Enhanced California Majority Report photo, Dave Jones Insurance Commissioner. www.camajorityreport.com

The health insurance rate regulating Proposition 45 on the November ballot is relatively simple in that it attempts to curb excessive premium increases by health insurance companies by allowing the Insurance Commission to deny any rate he or she deems as being unreasonable high. California, on the other hand, has developed a complex review process for rate proposals, yet no elected official or department has authority to stop the implementation of an excessive premium increase. While the implementation of Prop. 45 won’t be as bad or as smooth as the campaigns suggest, giving the insurance commission a big hammer to deny runaway premium increases outweighs the fears that its implementation will be a disaster.

Prop. 45 won’t be disastrous

Rarely do propositions have either the disastrous consequences put forth by the opponents or the world transforming benefits espoused by the authors of the initiative. They all seem to cost more money than expected and cause the enforcing departments to hire more people. Prop.13 limited property taxes and the three-strikes Prop. 184 put more habitual offenders in jail. But most people would agree that we still seemed to be taxed just as much as before and we don’t feel any safer even with more bad guys in prison.

No proposition is perfect

I suspect Prop. 45 will achieve the same mixed results as past propositions 13 and 184 that had laudable and noble goals. As a California citizen my whole life I no longer expect any politician, law, or voter approved initiative to ever fulfill the campaign promises or hype. For better or worse, we usually do get the kernel of inspiration of most propositions. For proposition 45, the light of reality will be the new executive power to deny excessive health insurance premiums.

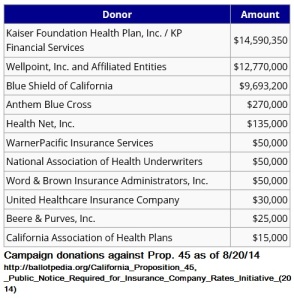

How much of the increase goes to campaign contributions

Biggest donations to defeat Proposition 45 are all connected to the health insurance industry.

From a purely psychological and strategic perspective, the mere realization that the Insurance Commissioner can deny a proposed rate increase by a health insurance company or health plan is significant. It’s not that health insurance companies won’t still push the envelope of unacceptable rate increases, but they may dial back the percent increase. The bulk of any health insurance premium and rate increase is built upon sound actuarial data. Unfortunately, it is difficult to parse the necessary rate increase to cover forecasted trend increases in health care services from that of the company’s desire to pad the bank account for CEO salaries, bonuses and political campaign contributions.

Prescription drug costs rapidly increasing

A glance at the 2015 rate proposals for individual and family plans shows that most of the carrier’s healthy increases are driven by increasing costs of prescription drugs and hospital expenses. (See: Covered California 2015 rate comparison by region). But even these trend increases don’t account for some of the double digit rate increases that Covered California is allowing to take effect in 2015. Since the rate and benefit negotiations between Covered California and the carriers are secret, we don’t know if the new rates were modified during the bargaining process or the carriers just convinced Covered California they weren’t that bad.

We do know that…

- Health Net is eliminating their PPO plans for Exclusive Provider Organization (EPO) plans with no out-of-network coverage And increasing those premiums 5% to 9%.

- Anthem Blue Cross is increasing the EPO plans in several regions from 11% to 14% and their region 3 HMO plan is jumping 15% to 19%.

- L.A. Care is bumping up their Bronze HMO plans 12%

- Kaiser is back peddling on rates with an 8% decrease on many plans in several regions. Kaiser’s actuarial review by Milliman states the decrease is not actuarially sound in the aggregate.

Is 19% a reasonable rate increase?

When is a 19% rate increase considered reasonable? Did Kaiser overcharge for health premiums in 2014? How can a health insurance company cut benefits by switching to an EPO, further reduce their providers and be granted a 9% increase? (See: Covered California plans likely to continue offering narrow networks and Health Net drops PPO Plans from California ).

Covered California is a business

Covered California, while neither the Board nor staff can take a public stand, has come out against Prop. 45 with an internal analysis of the disruption the proposition will have on their operations. Of course, most of their analysis is speculation based in part on the less than cuddly relationship between Covered California and the Insurance Commissioner’s office. If the high paid executives can roll out a cranky but usable website for the ACA tax credits, they can certainly work with the Insurance Commission so Prop. 45 has minimal impact on their operations. But let’s not forget that the DOT COM at the end of the Covered California website means they are a business. In 2015 Covered California has to be self-supporting as the federal grant money dries up. Download Covered California analysis of Prop. 45 at end of post.

Businesses care about revenue

As a business, Covered California is more concerned about their own existence than the interests of the consumer in many situations. How else could they let Health Net switch to an EPO and get a rate increase? How can they let Anthem Blue Cross and other carriers get away with double digit premium increases without explaining it to the public?

Tax credits white wash premium increases

Covered California makes their money from a fee charged on each health plan sold. The ACA subsidy helps hide the burden of this fee and excessive rate increases from the consumer that is eligible for the Advance Premium Tax Credits. Covered California has very little motivation to curb excessive rate increases because they know it is muted for over 90% of consumers who purchase plans through the exchange. In short, Covered California can’t be held up as an “independent commission” regulating rates because they have a horse in the race along with the health insurance companies.

Insurance Commissioner should have a STOP sign

It’s hard to speculate if the Insurance Commissioner would have had any more impact on negotiating reasonable rate increases beyond what Covered California and the Department of Managed Health Care negotiated and reviewed. What is undeniable is that the health insurance companies are ten steps ahead of any regulating law or agency oversight. However, there is no getting around a stop sign that might be thrown up by the Insurance Commissioner. It’s probably time we had one real cop that can that can lift a stop sign high in the air for the public to see and deny excessive rate increases. It’s time for Prop. 45.

See also: Agents unite to bash Prop. 45

[wpfilebase tag=file id=159 /]