There are two reasons why Affordable Care Act (ACA) health insurance is so expensive. The first reason is the comprehensive list of coverage benefits included in the health plans. The second reason is the cost of the health care services and prescription drugs the insurance company must pay on the plan members behalf.

This is not a defense nor an attack of the current health insurance system. It is merely my observations of the current health insurance market after being an insurance agent for 15 years.

Two Reason Why Health Insurance Is Expensive

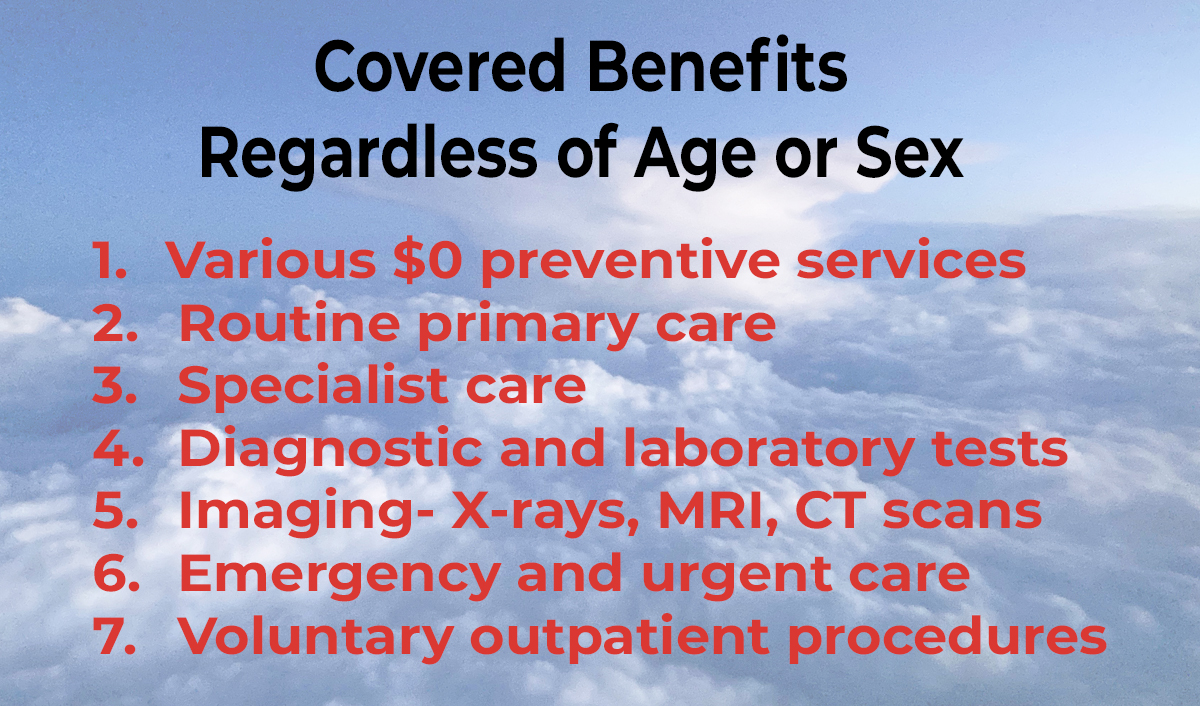

One reason why Affordable Care Act health insurance is expensive is because there are few gaps in coverage. The health plans include a laundry list of covered benefits regardless of your sex or age. In other words, virtually any health care system a person might experience will have some coverage benefits.

Covered Benefits

Preventive services such as immunizations, mammograms, annual physicals and colonoscopies for individuals over. With many of the services at no cost to the plan member.

- Routine primary care and specialist office visits

- Diagnostic and laboratory tests

- Imaging: X-rays, MRI, CT scans

- Emergency and urgent care services

- In and outpatient surgeries

- Maternity

- Mental health services

- Substance abuse treatment

- Cancer treatment

- Occupational and rehabilitative therapy

- Durable medical equipment

- Prescription medications

Before the ACA, there were health plans that may have excluded services such maternity, mental health, or coverage for prescription medications. Plus, most plans included exclusions or waiting periods for pre-existing conditions.

If you remove any of the covered benefits, you will reduce the cost of health insurance. If you apply exclusions and waiting periods for pre-existing conditions, you will reduce the cost of health insurance. When you reduce the prospect of potential claims the health insurance company must cover, the monthly health insurance premiums will be lowered.

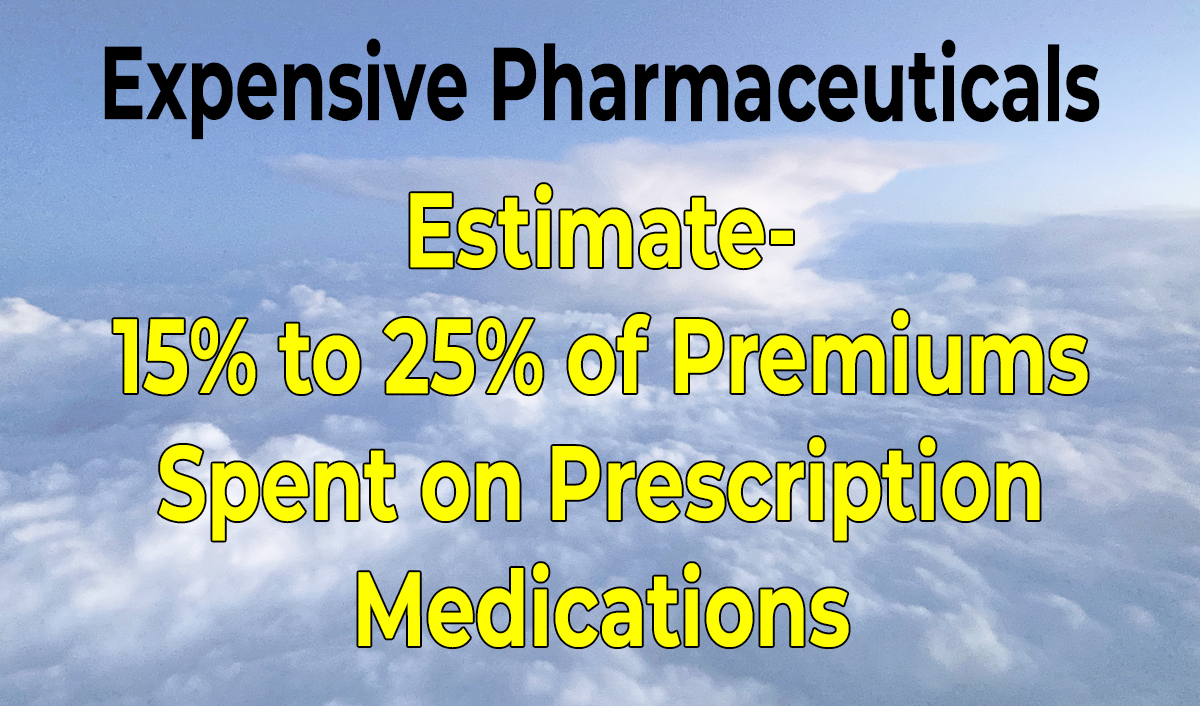

Pharmaceuticals

A big driver of increased health insurance premiums is coverage for prescription medications. Some estimates are that 15 to 25 percent of premiums are spent on covered drugs for the health plans. Before the ACA, there were many plans that did not include prescription drug coverage. Covering a comprehensive list of drugs for a variety of health conditions has increased the average health insurance premium.

Health plans must contract with pharmacy benefit managers to make covered prescription medications available to plan members. Drugs are expensive and one of the largest drivers of increase health insurance rates. While some people may rarely receive a health care service, they could have very expensive medications that run thousands of dollars a month.

The health plans, depending on the metal tier of the plan, can cover the majority of the prescription drug costs. Many of the health plans are activity working to reduce the cost of drugs available to plan members either through price negotiations or alternate delivery systems.

The Cost of Delivering Health Care Services

Aside from the covered benefits of ACA health plans offered in California, the premiums reflect cost of delivering health care services. In other words, the premiums reflect the cost of paying claims to a variety of providers from therapists to hospitals.

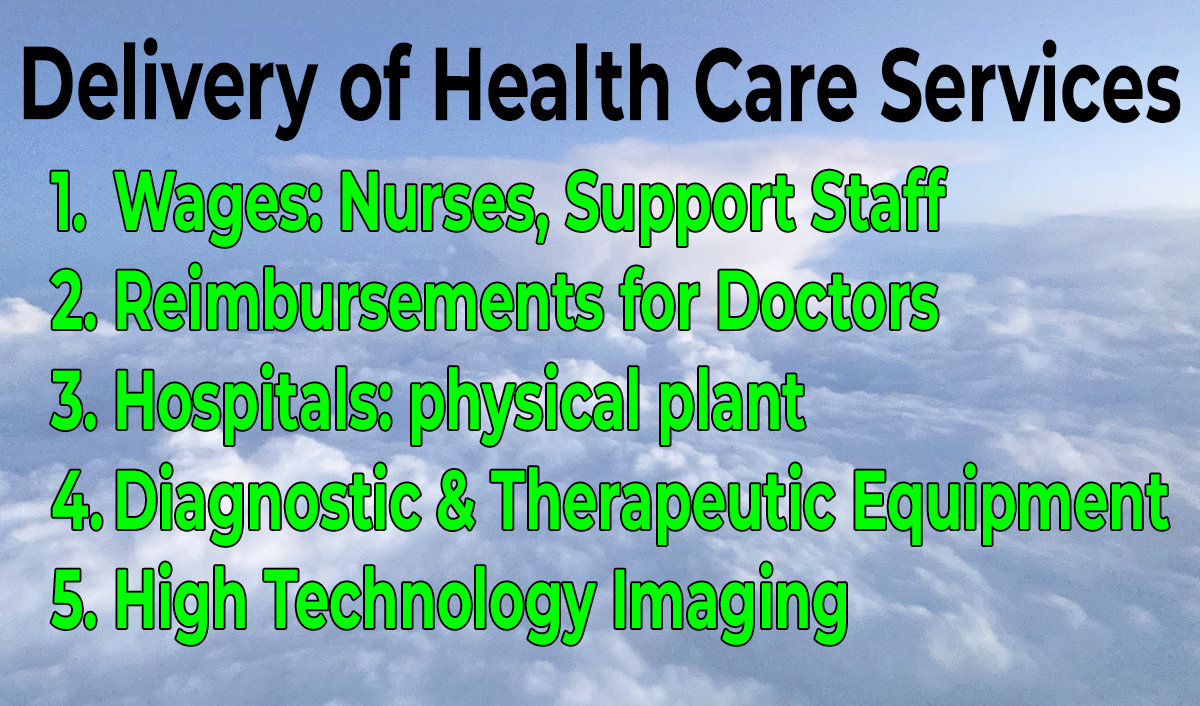

Some of the expenses included in reimbursement rates the health plans pay to providers are:

- Wages: nurses, administrators, support staff

- Reimbursements for doctors

- Hospital/facility: physical plant, debt service

- Diagnostic and therapeutic equipment

- High technology imaging machines

Health insurance premiums could be reduced if the doctors and nurses were paid less. I will not be the person to ask any of those highly trained professionals to take a pay cut.

If all the health plans must cover all the same services, why aren’t all the Bronze, Silver, Gold, and Platinum metal tiers from all the different insurance companies the same? While there can be savings from the type of plan offered – HMO, EPO, PPO -, the health insurance premiums are tied to contracted reimbursement between the insurance company and the providers.

The simplest model is Kaiser Permanente. Kaiser health insurance contracts with the Kaiser hospital system and the Kaiser doctor medical groups. Each service provided by the hospital or doctor has a set reimbursement rate.

It gets more complicated when the health plan is a PPO that contracts with multiple hospitals and medical groups. If the PPO plan wants certain hospitals and doctors in-network, they may have to pay more for those services. The bottom line is that health plan may pay a lower amount for the exact same health care service you receive if you receive the service from one hospital over another.

Hospitals

For better or worse, some hospitals and medical groups command higher reimbursement rates for services because of their popularity, reputation, and renown. If more of the health plan members receive cancer treatments from higher cost providers, the health plan will pay more in claims than if the patient went to a lower cost facility.

Regardless of the provider, delivering health care in the United States is expensive. Hospital systems have labor costs such as nurses, clerical staff, facility engineers and maintenance. Hospitals also have debt for acquiring the latest imaging technology machines and expansion of facilities. It is difficult, to nearly impossible, to mandate that hospital systems charge less for their services when they have budgets and debt service that stretches into the future.

Medical Groups

Medical groups, comprised of doctors and support staff, have expenses for salaries and facilities. Similar to hospitals, the reimbursement rates for medical group services reflect the cost of doing business. Yes, doctors can receive large salaries for their services. I’ll let you tell the cardiologists, oncologists, or dermatologists that they should charge less for their services.

The health plans routinely have bitter negotiations with hospital systems and medical groups. The health plans want to reimburse a lower amount for services, and the providers want a higher amount. Eventually, they either compromise or the health plan drops the providers from their network.

In general, the cost to deliver health care services is more expensive in Northern California than Southern California. We see this reflected in the health insurance premiums. A 40-year-old individual in Southern California will pay a monthly premium for a Blue Shield Bronze 60 PPO plan of approximately $635 a month.

If that same individual moves to Northern California the monthly premium for the exact same plan can be $150 higher at $790. The plan benefits are the same. However, the potential for health care claims with more expensive providers is reflected in the monthly premiums.

Medical Loss Ratio Explained

The insurance companies collect billions of dollars in premiums. The assumption is that the vast sum of revenue goes into corporate profits because the average person makes no health care claims but pays high premiums. With ACA individual and family plans, the insurance companies must spend 80 percent of premium dollars on health care claims and quality improvements. This is known as the medical loss ratio.

Under the medical loss ratio, insurance companies can spend 20 percent of premium dollars on marketing, operations, and administration. As an insurance agent, I’m part of the marketing. California health plans pay an average of $17 per person per month commission to agents for each enrollment. A large portion of the 20 percent goes to operating the health insurance such as enrollment, customer service, and claims processing.

Another cost for the health plans is if the enrollment goes through Covered California. The health plans pay Covered California approximately 3 percent of the full premium amount to Covered California. The carrier fees fund Covered California’s operations and marketing.

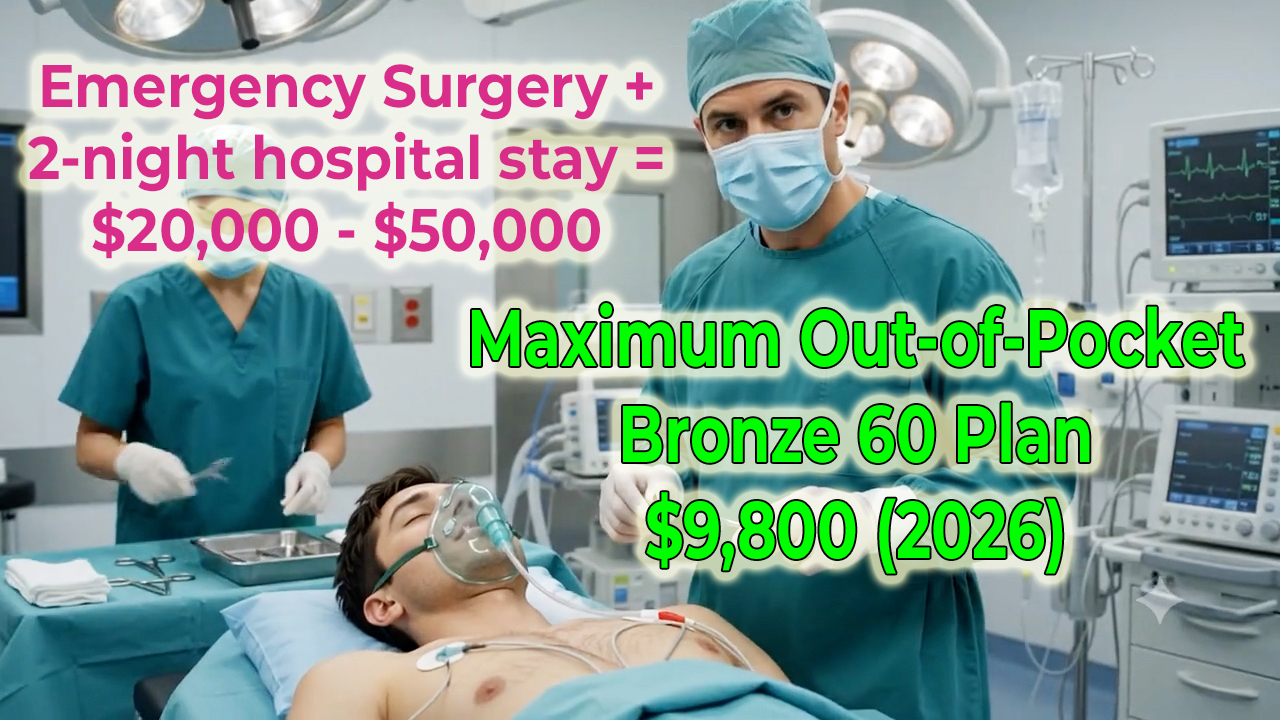

While health insurance premiums are high, the value proposition is that a health plan protects you against exorbitant health care expenses. It is estimated that an emergency room surgery followed by a 2-night stay in a hospital costs between $20,000 to $50,000. Regardless of what hospital you are taken to, if you have a Bronze 60 plan, your maximum liability is $9,800.

The health plan will pay all health care expenses over $9,800 for the remainder of the year. Most people would spend $9,800 to save their life or that of a family member. The rates for health insurance could be reduced IF the maximum out-of-pocket annual amount was raised to $20,000. This, of course, is just cost-shifting. The plan member pays more – or all – of the costs of the health care services and the health plan pays less.

YouTube video review why health insurance is expensive.