Are two health plans being paid on behalf of Covered California consumers?

In recent weeks I’ve been contacted by several consumers who found out they had been enrolled in Medi-Cal while receiving, and still paying, for their subsidized private health insurance through Covered California. Aside from the obvious question of how could this happen, is the reality that Covered California may have been advancing tax credits to private health plans while the Department of Health Care Services was paying counties for Medi-Cal enrollment for the same household.

Mysterious System changes CoveredCa accounts

Earlier in 2014 it was a mystery who was tinkering with the accounts of Covered California consumers and deleting their income. (See: Mysterious System changes CoveredCa accounts). Families were receiving notices of their new Medi-Cal enrollment after they had successfully purchased a private health plan through Covered California. Investigation showed that a user by the name of System had disallowed some or all of the account holders stated income. The removal of income lowered the monthly household income below 138% of the federal poverty line making the individual or family eligible for Medi-Cal enrollment.

Medi-Cal was news to these families

Some families, completely unaware that their income had been changed, were surprised by the Medi-Cal eligibility and fought it. For these folks, this Medi-Cal eligibility had to be some sort of cruel bureaucratic snafu. After all, they continued to receive an invoice from their health plan at the subsidized rate and they continued to pay it. Within the initial Covered California enrollment if a household income wasn’t high enough to qualify for the tax credits they were only offered Medi-Cal.

Minimum essential coverage

Under the ACA, if an individual is eligible for minimum essential coverage from a government program like Medicare or Medi-Cal, they are ineligible for the Advance Premium Tax Credits to reduce their monthly health insurance premium. So once a household becomes eligible for Medi-Cal, at a minimum the tax credits should cease or the consumer should be dis-enrolled from the health plan. Some households had their health plans cancelled and others did not. No one mentioned they were offered the option to keep their private plans at full premium without the tax credits.

The government knows your income

The deletion or disallowing of income for a household seems to occur in two ways. The county or Covered California system operator learns that income stated such as a job, unemployment benefits or disability insurance has ended and they make the adjustment before the account holder does it. Income can also be removed if the consumer failed to provide verification for the income. In either event, the removal of the stated income is enough to drop the household into Medi-Cal. The county departments that administer Medi-Cal enrollment must be able to tap into other government databases to learn if household members really are receiving wages from a job. With this information they can delete income if their records show it is not current.

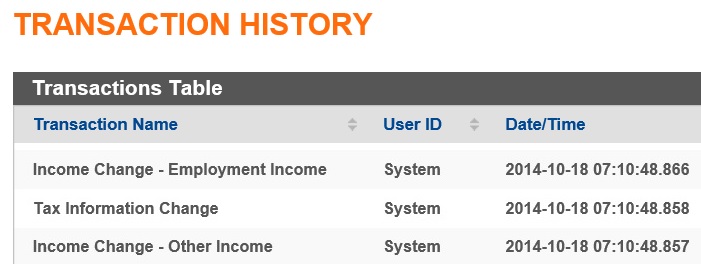

How do I know if the System changed my income?

Anytime anyone changes a field in a Covered California account it is logged. As an agent, if I make a change my user ID will be logged in the transaction file. If a Covered California employee makes a change the user will be Customer Service Representative. When a county worker makes a change I’ve been told from Covered California that the user name will by System. To review your transaction history and log: sign into your account, click on the Summary check box and look for Transaction History on the left hand side and click the link. You’ll get a screen that will give you this type of information.

User ID System indicates a county worker was adjusting your account according to Covered California.

Lack of clear communication

Some people learned they had been enrolled in Medi-Cal when their health plan had been terminated or when they receive a letter from their county asking them to select a managed health care HMO Medi-Cal plan. No one has mentioned they received any correspondence from Covered California that their income had been changed, their health plan terminated or their subsequent enrollment in Medi-Cal. The most interesting scenarios involve consumers who are enrolled in both Medi-Cal and their private plans. One county social services worker explained it this way in a comment left on the blog post Mysterious System Changes to Covered California Accounts –

As a County Medi-Cal worker the changes reflected in the Transition History are due to the Data Transfer required for the Counties to enter the applicant’s information into their SAWS System. Due to lack of training and understanding of how the systems talk, inadvertently a worker can erase or change entries. There are times our instructions are to close a case after linking the Covered CA case # to Our county # especially if the case is APTC only. By doing so, none of the data is entered into the case. Some cases then send a transaction to Covered CA and erase all the info such as income and tax filing status. Now why it does this happen only on some case and not others are still a mystery. As a county worker I take pride in my work however with the technical glitches that are out of my control and the lack of training and support we received make me wonder if I can continue enjoy my job as I have in the last 12 before. Please look at it from all angles before casting judgment.

While some health plans are properly terminated when the consumer is bumped down to Medi-Cal, others are not. Is it possible that Covered California continues to send the ACA tax credit to the carrier to keep the policy in force while the consumer is also enrolled in Medi-Cal?

A new meaning of dual-eligible

One gentleman I talked to was enrolled in Medi-Cal while he was still making his Kaiser premium payments. He assumed his county threw him into Medi-Cal after he lost his job and he applied for unemployment. He did not adjust his income through Covered California, the county or other agency did it for him. Once he got his unemployment benefits his household had enough income to become eligible for the tax credits again. For the period he was on Medi-Cal his Kaiser health plan was still in force. Kaiser would have only kept the policy going if they had been receiving the tax credits from Covered California to make up the full premium amount.

Who is authorized to adjust consumers account?

One issue that really frightens people is that unknown people are going into their private Covered California accounts and making changes without prior authorization or notice. More than likely, buried in the fine print of the Covered California agreement, there is undoubtedly a clause allowing certain government entities the access to a consumer’s account and to make changes without consent. Another commenter on the Mysterious System Changes to Covered California Accounts wrote –

This just confirms so many Obamcare fears about government controlled health care. That is so terrible that the county can just go in and do whatever they want. What if someone has a life threatening condition and they depend on the care of doctors that are in-network for the plan they enrolled in? I have had this happen to 3 members already. Because the kids were Medi-Cal, somehow Medi-Cal went in and changed the income to ZERO, kicking the parents off their Blue Shield PPO. In one case, for a member with a 1/1 effective date, Medi-Cal went in and not only changed the income to ZERO, but submitted a change to cancel the Blue Shield PPO retroactively to 1/1. This was done in June, which created a credit of 6 months worth of premiums for which Blue Shield now has no idea what to do with. So not only has the member been kicked off her plan by a mysterious county worker who was not given permission to make changes, the member had services paid for by Blue Shield during that time, which now may actually not have been covered. Can you imagine if someone was undergoing serious care for a chronic condition only to find out they can no longer receive care from their doctor? What a complete mess.

Another commenter left this message –

Finally! Explanations for the total nightmare I have encountered for 5 months. In my case they terminated my policy in the exchange and then reinstated it to the wrong policy (double the premiums; extremely high deductible and out of pocket costs). No changes have occurred in the originally approved enrollment. None! I’ve done everything to get changes made by ‘mystery’ to be corrected including currently in a three month hold for a State Appeal with no coverage for which I have already paid once. Does anyone know an e mail contact for a department at Covered CA with human beings that will actually read the documentation repeatedly sent. It would have to be high up as I’ve been everywhere else.

Where’s the audit?

I’m sure it’s a tiny fraction of the overall health plan enrollments, but it seems that some private plans have received tax credits and Medi-Cal managed care plans have received premium payments at the same time for the same consumer. So the question is, will any of this ever be reconciled or audited? Does Covered California have a clue if they are paying a tax credit to private plans when the account holders are enrolled in Medi-Cal. Does the Department of Health Care Services know if they are paying premiums to HMO plans when the members are enrolled in a subsidized private plan? And when will anyone finally realize they should alert the consumer when they terminate their health plan, change their income or just enroll them in Medi-Cal without their consent?