Some people will inflate their income to avoid Medi-Cal health plans.

While most people are thrilled with the ability to get affordable health insurance through Covered California, others are trying to avoid the premium free health insurance being offered. Specifically, some families and individuals are trying to figure out how to avoid having either their children or their family automatically enrolled in Medi-Cal. Inflating the income of the household is one way side step automatic enrollment in Medi-Cal health plans.

Covered California has made numerous changes to their income pages along with other application changes. To review the changes and download documents regarding the new and improved website visit 2016 income and application changes for Covered California enrollment.

- [wpfilebase tag=fileurl id=1049 linktext=’ Job Aid – Income Pages 2016′ /]

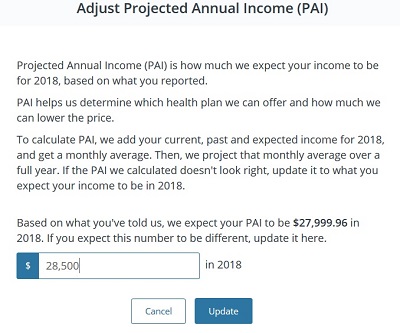

Adjusting Projected Income

If a household is automatically enrolled into a new health plan through Covered California, but the original household income is now in the Medi-Cal range, the household will be put on a carry-forward status for enrollment and their information sent to Medi-Cal. This means that the health plan will be active, but the county Medi-Cal office will review the case and if the income has not been adjusted out of the Medi-Cal range, the household may be determined Medi-Cal eligible.

Covered California includes an income adjustment tool to increase or decrease the projected income. The income adjustment tool (it can found at the bottom of the income section edit page) allows people to increase their income which decreases the amount of monthly tax credit subsidy they will receive. However, adjusting the income will not change the flag that the household income is within the Medi-Cal. The actual income entries must be changed in order for the system not to determine that household might be eligible for Medi-Cal.

Adjusting Projected Annual Income amount will not lift you out of Medi-Cal.

A good way to know if you have been put in the carry-forward because your income is too low is that NO monthly tax credits will be applied to the enrollments. The family will be billed the full premium amount for the health insurance, because their estimated income is too low and within the Medi-Cal, making them ineligible for the tax credits.

Inflating the income makes premium assistance available

Under the Affordable Care Act Medi-Cal eligibility for health insurance was expanded to included individuals and households earning between 133% and 138% of the federal poverty line. The way the Affordable Care Act is set up; if you, your family or children are eligible for Medi-Cal, those individuals are respectively ineligible for any premium assistance to lower monthly premiums for the marketplace plans. The household can purchase a Bronze, Silver, Gold or Platinum plan, but there will be no tax credits to lower the monthly premium.

DHCS MAGI Medi-Cal individual household size flow chart.

New -> DHCS MAGI Medi-Cal individual household size flow chart.

Some want to avoid Medi-Cal

It’s not that people I’ve talked to are not appreciative of the Medi-Cal services. However, usually through past experience they would rather not be on Medi-Cal again. Sometimes a family is seeing a doctor who doesn’t accept Medi-Cal and they don’t want to lose her. People also hear of extended wait times for office visits as fewer doctors in some regions are not accepting new Medi-Cal patients. For better or worse, perception is reality in the eyes of many people.

An incentive to work harder, make more money?

The way to avoid Medi-Cal is to make more money. And if you can’t make more, some people are considering inflating their income for 2014. Here is a hypothetical example.

Julie just turned 26 and can no longer be on her father’s health insurance plan. She has a few health challenges that have been under control with the help of a local physician. Julie loves this doctor but the doctor doesn’t accept Medi-Cal. Julie is living at home and has started a small pet sitting business. While she can see her business expanding, along with her profits, in 2014, she is only making about $15,000 annually in 2013.

Her current income is below $15,860 or 138% of the federal poverty line which makes her automatically eligible for Medi-Cal and ineligible for the premium assistance through Covered California. Julie is optimistic that her business will provide her with at least $16,000 in adjusted gross income in 2014.

Bronze plan is $0 premium for Julie

A 26 year old making $16,000 (based on 2014 rates) in zip code 95608, Carmichael, CA, would be eligible for $225 in a monthly premium assistance tax credit to be applied to any plan he or she chose. That would make the least expensive Bronze plan at $201 a month equal to zero with the tax credit. The least expensive Silver plan would be $44 after the tax credit is applied to the $268 monthly premium. Julie’s doctor accepts both of the plans.

Qualifying events and income adjustments

If at any time during the year a family’s household income exceeds the expanded Medi-Cal eligibility, that is a qualifying event and they can then apply for one of the Covered California plans and premium assistance. If the household income continues to increase and Covered California is not notified, the individual might be liable for tax credits they received based on the lower income. I have not found any documentation on either the Department of Health Care Services Medi-Cal or Covered California Medi-Cal websites that explains how an individual or family may be penalized or asked to return tax credits if they inflated their income to avoid Medi-Cal.

Is this an ethical dilemma?

What should Julie do?

Should she say goodbye to her doctor and accept Medi-Cal?

Should she accept Medi-Cal with her current income and then transition out when she can verify she is making more money?

Should she just be optimistic and inflate her income so she can continue to she her doctor and stay healthy?

If anyone has any clarity to the regulations, I would love to get them and post them here.

Julie can also enroll in a health plan off-exchange or through Covered California and decline being considered for premium assistance. In both scenarios, Julie will have to pay the full premium amount for her health insurance and not be able to claim the Premium Tax Credit on her taxes. But it may be worth it to her to keep the doctors she loves and trusts.

Families can also enroll their children who have been deem Medi-Cal eligible in off-exchange plans also. See Why are my Children on Medi-Cal?

See: IRS limits repayment of excess advance premium tax credits

IRS waiver of low income

Kaiser Health News is reporting, Consumers Whose Income Drops Below Poverty Get Break On Subsidy Payback, which indicates that the IRS won’t go after individuals and families that were deemed eligible for APTC but whose ultimate income is below the FPL. With in the article they cite §1.36B-2 Eligibility for premium tax credit from the IRS for this claim. While this may hold for states who did not expand Medicaid up to 138% of the FPL, I’m not sure if it is completely applicable for California who has expanded Medicaid up to 138% of the Federal Poverty Line. There is also the issue that within the Covered California agreement a household must report any changes to income within 30 days. My question has always been, if someone is approved for APTC at $20,000 at the beginning of the year, and then their annual income drops to $15,000 in the middle of the year (making the individual technically eligible for Medi-Cal) and this change of income is not report-

Will the individual owe the APTC for the period when the income dropped below 138% of the FPL?

Will they have to repay all the APTC for the entire?

The KHN provides a glimmer of hope that the IRS won’t come after people if their income dips below the FPL as stated on their 2014 federal tax return. But I really want to see it explicitly written in English by the IRS before I’ll believe it.

Covered California Countable Income

[wpfilebase tag=file id=1617 /]