Are Covered California SHOP enrollment projects inflated to meet the budget?

Covered California staff is forecasting that SHOP enrollment will double by the end of 2014 and double again during open enrollment for 2015. A list of assumptions was given for the stellar forecast enrollment during the May 2014 Board meeting where the topic was revenue projections from fees charged on individual small group members. Based on the current experience of agents and SHOP groups, such an optimistic projection may not be achievable.

AreSHOP enrollment projections over estimated?

Here are their assumptions for increased enrollment from the 2015 Enrollment Forecasts presented at the May 2014 Covered California Board meeting. Download the presentation at the end of the post.

The Medium enrollment forecast reflects the following major assumptions:

SHOP enrollment support improves and brokers gain more confidence in selling SHOP policies.

As of June 5th, five months after the first SHOP plans went into effect, agents haven’t received commissions on groups they helped enroll. There is no bigger disincentive to representing a product or carrier than the failure to be paid the agreed upon commission. Heap on top of that confidence crushing problem the ongoing invoice issues. SHOP currently is having problems migrating groups with January and February effective dates into the new billing system. This integration problem has left groups with invoices that have yet to be corrected and are paying for members who don’t want the coverage. Like I told the Board in my public comments, I have a small group right now and Im not going to take SHOP to them because I cant get my one SHOP group completely through the process correctly.

The overall small group market continues to shrink.

This assumption in support of increasing SHOP enrollment seems contradictory. Perhaps they mean that the plans offered by the different carriers continue to shrink. However, whether the market or the number of plans is shrinking, SHOP offers nothing that would fill the vacuum of a shrinking market or plans that arent already being offered. SHOP doesnt even have Anthem Blue Cross as a plan offering which is a significant hole in its own portfolio.

Market share will increase in 2016 when employers with up to 100 employees will be eligible to participate.

At the close of open enrollment, SHOP had 1,156 small groups representing 4900 employees. That is 4.24 employees per group. If SHOP isnt attracting the 30 to 50 employee small group, why do they think that groups of 100 employees will suddenly want to sign up? In addition, many other analysts are forecasting an overall move away from offering group health benefits to employees. Their next assumption seems to refute their large employer migration premise.

High retention rate of existing policies.

Health insurance companies do experience a relatively high retention rate among their small groups. That reduces the possibility of groups larger than fifty employees, or any small group, from changing carriers and moving to SHOP. The analysts at SHOP seem to be severely underestimating the determination of agents and carriers focused on keeping their clients. Of the 1,156 employers with SHOP, I would guess that many were new to the small group health insurance market. If my guess is correct, it indicates that SHOP picked up enrollments based on the tax incentives and a new marketing approach and they didnt pry small groups away from their existing plans.

Strong new enrollment during the 4th quarter of each year.

This isnt an assumption,it’s a day-dream. They forecast that SHOP employee enrollment will balloon from 4,900 to 8,800 by the end of FY 2013-14. Thats a 44% increase in a program that as of June can’t deliver a correct invoice to their groups. Perhaps they are assuming a baby boom amongst the current members. But the presentation for the projectionsof SHOP start off with the point of fact statement

Enrollment in SHOP nationally and in California is substantially lower than previously estimated. The updated enrollment forecast is based on experience to date, anticipated program changes to make SHOP more competitive and expert input regarding likely changes in the small employer market.

The SHOP folks have bought the message that their experts gave and they wanted to hear, specifically, they are going to be a big success. That is what consultants get paid to say because they dont have to bear the burden of the failure.

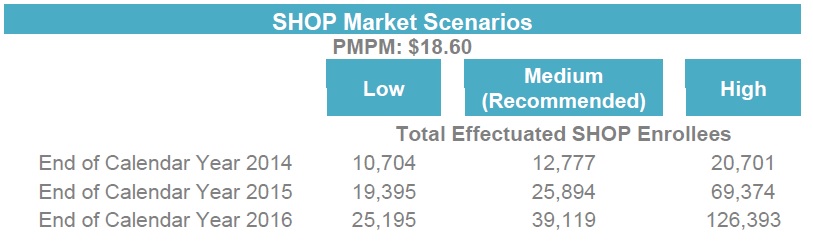

2015 Covered California SHOP enrollment projections.

Can SHOP grow by 44% in six months?

These projections are very import to the Covered California and their viability to maintain operations. Covered California must be self-sustaining in 2015. Their revenue to maintain operations is based on the monthly fee assessed on all enrollments: $13.95 per person in an individual family plan and $18.60 per employee in a small group plan. Under the Medium or Recommended enrollment projection scenario they have SHOP reaching 12,777 employees by the end of 2014 and producing $237,652 per month. If the current SHOP enrollment stays steady at 4,900 through 2014 the monthly revenue will be approximately $91,140.

Are rosy projections based on reality?

Even if SHOP doubles in enrollment to 9,800 at the end of 2014, they have missed the low estimated projection of 10,704. The medium projection has SHOP enrollment at 25,894 by the end of 2015. That is double the 2014 enrollment which means double the revenue. Fortunately for Covered California missing their target enrollment numbers is not terribly critical since the SHOP revenue is less than 2% of the overall budget. But that still doesnt excuse the overly rosy enrollment projections that dont seem to be based on reality.

SHOP promise and website crashed

SHOP can be a force in the small group market, but they will really have to work. The tax credit for the employer can be an incentive along withthe selling feature that each employee can select the carrier they want. The problem for SHOP is that this feature is already offered by California Choice, along with a billing system that works, Anthem Blue Cross plans, plus dental and vision insurance plans. The attraction for agents was having an enrollment portal and dashboard to manage numerous small groups in one place. Alas, the SHOP website was such a mess that it was taken off-line with a promise of a return in the fall of 2014. The advantages SHOP offered have evaporated due to either poor planning, management or both.

June 2014 SHOP status

This is what we know

- Covered California SHOP got half the enrollment they anticipated for the 2013-14 open enrollment period.

- The SHOP website crashed leaving groups and agents stranded.

- SHOP continues to have problems generating correct invoices six months after their launch.

- Agents have yet toreceive any commissions for the small groups they helped enroll.

- SHOP doesnt offer Anthem Blue Cross or dental and vision plans to small groups.

Making SHOP acompetitor

With all this negative information Covered California still believes SHOP enrollment will double by the end of 2014. Like I told the Board, You might want to hedge your bets on the SHOP enrollments. Short of a complete collapse of the private market for small group plans, SHOP is going to have an uphill battle to gain market share in a very competitive market place. Its not that I dont want to see the SHOP program succeed, but the folks managing SHOP will have to show they have a demonstrably better portfolio of plans and customer service than they have exhibited to date.

[wpfilebase tag=file id=54 /]