When it becomes apparent your income is increasing more than your Covered California income estimate, reporting the higher dollar amount poses an ethical dilemma for some individuals and families. The higher income means a reduction in the monthly subsidy to lower the health insurance premiums and possibly losing low copayments of an enhanced Silver plan.

The good fortune of a higher annual income comes with the cost of higher health insurance premiums. The increased income estimate also means that an individual or family enjoying the lower copayments, coinsurance of the Silver 94, 87, or 73 health plans may see their health care costs increases.

To Report or Not, the Ethical Dilemma

The ethical dilemma or conflict occurs because the household has agreed to report increased income streams, which will necessarily translate into higher health care costs. It is normal consumer behavior to minimize costs while maximizing benefits of any goods or services. The decision to report a higher income is clouded by issues such as the income is only an estimate and excess subsidy (Advance Premium Tax Credit) will be captured when the household files their federal income taxes.

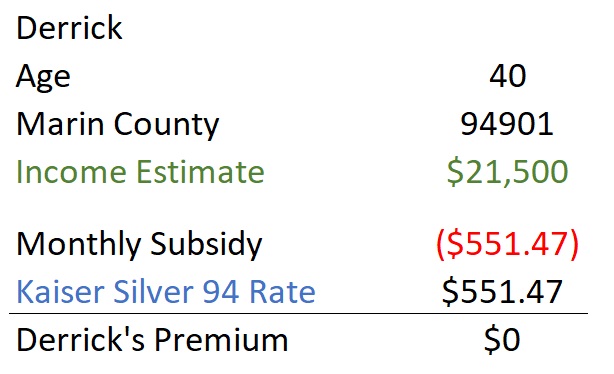

As an example, let us consider Derrick, a landscaper in Marin County. He is 40 years old and estimated his income $21,500 for the next year. Covered California determined that Derrick was eligible for a subsidy of $551.47 per month that was equal to his Kaiser Silver 94 health plan. Derrick’s health insurance premiums beginning in January were $0.

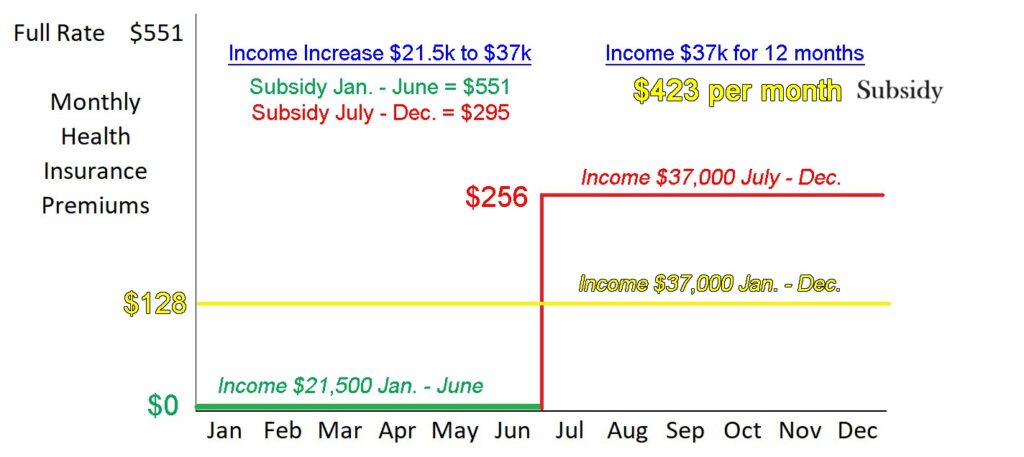

Income Increase Drastically Increases Monthly Health Insurance Premiums

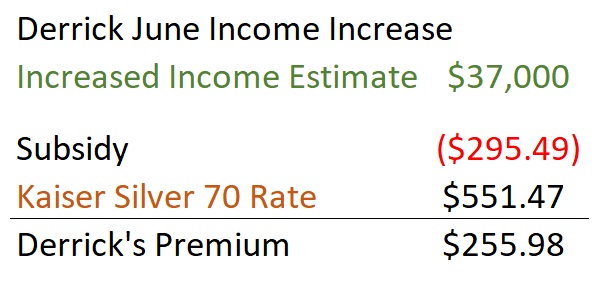

Derrick’s business began to pick up in the first part of the year with new accounts and a few side jobs. In June he reported an increase to his annual income estimate to $37,000 in his Covered California account. His subsidy dropped down to $295.49 and his health insurance premium jumped from $0 to $255.98 per month. In addition, Derrick lost the Silver 94 and was moved to a Silver 70 Kaiser plan.

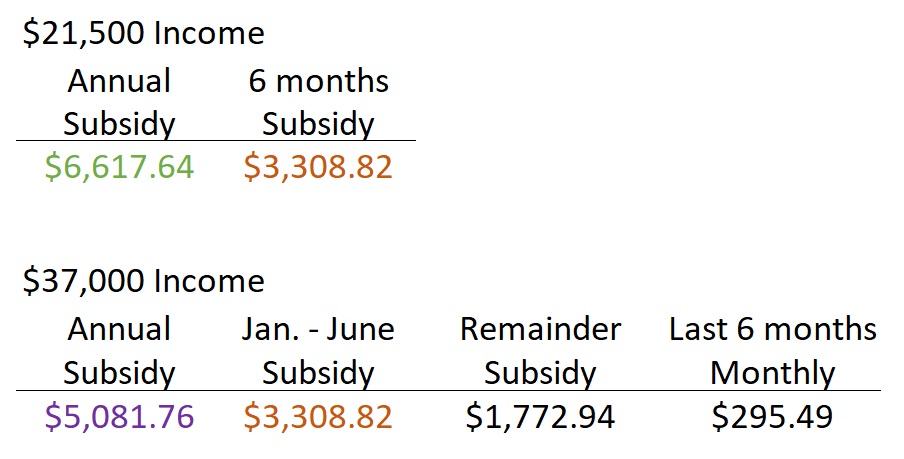

The drastic increase to Derrick’s health insurance premium occurred because he had used a lot of the larger subsidy based on the lower income in the first half of the year. At $21,500, Covered California determined Derrick was eligible for a $6,617.64 annual subsidy or $551.47 per month. At the higher income of $37,000, Derrick is only eligible for an annual subsidy of $5,081.76.

Covered California must subtract the subsidy Derrick already received under the lower income amount for the first 6 months of the year, $3,308.82, from the lower annual subsidy amount. The remainder is $1,772.94, that is then divided by 6 for the last six months of the year. This results in a monthly subsidy of $295.49.

If Derrick would have been able to predict his income would be $37,000 at the beginning of the year, his monthly subsidy would have been $423 ($5,081.76 divided by 12 months) and his monthly premium would have been $123 for all 12 months.

Income Increase Moves Household from Silver 94 to Silver 70

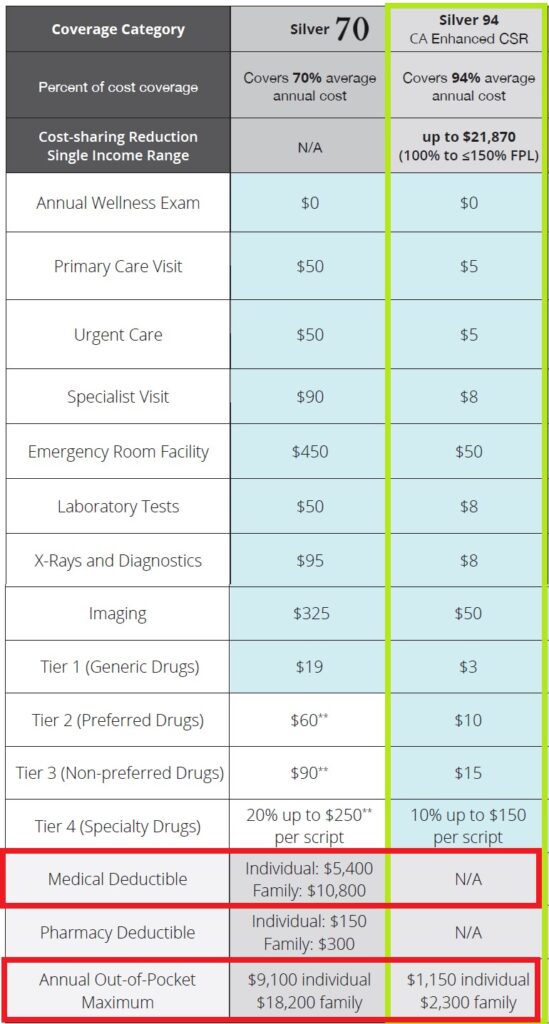

The second hit Derrick took by reporting his higher income was moving from the reduced cost-sharing Silver 94 to Silver 70. Derrick’s primary care visits jumped from $5 in June to $50 in July. All of his other health care costs also increased. In addition, Derrick is now subject to a $5,400 medical deductible if he hospitalized. His annual maximum out-of-pocket amount went from $1,150 under the Silver 94 to $9,100 under the Silver 70.

If Derrick does not report the increase of income during the year, he will be subject to repaying part or all the excess subsidies when he files his federal income tax return. There is no mechanism to recapture the reduced cost-sharing for the health care services under the Silver 94 plan.

Regardless, the drastic increase in the monthly premiums and loss of the reduced cost-sharing Silver plan is enough to give any rational person pause before they report the change to Covered California. It creates an ethical dilemma between complying with the Marketplace Exchange agreement to report changes to the income and the very real financial cost to the household.