PPO health plans can have monthly premiums 50 percent higher than the least expensive HMO plan in the same metal tier in parts of California. Why are PPO health plans so expensive, or conversely, why are HMO plans so inexpensive relative to PPO plans? Some of the reasons for the premium differential lies in the health care model, provider network, and patient behavior.

EPO and PPO Plans Usually More Expensive Than HMO Plans

The Affordable Care Act mandates two important conditions upon individual and family health plans. First, health plans must spend 80 percent of their premium revenue (also known as the medical loss ratio) on patient health care and quality improvement. Second, health plans have to be designed to meet certain criteria for the metal tier levels of Bronze, Silver, Gold, and Platinum. Regardless of whether the health plan was an HMO or PPO, it had to meet the spending requirements and metal tier actuarial value.

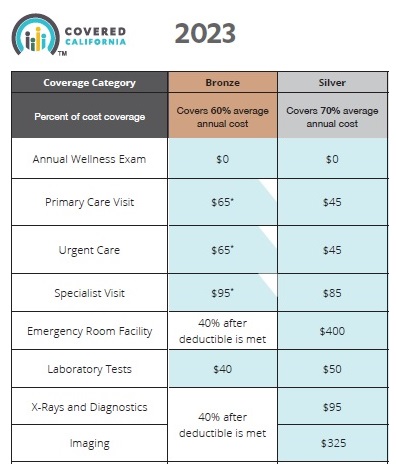

Covered California has gone even further by regulating that all metal tier plans have the same standard benefit design for member cost sharing regardless of whether the health plan is an EPO, HMO, or PPO. For example, a member of a Silver 70 plan will pay $45 for an office visit, $85 for a specialist visit, $50 for laboratory tests, and $95 for an X-ray for 2023. This is irrespective of the health plan type of EPO, HMO, or PPO.

Even with the medical loss ratio mandate on patient spending and set copayments, coinsurance, and deductibles by metal tier, we still find large disparities in the monthly premiums for what looks like the exact health plan. How can a PPO health plan have a monthly premium that is 70 to 90 percent higher than the least HMO plan offered?

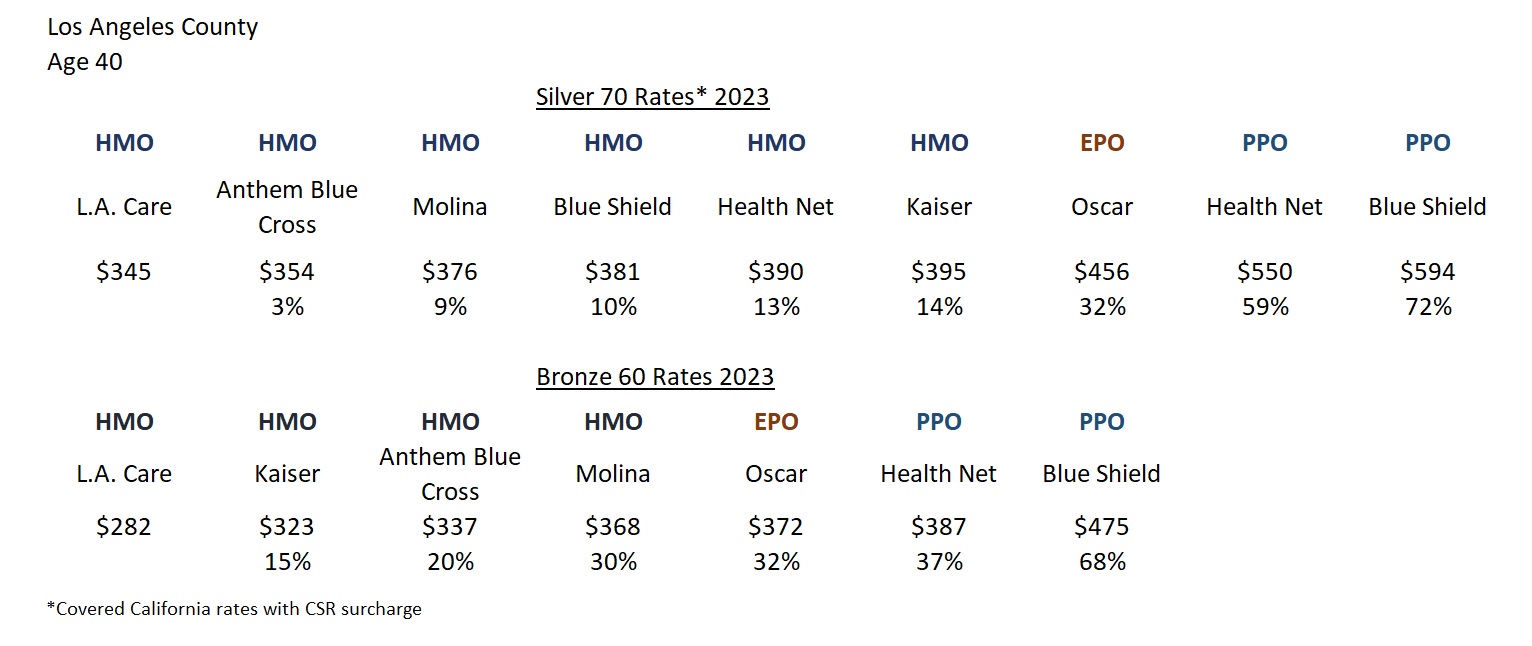

In Los Angeles County, for a 40-year-old individual, the EPO and PPO plan rates (before any subsidy) are 32 to 72 percent higher than the least expensive HMO plan offered. The rate differential was also found in the Bronze plan where they were 32 to 68 percent higher. Note that Blue Shield offers a very competitively priced HMO plan which indicates that it is the plan model – not carrier greed – that is driving the rates.

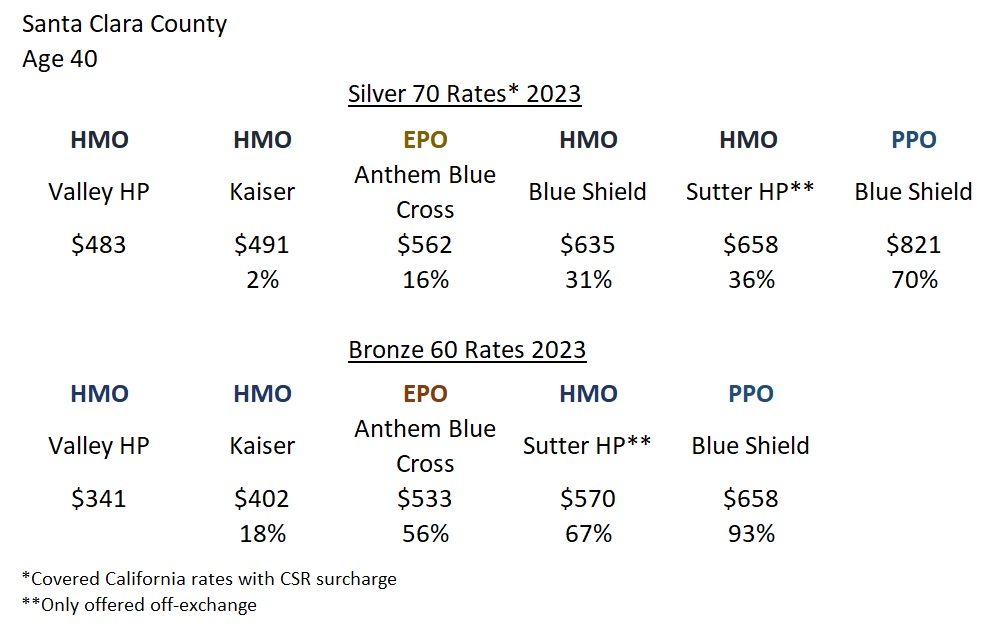

While a similar rate differential was found in Santa Clara County for a 40-year-old individual, there are some anomalies. The most expensive PPO plan in Santa Clara County, for the 40-year-old before any subsidies, was 70 percent higher for the Silver 70 and 93 percent higher for the least expensive Bronze plan. The Blue Cross EPO Silver and Bronze plan stands out as a good value. While still more expensive than two of the HMO plans, the Blue Cross EPO is less expensive than some other HMO plans with a large network of providers.

The Sutter Health Plan HMO is not offered through Covered California and is not eligible for any subsidies. The big selling feature for the Sutter HMO, and reason for the relatively higher premium rates, is access to Sutter doctors and hospitals. The Sutter Bronze and Silver HMO plans have the exact same standard benefit member cost sharing and covered services as the other plans offered in the region.

Cost Containment of HMO Health Plans

Aside from those regions who may offer an EPO plan at a very competitive rate, PPO and EPO plans consistently are more expensive throughout California. There are some fundamental differences in plan types that translate into in lower costs for some the health plan models.

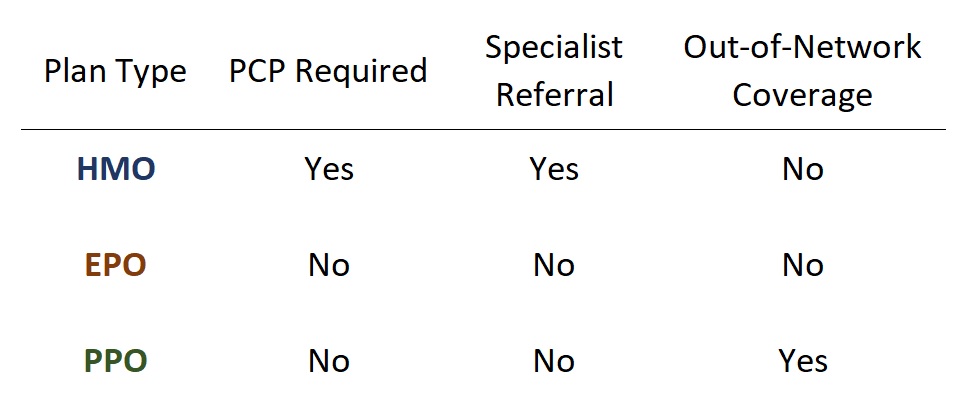

HMO: health maintenance organization. HMOs require you to select a Primary Care Physician (PCP) and visit that doctor for most of your initial health care services. In order to see a specialist (excluding OBGYN), you must see your PCP for a referral. There is no out-of-network coverage with an HMO. If you visit a health care provider (excluding emergency and urgent care) not in the health plan’s network or without a referral, the HMO will never cover any of the cost of the service.

PPO: preferred provider organization. The PPO plan member can select any network provider to receive health care services. No PCP is required for most specialist appointments. The PPO will share in the cost of out-of-network services after an out-of-network deductible is met.

EPO: exclusive provider organization. EPO plans mirror PPO plans except they have no out-of-network coverage.

California is dominated by HMO plans in the larger population regions of the state where health plans can operate an HMO plan type. We also see a couple of the carriers (Anthem Blue Cross and Blue Shield) that offer both HMO plans and either an EPO or PPO plan. This is a signal that HMO plans do contain health care claims resulting in lower premiums in many instances.

Within the HMO plan model, the health plans pay a monthly capitation dollar amount to the medical group of your selected PCP. Whether you see your PCP or not, the medical group is paid the capitation amount every month. In return for the regular capitation amount, the medical group agrees to provide some services without filing a claim or reduced cost to the health plan. It can be that your PCP visits are not reimbursed by the health plan. The doctor’s office or medical group may only receive your set office visit copayment.

In most cases, the PCP can address most health care concerns without the need for involving a specialist. For example, I lost hearing in one of my ears. The PCP quickly diagnosed the problem and blasted the wax plug from my ear. Hearing restored. I could have gone to an ear, nose, and throat (ENT) specialist and had the same procedure. Of course, the resulting cost to me and the health plan would have been higher.

If I did need a referral to a specialist, it would have been first within the medical group of my PCP, then to an outside provider that was also contracted with the HMO plan. You can think of an HMO as a funnel where you are being directed to the various providers (doctors, labs, tests, imaging, specialists, facilities, etc.) to meet your health care needs.

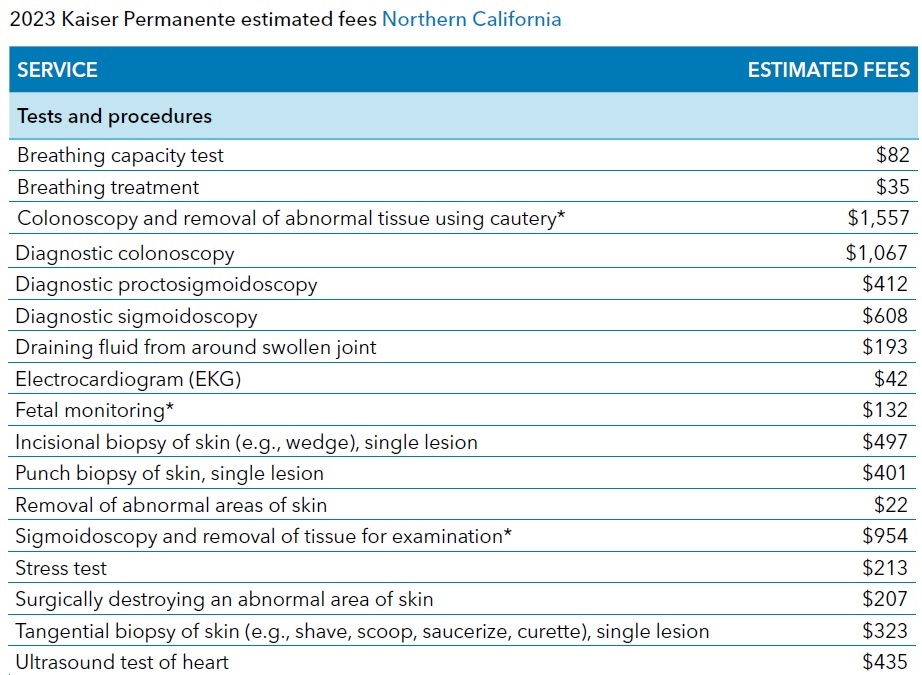

The ultimate example of this health care flow is Kaiser Permanente. A testament to the cost containment of the HMO model is not only the lower health insurance premiums but also the fee schedule that Kaiser publishes with rates for routine services that seem reasonable.

Pharmacy Costs Increasing For All Health Plans

The cost of prescription medications sucks a large and growing percentage of health insurance premiums. However, there is no available data to suggest PPO plans have higher drug costs than HMO plans.

Larger EPO and PPO Provider Network for Health Care Services

Many HMO plans are limited to small geographical region, which limits their provider network. L.A. Care operates only in Los Angeles County. Sharp Health Plan is limited to San Diego County. Valley Health Plan operates only in Santa Clara County. Other health plans operate across few different counties such as CCHP and Western Health Advantage. The limited footprint of some of the HMO health plans helps control costs by reducing the number of providers in their network.

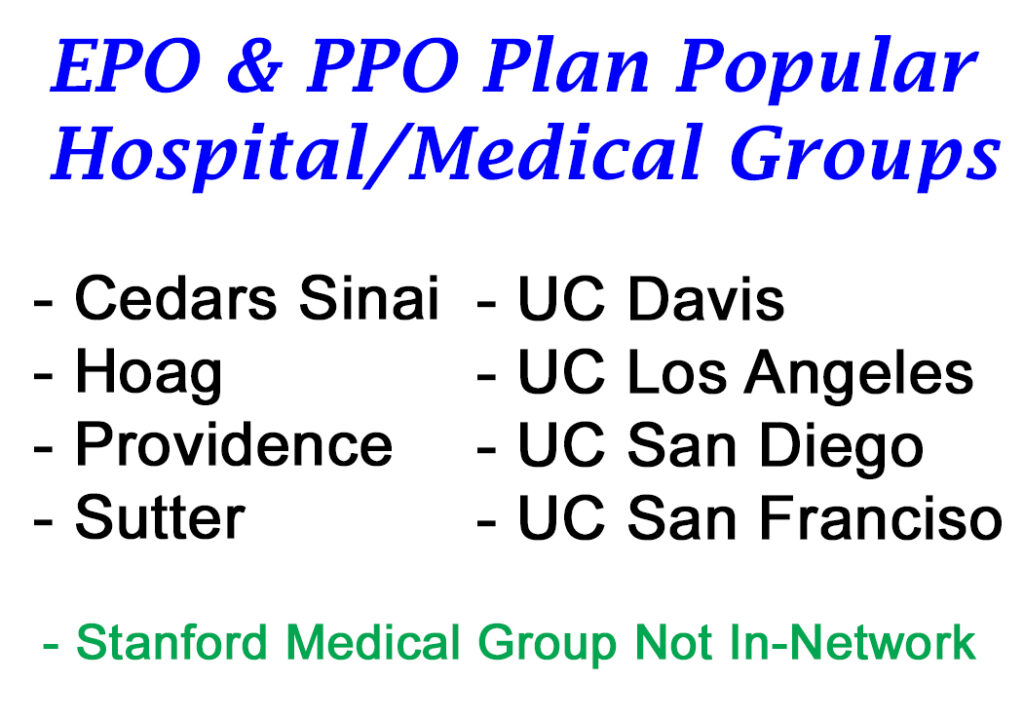

PPO and EPO plans generally have a larger network of hospitals and medical groups. They will include popular providers such as Cedars Sinai, Hoag, Providence, Sutter, and UC hospitals and medical group. The members of PPO and EPO plans can travel great distances to see their favorite specialist.

There is a limit to the provider networks of the PPO plans. There is no individual and family plan PPO plan that offers Stanford medical group and hospital. The lack of Stanford is probably a combination of the higher reimbursement rates Stanford may seek for their services and their popularity as a health care provider.

Consumer Behavior

It is simple consumer economic behavior that, given an option at the same cost, the health care consumer will select whom they feel provides the best value. Large medical groups and hospitals engage in marketing to tout themselves as the best health care provider. Some of these organizations are leaders in the treatment of certain illnesses. If the cost of an office visit is $45 regardless of whether you visit the local clinic or world renown medical office, many people will opt for the more famous provider.

The more popular, famous, prestigious medical groups and hospitals also command the highest reimbursement rates from the health plans. If a PPO wants Sutter, UC Davis, Hoag, and UCSF in-network to attract plan members, they must recognize they will reimburse those providers for their services at a higher dollar amount for certain services. Consequently, the EPO and PPO plans will see their members gravitate to higher cost providers, even when the member pays the same amount for the services. However, the cost to the consumer is in a higher health insurance premium for the availability of those providers.

For example, the 2023 Northern California Kaiser HMO fee schedule states that an eye exam for a new patient is $254. Under the Silver 70 plan, the specialist visit for an ophthalmologist would be $85. The health plan picks up the other $169 ($254 – $85.) If the patient selects an ophthalmologist for their EPO or PPO network from a popular medical group, the cost of the eye appointment may be $300. The patient only pays the $85 copay. The health plan pays $215 ($300 – $85.) While the $45 difference between the HMO reimbursement rate and the PPO cost may not seem like much, when you spread the increased costs over thousands of plan members, it adds up. The result is that the PPO and EPO must charge a higher rate to sustain paying out the claims.

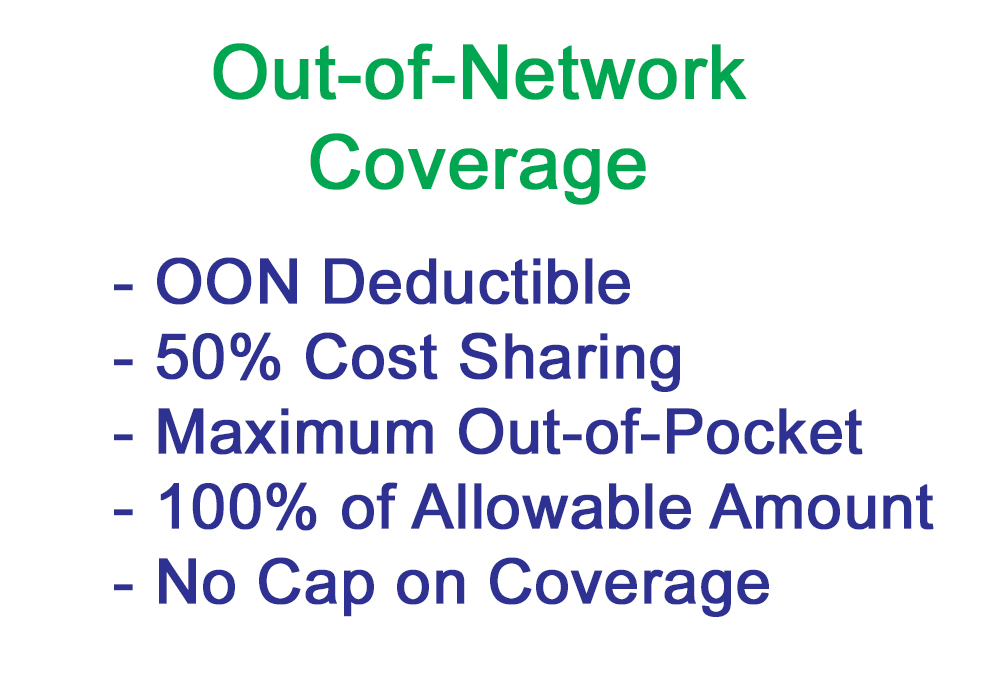

Out-of-Network Coverage

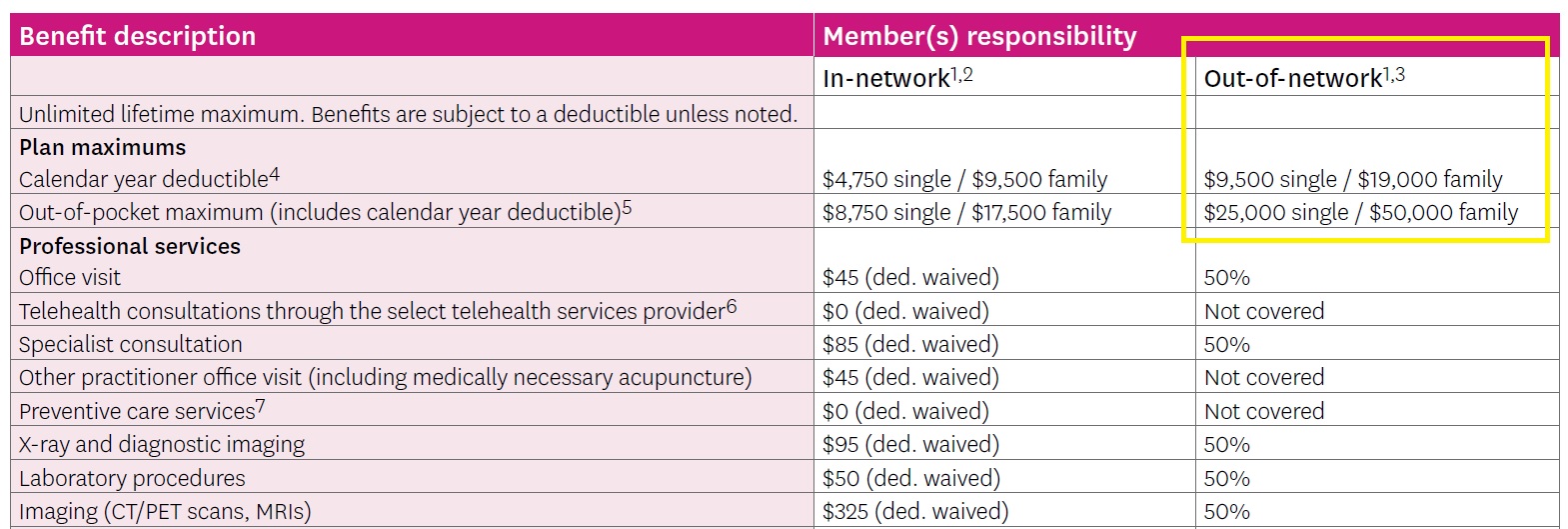

PPO plan members get a benefit that the other plan types do not offer and that is out-of-network coverage. After meeting a hefty out-of-network deductible, the PPO plan will share 50 percent of the allowable amount for the out-of-network services. Once the out-of-network maximum amount is met, which is also a very large dollar amount, the PPO will pay 100 percent of the allowable amount, with no cap.

It is not advisable to use the out-of-network benefits for routine health care services. Individuals and families use the out-of-network benefits when someone’s life is at stake and they want a doctor and/or hospital to perform lifesaving treatment or surgery. If the treatment costs half a million dollars and the family pays only 10 percent of the cost, many would view that as a good value. However, the PPO plan is on the hook for the other 90 percent of the out-of-network health care services.

To circle back to the original question of why PPO plans are more expensive than HMO plans, the answer is found in the higher costs incurred under the PPO plan. Members can see more specialists that may also command higher reimbursement rates. Some PPO plan members also take advantage of the out-of-network benefits that can be very costly to the health plan. Taken altogether, PPO and EPO plans must price their plans to cover the potential higher costs.

This is not to say that PPO and EPO plan members receive better health care or have better treatment outcomes over HMO plans. HMO plans have great doctors and hospitals able to treat a wide variety of health care challenges. It is just the case that some people would like to direct their own health care journey under a PPO or EPO plan as opposed to working with a Primary Care Physician.