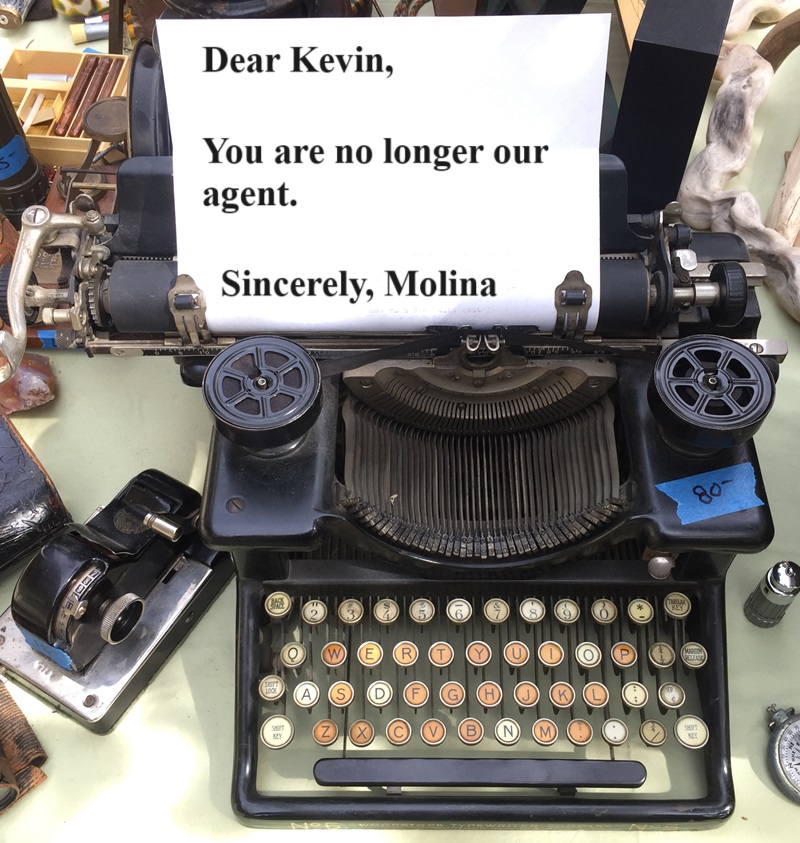

The letter was ominous, if not a little vague and light on details. Molina Healthcare had informed me that they had revoked my authority to solicit Molina Marketplace health plans. I was dumped as an appointed agent for Molina to enroll individuals and families into Covered California health plans.

There Was No Reason Why Molina Dumped Me

There was no specific cause for the Molina action against me. The letter stated, “Molina has the right to terminate an appointment or revoke a Participating Producer’s authority to Solicit the Molina Marketplace products at any time.” Gosh, what had I ever done to Molina other than represent their products fairly when presenting their Covered California health plans to consumers?

My only guess is to why Molina decided to cull me as an agent from their stable of producers is that I only had one enrollment in San Diego. If you are a big producer for an insurance company, they usually do not touch you. However, whipping a horse when it is down does not make it get up and run any faster.

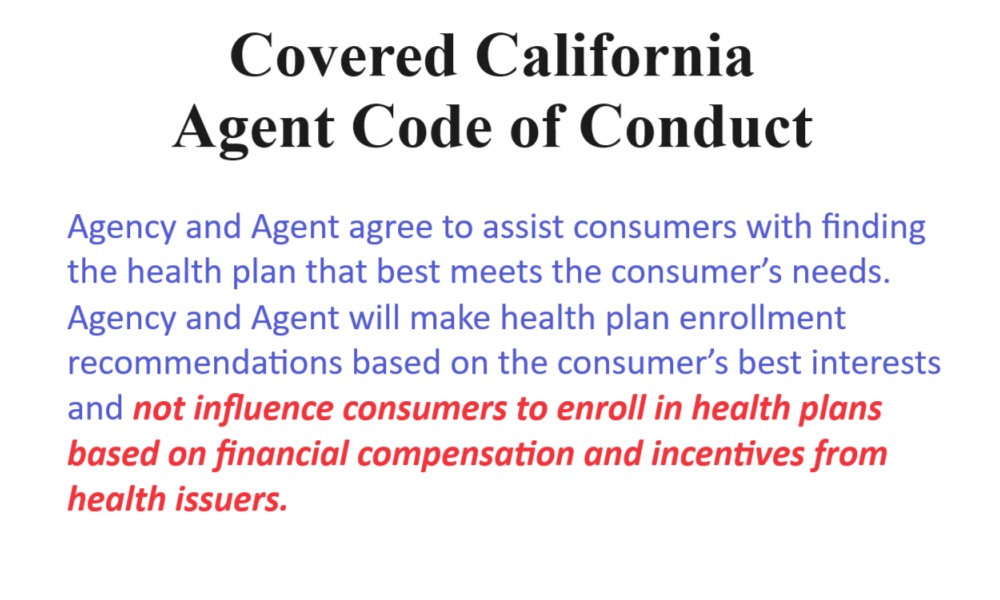

Covered California Agent Code of Conduct

My termination as a Molina appointed agent is in direct conflict with the 2020 Covered California Agent Code of Conduct. Under the rules of the Code of Conduct, the first rule is, “Agency and Agent agree to fairly and accurately promote Covered California health plans to consumers.” The Molina letter I received states,

Accordingly, this Notice is to inform you that you will no longer be authorized to Solicit enrollment in the Molina Marketplace products effective as of October 26, 2023.

If I somehow hide from a consumer that a Molina plan is being offered to them, I break the Covered California Agent Code of Conduct. If I present the Molina health plan as an option to the consumer, I may be subject to some sort of legal action by Molina for representing their plans.

No Steering Consumers Based on Healthplan Compensation

Another rule of the Agent Code of Conduct is that Certified Agents agree to, “…. make enrollment recommendations based on the consumer’s best interests and not influence consumers to enroll in health plans based on financial compensation and incentives from the health issuers.”

Admittedly, the commissions or the per member per month compensation offered by Molina and the other health plans is nothing to get excited about. However, it is nice to be compensated for the work of spending time with a consumer, assessing their health care needs, finding their providers, filling out the Covered California application, and enrolling the consumer into a health plan.

For some agents, the lack of any compensation is the impetus to avoid speaking about the plan. The bias, caused by no compensation, is like a health plan offering a bonus for enrolling a large number of individuals. Either way, some agents are influenced to steer consumers into plans they receive compensation for or meet some quota to receive a bonus.

What incentive do I have to enroll and maintain the Covered California account for an individual or family that wants to select Molina as their health plan? The incentive is if Covered California finds out I am steering people away from Molina they could revoke my certification to enroll consumers into their health plans. Of course, Molina is telling me not to talk about their health plans. I am lost about what I’m supposed to do.

For an agent, the service does not stop with the enrollment. There are other questions and actions that need to be taken after the enrollment. My one Molina client is typical of many Covered California consumers. We made sure the citizenship verification request from Covered California was properly uploaded. There is also the annual income attestation verification that usually needs to be filled out and uploaded to his account. Of course, there are the little changes to income and reviewing if the Molina plan is meeting his health care needs.

I have nothing against Molina. I have had several consumers enrolled into their health plans. They seem to have a good network of providers in the regions they offer health plans. Their plans are competitively priced. My one Molina client feels their customer service is good and he is happy with the health plan.

Until Molina dumped me, I was proud that I was appointed with every health plan offering insurance through Covered California. Regardless of where the individual lived in California, I could represent all the health plans with no bias based on compensation. Actually, I am too lazy to worry about if a health plan pays me a 1 percent commission or $17 per month for an enrollment. Every week I usually help either an individual or family apply through Covered California to be determined eligible for Medi-Cal. Agents receive no compensation for assisting with the first step of Medi-Cal enrollment.

My first consideration as a Certified Insurance Agent is to Covered California. I believe in their mission. Covered California is doing a good job of offering a variety of health plans to consumers with financial assistance to lower the monthly premiums. If a consumer feels a Molina plan is best them, I will assist in effectuating their enrollment into the Molina health plan.

2024 Molina Agent Commission Update

I still have not learned why Molina dropped me. In March 2024, I contracted with Dickerson Insurance Services to be my General Agent for Molina. Apparently, Moline only uses General Agents when it comes to working with agents. In April of 2024 I was reappointed with Molina.

In June, not seeing any commissions from my Molina enrollments, I contacted Dickerson to learn why. I had to provide Dickerson a list of my three Covered California Molina health plan enrollments. Molina told Dickerson that since those enrollments happened when I was not appointed with Molina, they would not pay me a commission.

I complained to Covered California that Molina was denying me commissions as the delegated agent for those enrollments. Covered California said that they have no control over how the health plans structure their agent rules.

As I replied to Covered California, a health plan can develop a scheme to deny commissions to agents, but I, as certified Covered California agent, must represent all of the health plans fairly. That makes no sense at all. Covered California is still making their 3.25% commission from Molina for the enrollments. I am cut out of the structure for at least those three clients. Thank you, Covered California, for sticking up for agents who perform close to 50% of the enrollments.

While I will not dissuade any client from selecting Molina, I won’t be able to endorse Molina either.