Covered California manages two different health insurance plan subsidies for individuals and families. The first premium tax credit subsidy is from the federal government under the Affordable Care Act. The second is from the state of California. Some people will receive both subsidies adding more stress when it comes time to file income tax returns.

Higher Income Eligibility for California Subsidy

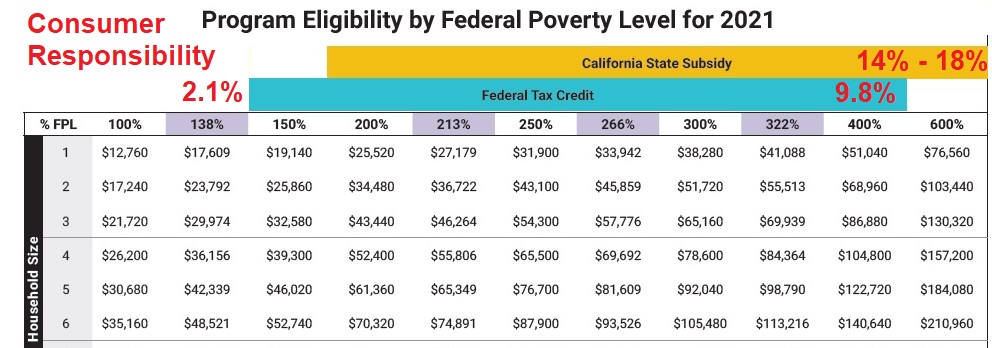

The Covered California income table was expanded to show that income up to 600 percent of the federal poverty level could be eligible for a subsidy. While most people seeking relief from high health insurance rates in California don’t really care who pays the subsidy, it may become an issue when it is time to file income taxes. Consumers need to be aware that they may be receiving subsidies from two different sources and each will need to be separately accounted for at tax time.

In 2020, Covered California started issuing premium tax credit subsidies to consumers from the state of California. This new subsidy is sometimes in addition to the federal subsidy. There are consumers who receive both the federal and state subsidy. The new California Premium subsidy is targeted at upper income households who earn more than 400 percent of the federal poverty level (FPL). The federal subsidy stops at 400 percent of the FPL.

The federal ACA subsidy is more generous limiting the household health insurance responsibility for health insurance premiums to 9.8 percent of household income. While the California Premium Subsidy may add a few dollars of subsidy below 400 percent of the FPL, it is really focused at upper income households. The California subsidy limits the household responsibility to between 14 and 18 percent of the household income.

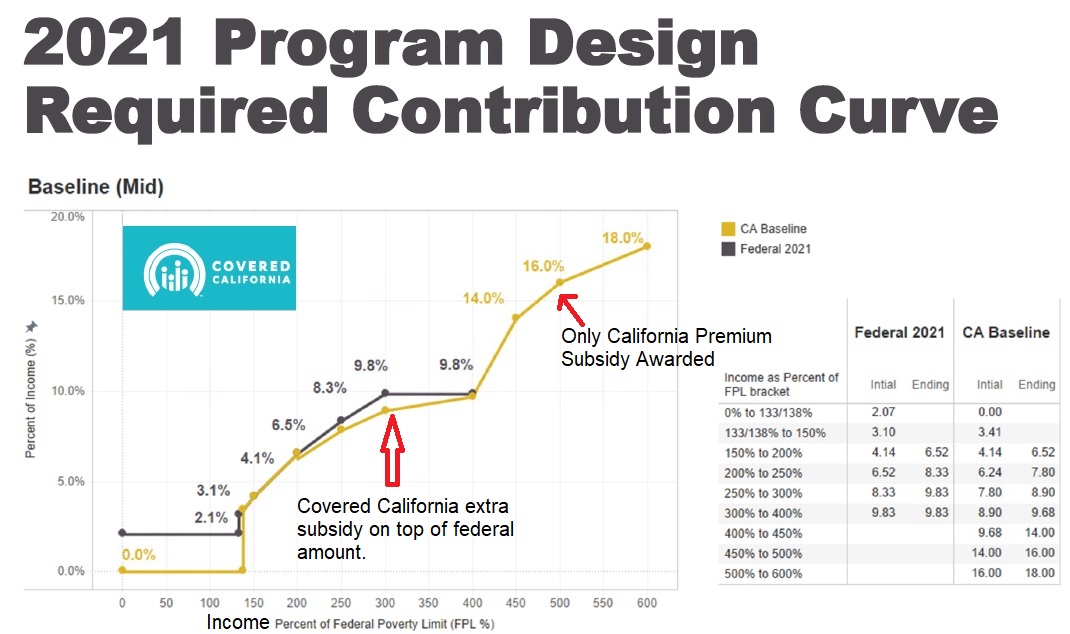

Both the federal and state subsidies use the second lowest cost Silver plan as the benchmark for determining the subsidy amount. Just because your income is in the zone for the California subsidies, it does not mean you will qualify for it. If the full cost of the health insurance plan is less than 18 percent of your household income, you may not be awarded any California Premium Subsidy. The federal ACA subsidy is reconciled on the IRS income tax returns, while the California Premium Subsidy is reported to the Franchise Tax Board.

Anecdotally, I have seen this happen often in Southern California where the health insurance rates are 30 percent less than Northern California and the household receives no California subsidy. On the flip side, I have many clients in Northern California who are getting a very generous California Premium Subsidy. This usually happens with individuals who are over 50 years old because the rates for older individuals are two to three times higher than younger adults and children.

Income Tax Reconciliation Federal and/or California

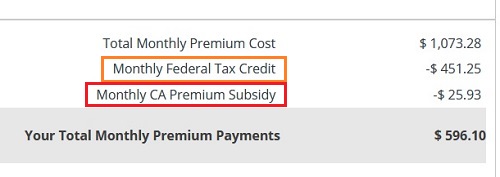

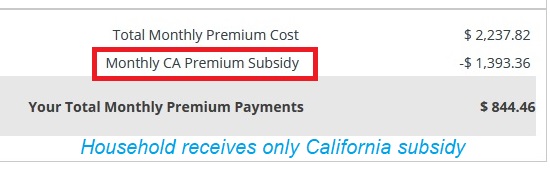

The second part of the subsidy puzzle that Covered California doesn’t really talk about is the reconciliation of the tax credit subsidies on income tax returns. If you receive both a federal and state subsidy, you will need to reconcile the amount you received with the subsidy you are entitled to based on the final Modified Adjusted Gross Income. If you only receive the California Premium Subsidy, you only have to deal with your California income tax return.

However, if your income deviates substantially from the estimate, either putting you in the federal ACA income zone or bumping you into the California income range (401% – 600% FPL), then the reconciliation will be more complicated. It’s possible to lose the more generous federal subsidy and receive no California subsidy, even though the income table indicates you are eligible for the California subsidy.

What does all this mean? Just because someone tells you that your income makes you eligible for health insurance subsidy, you still may not qualify for it. Additionally, there is no coordination of subsidy repayment between the feds and California. You may have to repay the subsidy to one government, while receiving a credit from the other government agency. If the final subsidy, regardless of who it came from equals thousands of dollars, it is probably worth the tax preparation hassle.