms and conditions and gives examples as to when the conditions may trigger eligibility for the PTC.

State exchange rules can be different

Then there are the state specific rules that may alter the flow chart’s application. For example, one condition to receive PTC on the flow chart is that the household income was at least 100% of the federal poverty line (FPL) in which case the tax payer may be able to take the PTC. In California, the household income must be greater than 138% of the FPL. An estimated Modified Adjusted Gross Income (MAGI) under 138% makes the household ineligible for PTC and places the family in Medi-Cal through Covered California.

Below are some of the topics Publication 974 covers

Minimum Essential Coverage

There are numerous government sponsored health plans that if a person is enrolled in or qualifies for, the individual is ineligible for the ACA premium tax credits. Pub. 974 lists the plans meet the minimum essential coverage (MEC) rules under the ACA along with the exceptions.

Employer Sponsored Group Plans

Within the list of health plans that meet minimum essential coverage are the conditions with which an employer-sponsored group plan is also considered MEC. The rule which may trip up some households is that group health plans are considered MEC as long as they are affordable for the employee and not necessarily the entire family. In other words, household members who are eligible to be on a group plan, as long as it is affordable for the employee only premium, are ineligible for PTCs.

Your family members also may be unable to get the PTC for coverage in a qualified health plan for months they were eligible to enroll in employer-sponsored coverage but only if it was affordable for the employee. If you or your family member enrolls in the employer cover-age, the individual enrolled cannot get the PTC for cover-age in a qualified health plan, even if the employer cover-age is not affordable or does not provide minimum value. –Pub. 974, page 5

How to determine if the plan is affordable. Your employer coverage is considered affordable for you and for a family member if your share of the annual premiums for self-only coverage is not more than 9.5% of your tax family’s household income for 2014. – Pub. 974, page 6

The IRS publication also discusses how to determine the affordability of group plans that are on a calendar year basis (Jan. – Dec.).

Domestic Abuse and Abandonment Relief

In order to be eligible for PTC married couples must file a joint federal tax return. This may be impossible under certain situations. Men and women who have suffered domestic abuse or abandonment, but are still legally married, can received premium tax credits as long certain records are kept.

Penalty Relief with excess APTC

Tax payers are subject to penalties if they don’t pay enough tax during the year either through paycheck withholding or quarterly tax payments. If a household has to pay back all or a substantial portion of the Advance Premium Tax Credits that could trigger the penalty. However, the IRS is providing relief from the underpayment penalty if it is triggered by the repayment of the excess APTC.

If you owe a penalty for failure to pay, the IRS will send you a notice demanding payment. To request relief from the penalty for failure to pay, you should respond to the notice demanding payment of the penalty with a letter that includes the statement: “I am eligible for the relief granted under Notice 2015-9 because I received excess advance payment of the premium tax credit.” The letter should be sent to the address listed in the notice demanding payment. Interest will accrue until the underlying liability is fully paid. – Pub. 974, page 8

Individuals not lawfully present

If a tax filer or a member of his or her household is not lawfully present or undocumented, they are not eligible for PTC and they are also exempt from having to purchase MEC health insurance.

If you or a member of your family is not lawfully present and is enrolled in a qualified health plan with family members who are lawfully present for one or more months of the year, you may take the PTC only for the coverage of the lawfully present family members. You must determine and repay all APTC paid for the coverage of a not lawfully present family member. – Pub. 974, page 9

Tax payers who have to extract the PTC for family members who are not lawfully present are instructed to use form 8962 Premium Tax Credit reconciliation. The calculations for determining how much APTC must be repaid when not lawfully present household members are comingled with lawfully present family members on the same health plan get complicated really fast. Publication 974 gives several examples and worksheets for this laborious task of how much APTC must be repaid.

Individuals filing tax return with no personal exemptions

Some individuals may file a federal tax return on income they earned even though they are claimed as a dependent on someone else’s tax return and they claim zero exemptions on their own tax return. You can’t be claimed as a dependent and also receive the PTC. Consequently, if an individual enrolled in a qualified Marketplace exchange health plan and received APTC, they will have to repay the advance premium tax credits.

If you file an income tax return but claim no personal ex-emptions, even for yourself, your tax family size is 0 and you cannot take the PTC. You must repay the APTC for which you are responsible. Complete lines on Form 8962 as explained below. Leave all other lines blank. – Pub. 974, page 15

Example 2. Mark enrolls himself and his child, Donna, in a qualified health plan with coverage effective for all of 2014. The Form 1095-A he received from the Marketplace shows that $6,000 of APTC was paid for their coverage ($500 is entered in Part III, column C, for each of lines 21–32). Mark files an income tax return for 2014 on Form 1040 and claims no personal exemptions. Mark’s parents, Steve and Sherry, claim a personal exemption for Mark. No one claims a personal exemption for Donna. Because Mark enrolled Donna in coverage and no one claims a personal exemption for Donna, Mark must reconcile the APTC paid for Donna’s coverage. Steve and Sherry must reconcile the APTC paid for Mark’s coverage. Because Steve and Sherry must reconcile the APTC paid for Mark’s coverage and Mark must reconcile the APTC paid for Donna’s coverage, Mark must complete Part 4 of Form 8962 to allocate shared policy amounts with Steve and Sherry. Mark, Sherry, and Steve do not agree on an allocation percentage. Mark completes Form 8962 as follows. – Pub. 974, page 15

Determining Second Lowest Cost Silver Plan premium

Even though either the federally facilitated Marketplace exchange or a state exchange is supposed to list the Second Lowest Cost Silver Plan (SLCSP) premium on the 1095-A, the IRS is acknowledging that, for various reasons, a tax payer may have to go search for the SLCSP. This may occur because the individual or family moved to a different rating region and didn’t notify the exchange or the SLCSP is left blank on the 1095-A because the household didn’t request financial assistance. While Publication 974 states that only the Marketplace exchange can provide the SLCSP, they seem to be indicating that they may accept SLCSP numbers not on a 1095-A but verifies from an exchange website.

If you enrolled through a state Marketplace, you may find information about whether your state has an SLCSP premium tool on that state’s website. If your state Marketplace does not have an SLCSP premium tool, you will need to contact the state Marketplace for the correct SLCSP premium. –Pub. 974, page 16

Partial year marriage calculation

A marriage or divorce during the year can lead to very complicated calculations for determining the correct PTC of the new households. The IRS provides several methods for calculating the PTC when marriage brings together new household members, income, and health plans during the tax year. The instructions take tax payers through a series of worksheets and the determination of the alternative family size.

Alternative family size. Your alternative family size is used to determine an alternative monthly contribution amount (see Monthly contribution amount under Terms You May Need to Know in the Instructions for Form 8962) on Worksheets I and III, which may reduce the amount of excess APTC for the pre-marriage months that you must repay. When determining your alternative family size, include yourself and any individual in the tax family who qualifies as your dependent for the year under the rules explained in the instructions for Form 1040 or 1040A, line 6c, or Form 1040NR, line 7c. Do not include any individual who does not qualify as your dependent under those rules or who is included in your spouse’s alternative family size. –Pub. 974, page 17

Most of the online or software based tax preparation programs have all the different steps and worksheets built into them for determining the partial year marriage PTC reconciliation. But there may still be situations that necessitate following the IRS worksheets to determine the final PTC.

Self-employed health insurance deduction

Under certain conditions, self-employed individuals can claim their health insurance premiums as a deduction on their federal taxes. This deduction reduces the tax payer’s Adjusted Gross Income (AGI). The tax payer’s AGI is fundamental for determining a household’s Modified Adjusted Gross Income for the purposes of calculating the amount of the Premium Tax Credit the tax payer may be entitled to. The health insurance premium deduction creates a circular reference problem with figuring the both the AGI and PTC.

Circular reference calculation

Federal 1040 tax forms contain a circular reference for self-employed individuals trying to calculate their premium tax credit.

For those familiar with Excel spreadsheets you’ll remember circular reference warning. “Circular references are any references within a formula that depend upon the results of that same formula. For example, a cell that refers to its own value or a cell that refers to another cell which depends on the original cell’s value both contains circular references.”

Serious number crunching

The circular reference issue is better explained by website thefinancebuff and its post Circular Reference In Self-Employed Health Insurance Deduction Under Obamacare Premium Subsidy. Publication 974 gives two methods for solving for the correct PTC for self-employed households. Neither of the methods are particularly user friendly unless you are a tax expert.

Tax software to the rescue?

Instructions for the 2014 form 1040 tax return state that tax payers who can qualify to deduct health insurance premiums from their taxes because they are self-employed and purchased a qualified health plan through a Marketplace exchange must use the worksheets in Publication 974 to determine that actual deduction. Supposedly, the online tax preparation software have the either the suggested IRS iterative or simplified calculation method built into the software.

“Can you take the PTC?” IRS flow chart from Publication 974 for the premium tax credits.