The 1095A you receive from your health insurance marketplace such as Healthcare.gov or Covered California can look baffling. The dollar amount numbers reported to you have a specific purpose when you file your federal tax return. If you find errors, you should promptly contact the marketplace exchange and request a correction.

1095A Dollar Amounts Explained

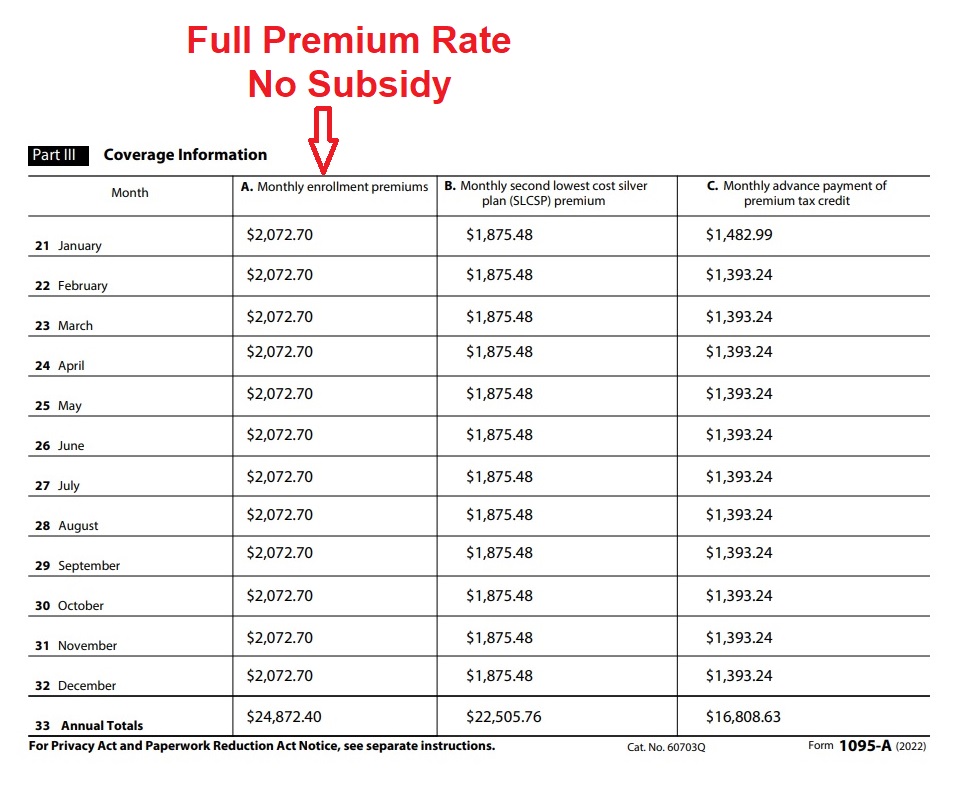

Column A. Monthly enrollment premiums is the full premium rate for the health insurance that the family members were enrolled in for the month. The important role this dollar amount plays is limiting your health insurance Premium Tax Credit subsidy. You can only receive a subsidy equal to the cost of the health insurance. If you are eligible for a subsidy of $2,500 per month, but enroll in a health plan that only costs $2,000 per month, your subsidy will be limited to $2,000.

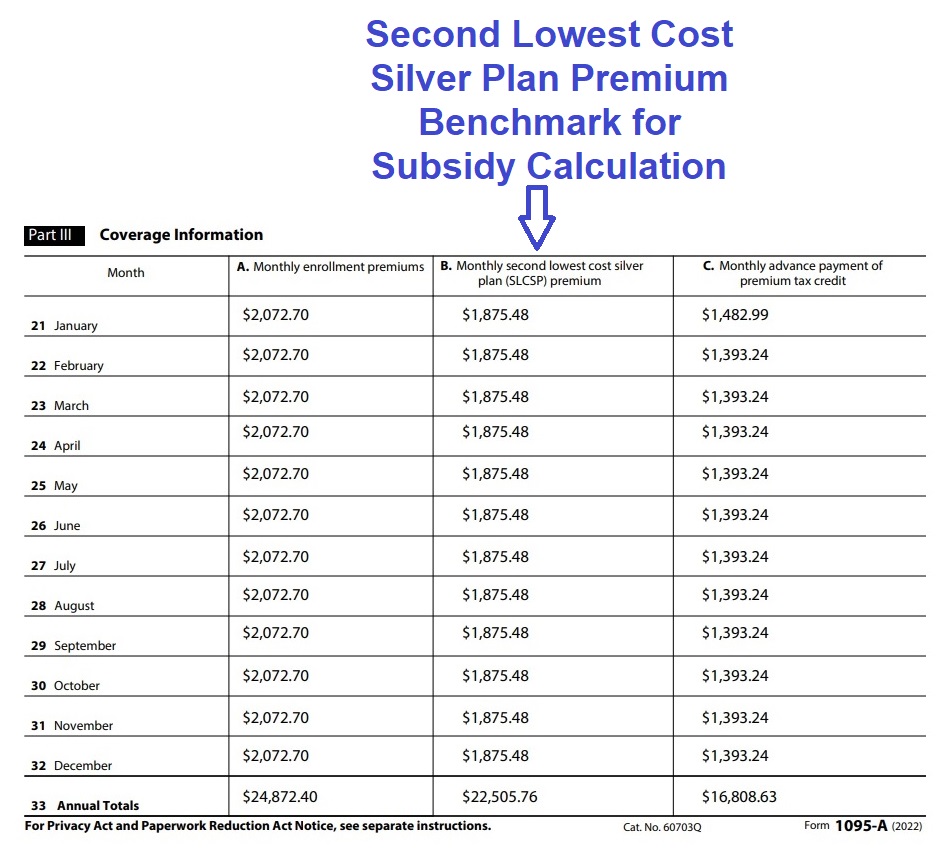

Column B. Monthly second lowest cost silver plan (SLCSP) premium is a very important dollar amount. The subsidy calculation is based on making the SLCSP a certain percentage of your household income. Perhaps your consumer responsibility percentage is 4 percent of your household income. The subsidy will be calculated to lower the SLCSP down to 4 percent of your estimate household income. The IRS uses the SLCSP to determine your final Premium Tax Credit based on your final Modified Adjusted Gross Income.

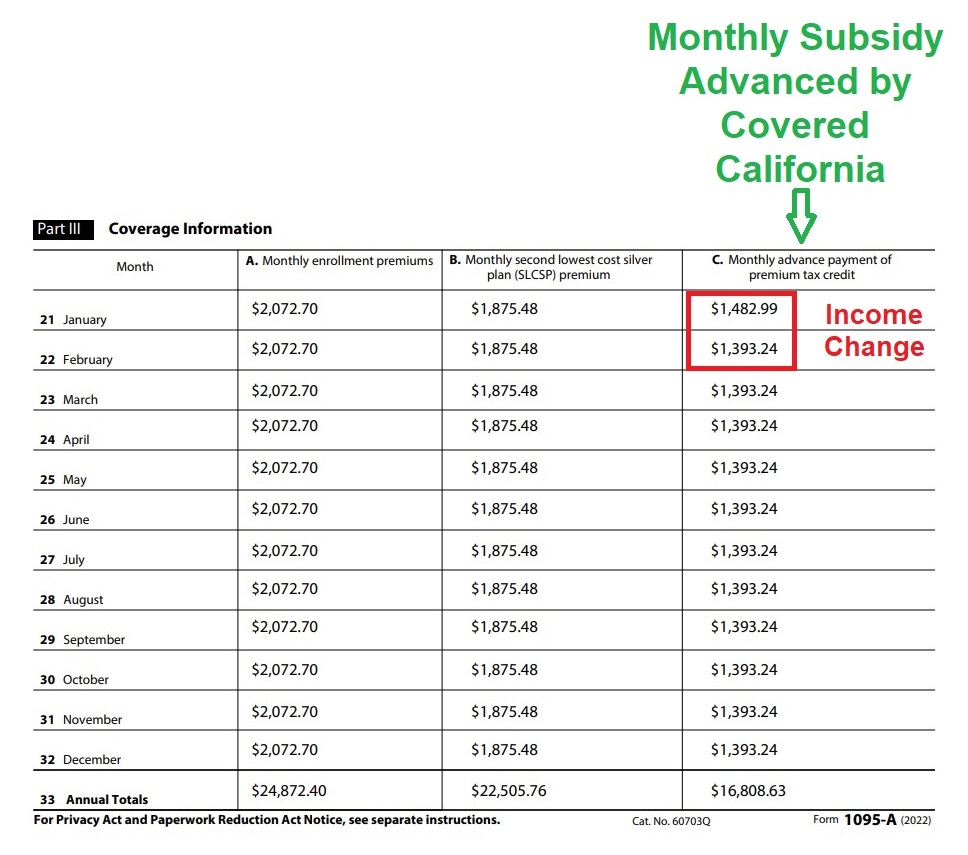

Column C. Monthly advance payment of premium tax credit is the dollar amount forwarded to your selected health plan every month by the exchange to lower your health insurance premium. The total dollar amount of column C will be compared to the Premium Tax Credit you are eligible for when you do your 2022 federal tax return. If your income is lower than the original estimate, you will get more Premium Tax Credit. If your income is higher than estimated, you will have to repay some, or all, of the Advance Premium Tax Credit (APTC) shown on the 1095A form.

Notice that in this example the APTC subsidy decreased from January to February. That is because the family increased their 2022 income estimate, which in turn, lowered the monthly subsidy they were eligible for.

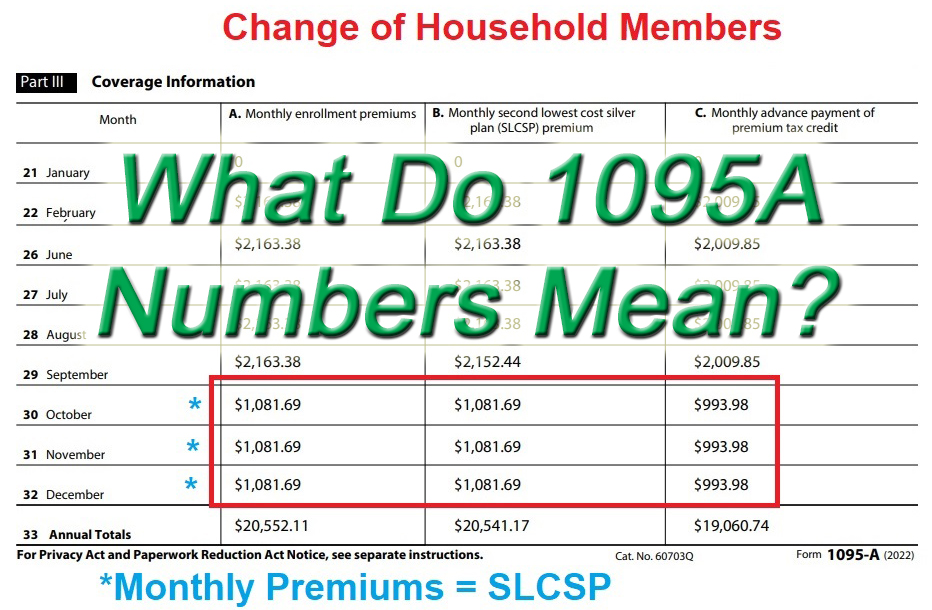

Change For Household Members

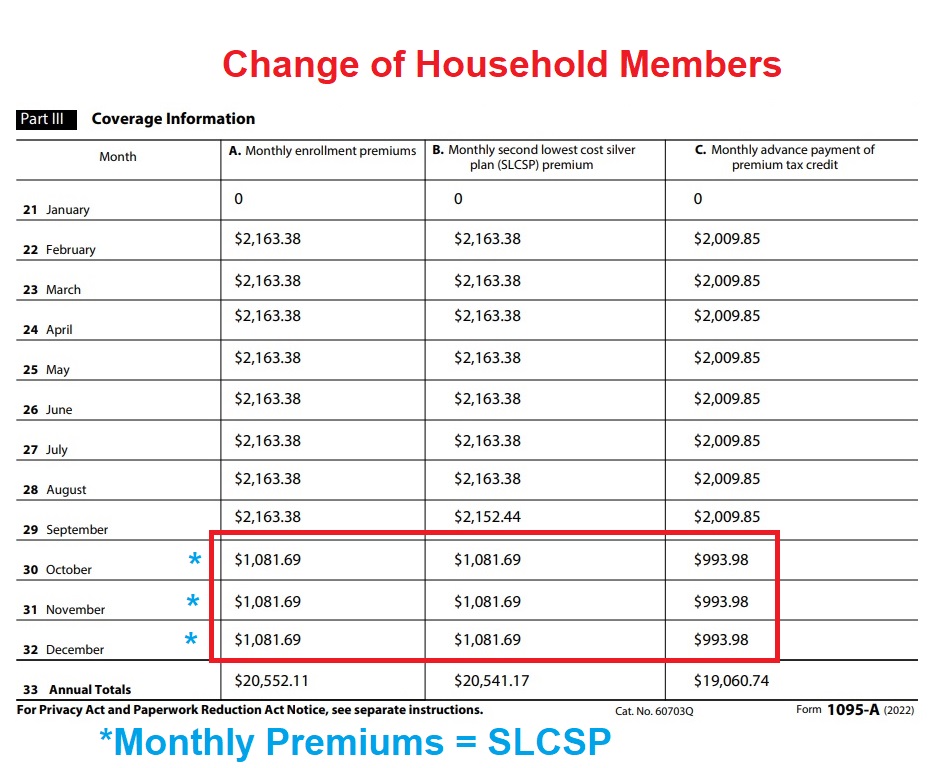

If changes to a household member’s enrollment or residence occurs during the year, two or more 1095As will be generated. In this example, one of the household members moved to another county. The first 1095A reflects the dollar amounts for those months through September for the whole family. The dollar amounts in the columns for October through December are for the remaining household member.

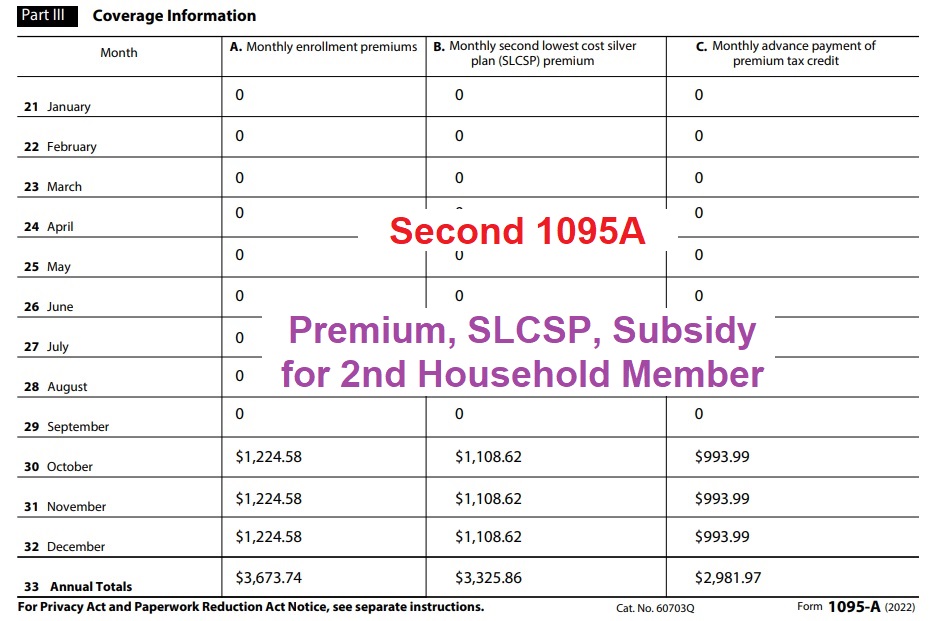

The second 1095A shows those dollar amounts for the second household member residing in a different county. Because the SLCSP can change by region, the second 1095A reflects a different dollar amount for the SLCSP for those last three months. Regardless, all of the total dollar amounts from the two 1095As will be added together on IRS form 8962 for the purposes of reconciling the final Premium Tax Credit for the primary tax filer.

Covered California 1095A Form Overview

The Affordable Care Act (ACA) requires IRS Forms 1095-A (issued by Covered California), B (issued by government agencies, such as Medi-Cal and Medicare, the insurance companies outside Covered California, and certain employers), and C (issued by large employers) be provided to consumers and a copy to the IRS.

A Covered California notice will be included with a consumer’s IRS Form 1095-A as well as instructions. This form will help consumers determine whether the amount of Federal Advanced Premium Tax Credits (APTC) paid to Covered California Qualified Health Plans on their behalf in the 2022 benefit year was more or less than the amount they were eligible to receive based on their tax return data, such as income, family size, and tax filing status.

FTB 3895 tax forms will not be provided for the 2022 benefit year because consumers did not receive the California Premium Assistance Subsidy. The FTB 3895 tax form is available for 2020 and 2021.

According to the IRS and Franchise Tax Board, consumers who are determined APTC/State Subsidy eligible and then later determined Medi-Cal eligible and have overlapping coverage for a month or two during the transfer process, do not generally have to repay the APTC/State Subsidy received during the overlapping months. However, if a consumer is currently enrolled in both Modified Adjusted Gross Income (MAGI) Medi-Cal and a Covered California health plan with APTC/State Subsidy, they must contact Covered California immediately.

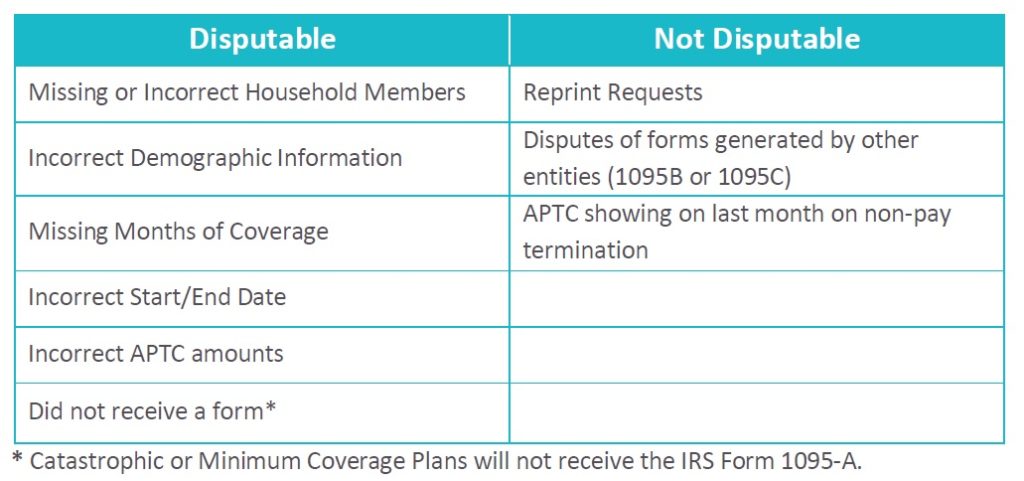

For more information and to access the 1095-A Dispute Form, visit the “Errors on your forms?” page of Covered California’s website. Please reference the chart below for examples of what is/is not disputable. Note: You may assist consumers with filling out the Covered California 1095-A Dispute Form, which is not an IRS Form.