For many individuals and families, their health insurance premiums will be lower through Covered California than a small group health plan. The higher subsidies offered by the American Rescue Plan, combined with the family glitch, means that many low and moderate income employees are paying more for their health insurance if they are in a small group employer plan. I compare some of the health insurance rates through Covered California and small group plans to illustrate the problem.

For several years, small group health insurance premiums were lower than the rates offered through Covered California to individuals and families. The lower rates combined with the employer contribution made the small group rates very competitive to Covered California. In recent years, the individual and family rate increases have slowed – and in some cases health plans rates have been reduced – closing the gap between the individual and family plans and small group plans for equivalent metal tier plans.

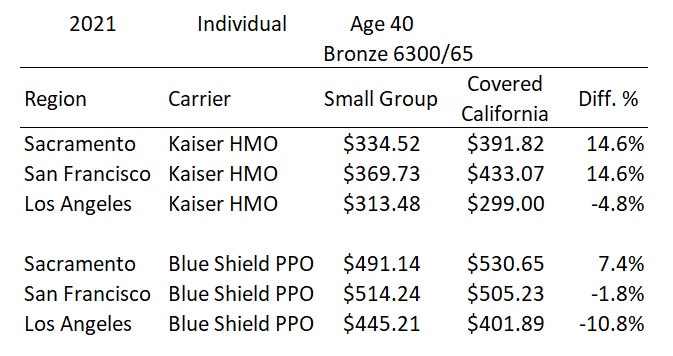

A quick comparison of the Bronze 60 ($6,300 deductible, $65 office visit copayment) offered by Kaiser and Blue Shield shows that depending on the region, the Covered California rates are actually lower than the small group plans. These are the full rates with no employer contribution or federal ACA subsidy to lower the monthly premium. The real test is a comparison of the net monthly rates after an employer contribution or Covered California subsidy is applied to the full health insurance premium.

Covered California Is Better Than Small Group Plans For Employees

The following rate comparisons are based on the following conditions

- Household family of three: two adults each age 40, one child age 10.

- Small Group rates were pulled from the respective region of Blue Shield and Kaiser small group rates dated January 1, 2021.

- Covered California rates and subsidy derived for the household based on a zip code within the specific county and using the latest household median income from the U. S. Census Bureau.

- Health plan comparison is the Silver 70 from Covered California and the comparable small group Silver plans. Note, the Covered California Silver 70 plans are artificially inflated 10 to 15 percent over the same plan off-exchange.

- Employer Contribution is the minimum 50 percent of the employee only rate. Zero contribution towards spouse and dependents.

- Assumption: only one adult has access to employer sponsored the health insurance.

- Family Glitch: if the spouse and/or dependents are offered affordable small group coverage, those individuals are ineligible for Covered California subsidies.

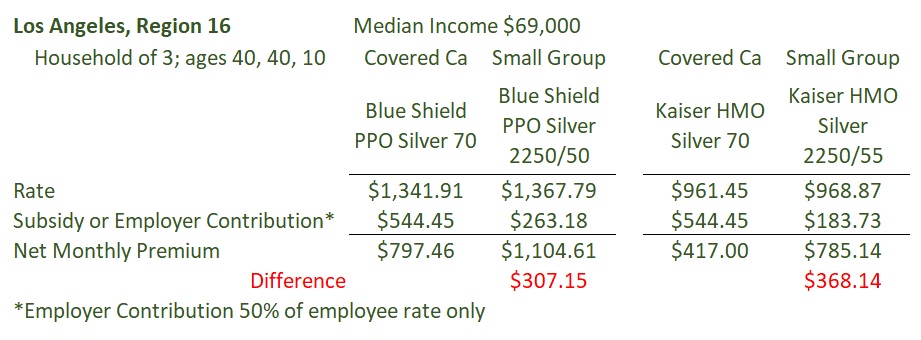

In Los Angeles, the median income is $69,000. The family of three pays $307.15 more for a Blue Shield PPO small group plan and $368.14 more for a comparable Kaiser small group plan, when compared to the subsidies offered through Covered California in Los Angeles.

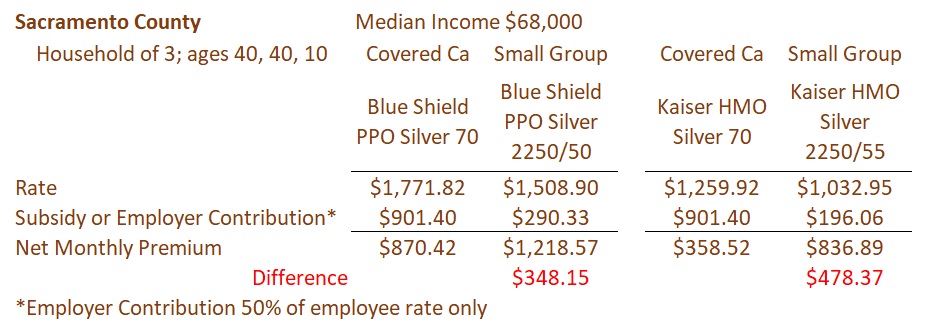

For Sacramento County, the median household income is $68,000. The theoretical family of three would pay $348.15 more for a Blue Shield small group Silver plan and $478.37 for the Kaiser Silver.

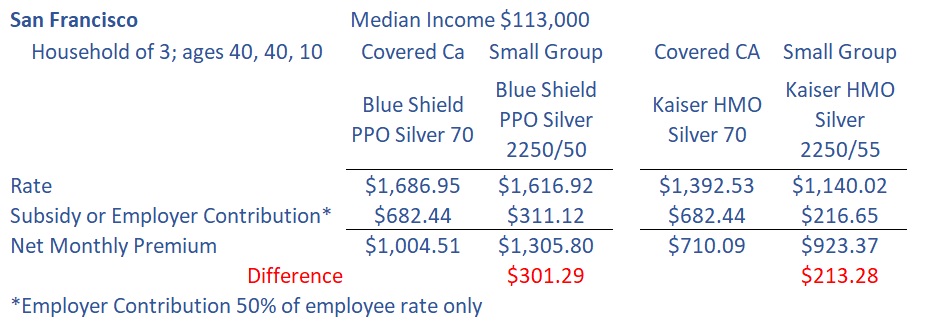

San Francisco has the highest median income of the regions compared at $113,000. The higher income lowers the subsidy in Covered California. However, the family would still pay $301.29 more for the Blue Shield small group Silver plan and $213.28 extra for the Kaiser Silver plan.

Small Group Lower Net Costs

The net monthly small group health insurance cost for the family could be lower if both adults have access to small group insurance. If the second adult chose the same Silver plan and the same employer contribution was made, the family would only have to pay the full rate for their child. However, only in the San Francisco scenario would an additional employer contribution reduce the net health insurance premium below the subsidize Covered California rate.

While it is not readily apparent from the comparisons, small group plans are generally better for higher income households. As the income increases, the Covered California subsidy decreases. The employer contribution for a small group plan is not dependent on income, but is tied to the age rate. The set employer contribution works in the favor of higher income households.

Worst Case Small Group

There is one pernicious small group feature that can make the net health insurance even worse than the those calculated. In some small group arrangements, the employer can set the benchmark contribution to a Bronze plan for the employee. Instead of 50 percent of the selected the Silver plan, the employer will only make a contribution of 50 percent of the lower cost Bronze plan. The smaller employer contribution if the family selects a Silver plan increases the final net cost for the family.

Covered California Flexibility

Small group plans dictate that all family members must be enrolled in the same plan as the employee. This is not the case with Covered California. One adult can select a Blue Shield PPO Silver, the other adult could enroll in a Molina Bronze plan, and they could enroll their child in a Kaiser Gold plan. The total subsidy would be the same, but the different rates could lower the overall family health insurance costs.

Based on the real-world comparisons I’ve done for individuals and families in small group plans, most would benefit from enrolling in Covered California. Anecdotally, I’ve talked to several employers who either have or are considering terminating their group coverage. Many small employers, who earn too much income to qualify for a large subsidy from Covered California, keep the small group plan to lower their health insurance costs. This is no problem if most of the employees are similar high wage earners. For the production employees, those making a moderate salary or hourly wage, Covered California provides a lower monthly health insurance cost.

As it stands today, Covered California is putting a brake on small group plans because the individual and family subsidies are so much better than what the employer can contribute to make health insurance affordable.