When individuals and families increase their income estimate in the Covered California application, they can notice a dramatic drop in the subsidy. The drop in subsidy seems disproportionate to the income increase. There are 2 elements of the subsidy calculation at work. First, the increase of income changes the household consumer responsibility percentage. Second, the household received lots more subsidy with the lower income and there is little left for the remainder of the year.

Some families are surprised that when they increased their income estimate in the Covered California application, they lost all subsidies for the remainder of the year. In other words, they had to pay the full health insurance premium for the remaining months. This is because they had received all the Advance Premium Tax Credit subsidy they were eligible for at the higher income estimate.

Increasing Income Results in Dramatic Drop of Health Insurance Subsidy

The dramatic loss of subsidy to reduce the monthly health insurance premiums is a direct result of a change to the consumer responsibility percentage and the subsidy amount the individual or family has already received. A case study will illustrate how the Affordable Care Act calculates the subsidy with changes in the middle of the year.

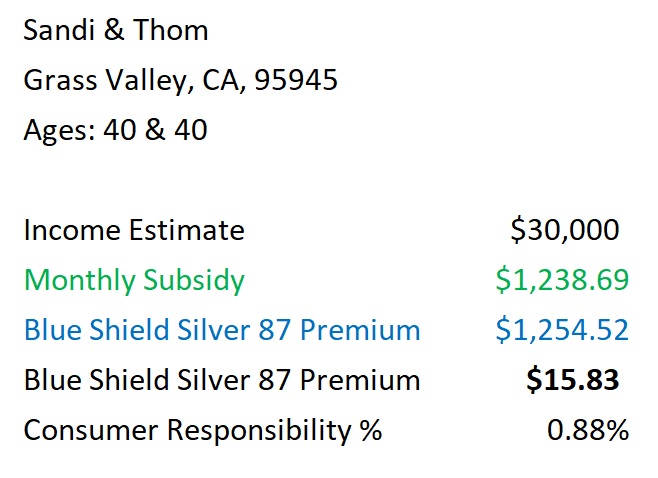

Sandi and Thom, a 2-person household, live in Nevada County, zip code 95945. They enrolled into Covered California for 2023 plan year with an estimated household income of $30,0000. Both Sandi and Thom are 40 years old.

Covered California determined they were eligible for a monthly Advance Premium Tax Credit subsidy of $1,238.69 and enhanced Silver 87 plan with lower consumer cost sharing. Sandi and Thom chose the second lowest cost Silver plan. After the $1,238.69 subsidy, their monthly health insurance premium for the Blue Shield PPO Silver 87 was $15.83.

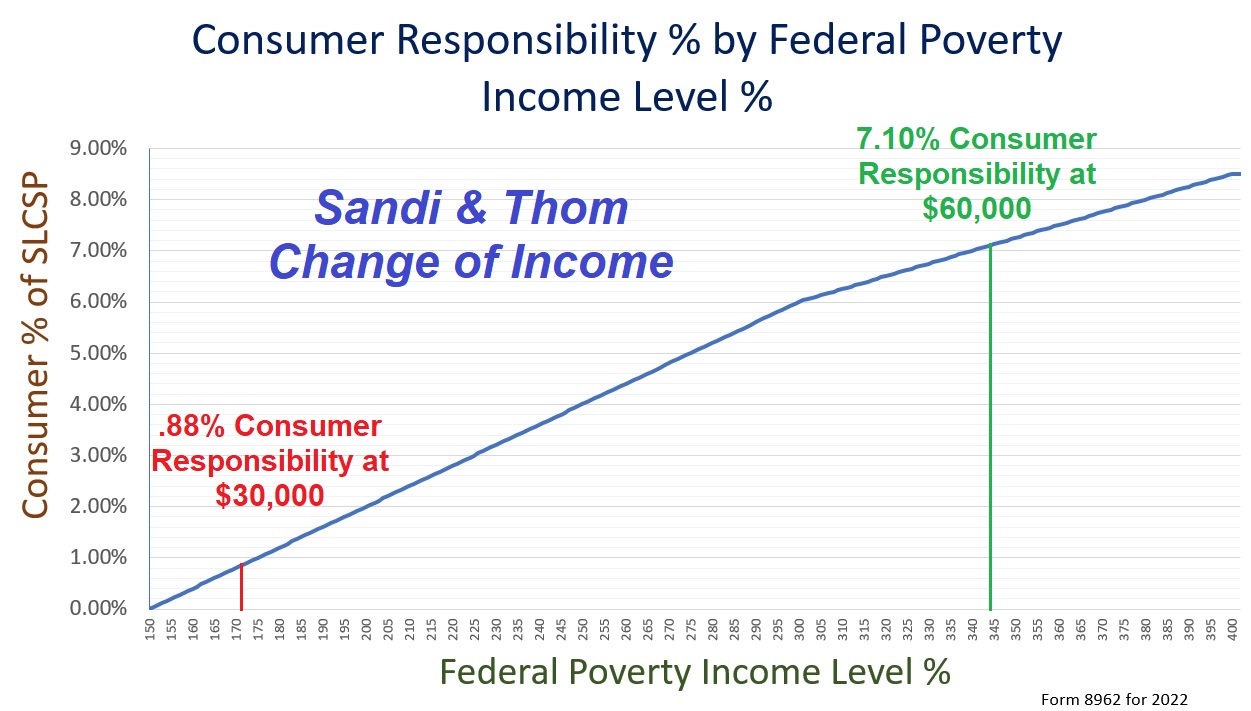

The Covered California application calculates the monthly subsidy based on Affordable Care Act rules that are outlined by the Internal Revenue Service form 8962 Premium Tax Credit reconciliation. Their household income was 172 percent of the federal poverty level. ($30,000 divided by FPL for household of 2 of $17,420.) The applicable figure from form 8962 is .0088. This translates into a consumer responsibility percentage of .88 percent.

Consumer Responsibility Percentage Increase

The applicable figure is also the consumer responsibility for their fair share of health insurance premiums. For Sandi and Thom they should spend no more than .88 percent of their household income for health insurance. The Advance Premium Tax Credit subsidy is to make the monthly premiums for the second lowest cost Silver plan no more than the consumer’s fair share responsibility. Sandi and Thom’s subsidy was $1,238.69 making their monthly health premium $15.83.

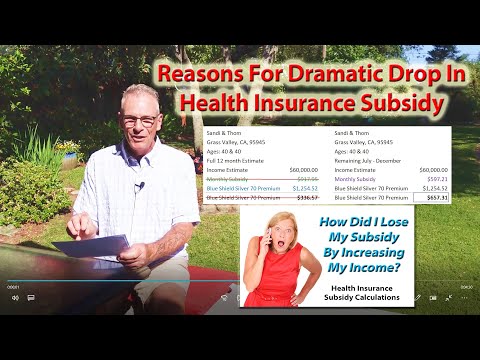

In June, Sandi and Thom report an increased income estimate from $30,000 to $60,000 for 2023. That changes their consumer responsibility percentage for their health insurance from .88 to 7.10 percent of their household income.

Inaccurate Shop & Compare Tool Estimate

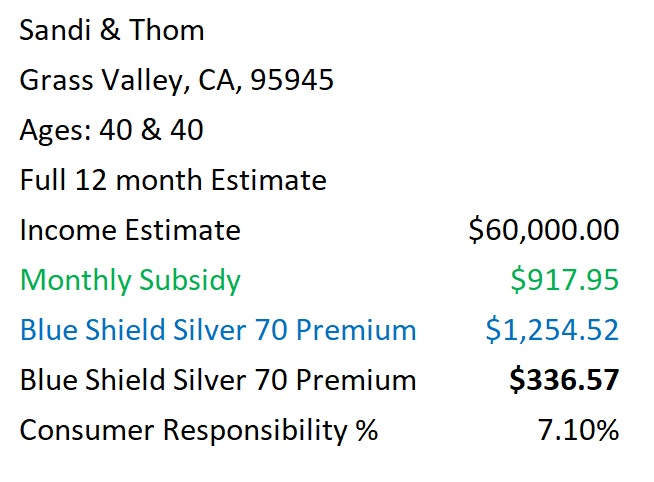

They used the Covered California Shop and Compare tool to determine how much their new premium would be. For a full year, the monthly APTC subsidy would have been $917.95, a decrease of $320.74 with the lower $30,000 income estimate. Based on a full year, Sandi and Thom’s Blue Shield Silver plan would have been $336.57 per month. But the calculation is inaccurate because it does not include the subsidies Sandi and Thom already received at the lower income.

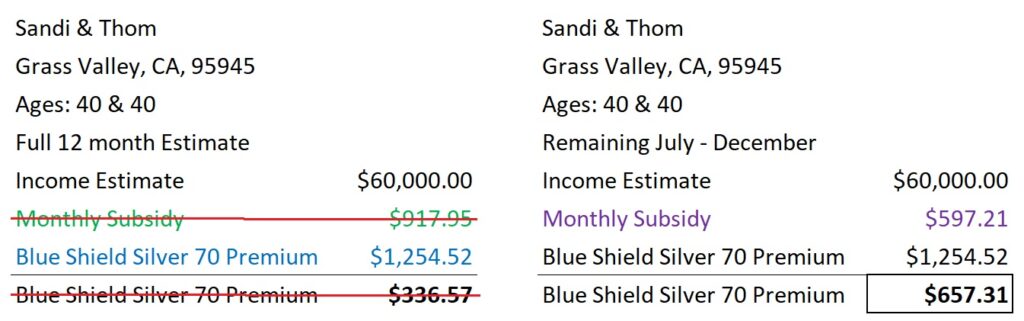

When the income estimate was increased in their Covered California application, the subsidy was properly calculated for the remainder of the plan year. The first thing Sandi and Thom notice is that they lost the Silver 87 plan and with the higher income are now only offered a Silver 70. Another disturbing problem for them is that instead of $336.57 monthly premium, their new premium for the Silver 70 is $657.31. They went from paying $16 a month for a great Silver 87 plan to $658 per month for Silver plan that has higher copays, coinsurance, and deductibles.

Subtraction of Previous Premium Tax Credit Subsidy

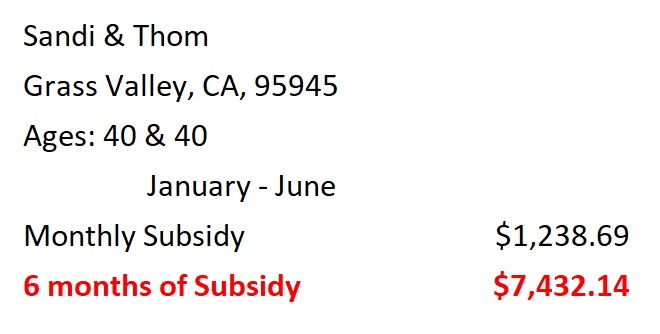

The monthly premium can be traced to the accounting of the annual subsidy amount. At $30,000, Sandi and Thom’s annual Premium Tax Credit subsidy was calculated at $14,864.28 that translates into $1,238.69. Through the end of June, when they increased their income, Covered California forward $7,432.14 on their behalf to the Blue Shield PPO plan.

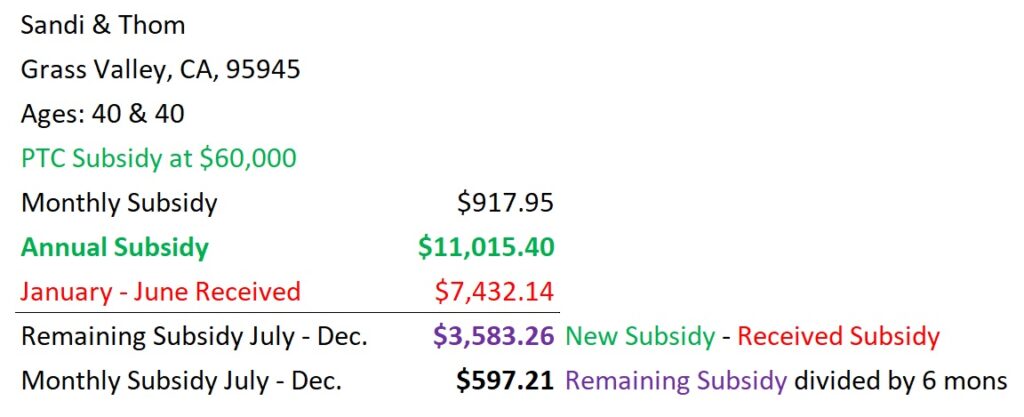

With the higher income estimate of $60,000 and higher consumer responsibility percentage, Sandi and Thom are only eligible for an annual Premium Tax Credit subsidy of $11,015.40. To make sure Sandi and Thom don’t receive too much subsidy at the higher income estimate, Covered California subtracts what they have already paid on behalf from the new annual amount ($11,015.40 – $7,432.12 = $3,583.26.)

This subtraction only leaves $3,583.26 to be for distributed over the remaining months of enrollment, July through December. The final subsidy applied to the health insurance premium is $597.21 making the monthly premiums $657.31. The final premium is double what the Covered California Shop and Compare tool predicted. However, the Shop and Compare Tool does not know how much subsidy had already been expended on the couple’s behalf.

Moving to a different region with lower health insurance rates

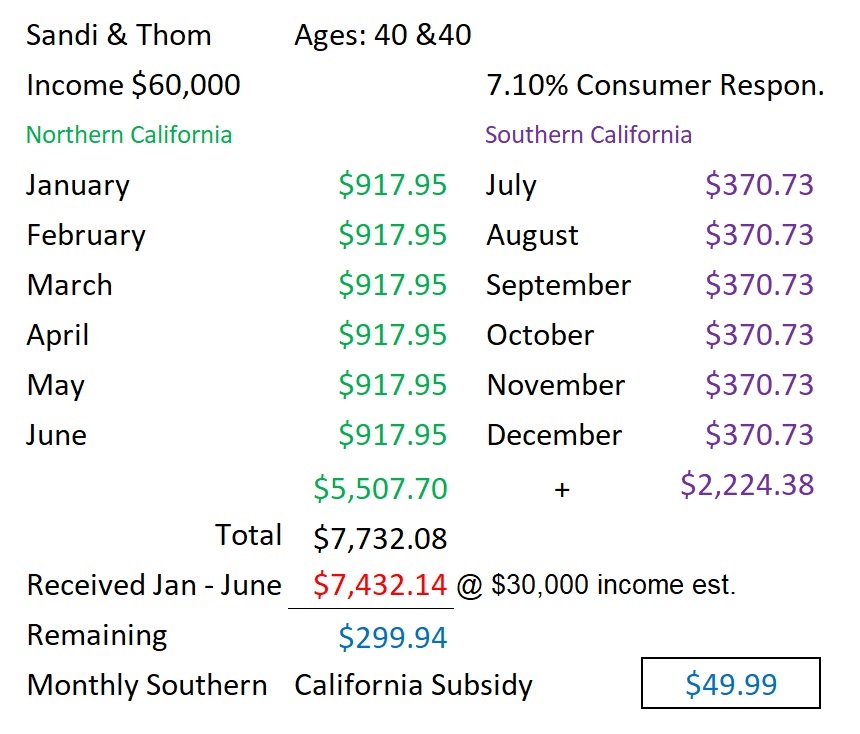

If Sandi and Thom move to Southern California, the results are worse. Because the health insurance rates are lower in Southern California, Sandi and Thom would only be eligible for $7,732.08 annual Premium Tax Credit based on Northern California and Southern California health insurance premiums, which are lower in Southern California. In Northern California they were eligible for $917.95 per month. In Southern California they are only eligible for $370.73 per month with the same 7.10 percent consumer responsibility.

Covered California must subtract the $7,432.14 Sandi and Thom already received at the lower $30,000 income from the revised Premium Tax Credit subsidy estimate of $7,732.08. This leaves a balance of $299.94 for Sandi and Thom to reduce their health insurance premiums. The $299.94 is divided by 6 for the remaining 6 months of the year for a monthly subsidy of $49.99.

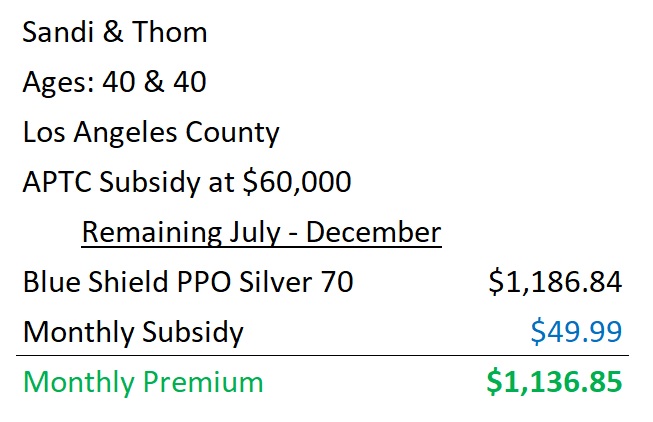

Sandi and Thom can then apply that $49.99 subsidy to the Blue Shield PPO Silver 70 in Los Angeles County. However, the monthly premium for Sandi and Thom will be $1,136.85 because there is so little subsidy left to lower the premium. At this point, Sandi and Thom should look at lower cost health plans in their new region.

The dramatic drop in the Advance Premium Tax Credit subsidy when the household income increases or the family moves to a different region is make sure the household does not have to repay a large amount of excess Premium Tax Credit by to the federal government when they do their taxes.