As an insurance agent, I get an almost predictable sneer from people when I tell them that either they or their children are eligible for Medi-Cal based on their household income through Covered California. But in almost all situations, MAGI Medi-Cal, for the cost of $0 per month, is really good health insurance. MAGI Medi-Cal is equivalent to having a Platinum plan through Covered California.

Medi-Cal is California’s version of Medicaid, the federally subsidize health plan system for low income, aged, and disabled individuals. MAGI is the acronym for Modified Adjusted Gross Income. When the Affordable Care Act came online in 2014, California opted into the expanded Medicaid program offered under the Affordable Care Act.

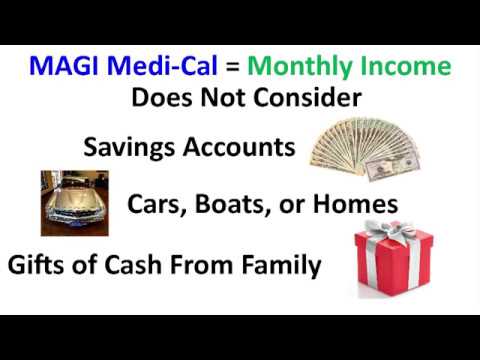

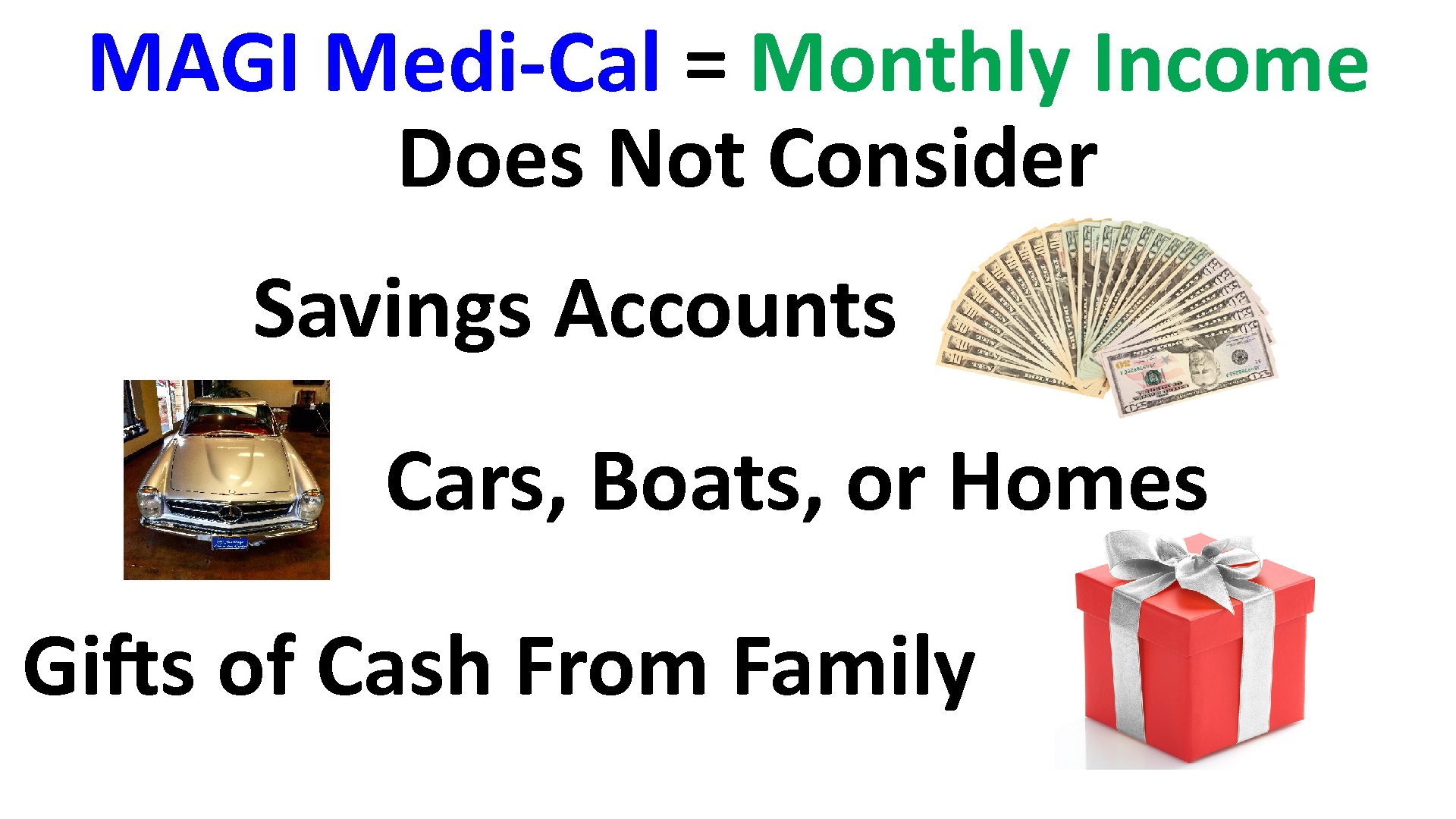

This means that an adult whose Modified Adjusted Gross Income is under 138 percent of the federal poverty level is automatically eligible for Medi-Cal. MAGI Medi-Cal, as it is known, only considers a person’s monthly income. They don’t consider your savings account, assets like cars, boats, or homes, and they don’t consider non-taxable gifts from your family.

The downside for some people is that if you are eligible for MAGI Medi-Cal, you are ineligible for the Premium Tax Credit subsidies offered through Covered California for a private health insurance plan. The animus towards Medi-Cal has its origins in factual, but anecdotal, stories of less than desirable health care provided by Medi-Cal. There is also the issue of having to deal with the bureaucracy of Medi-Cal at the county level.

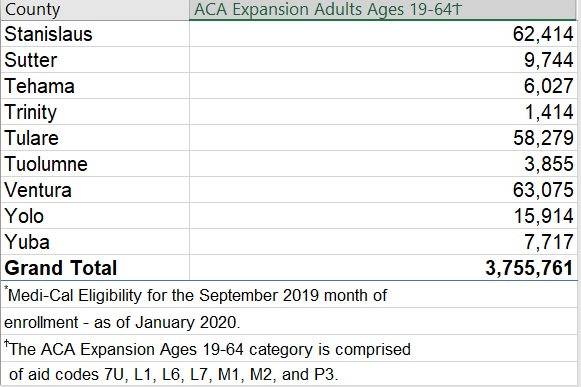

3 Million Adults Enrolled in MAGI Medi-Cal

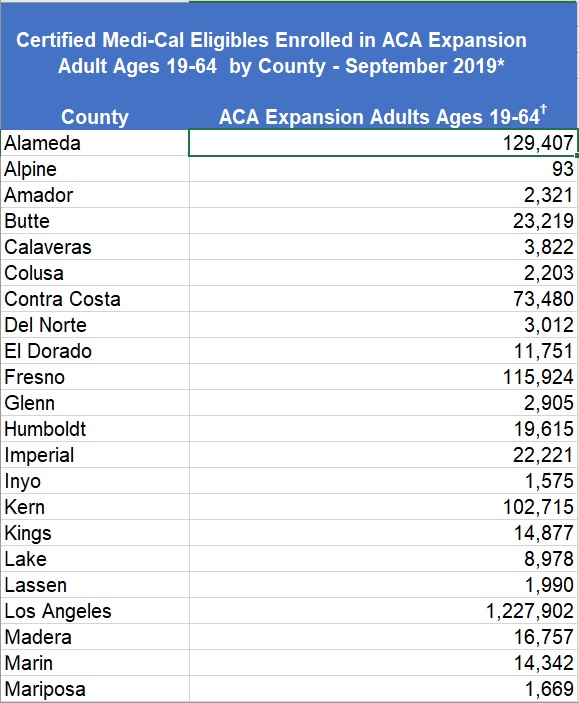

However, as of September 2019, there were 3.7 million adults between the ages of 19 and 64 enrolled in MAGI Medi-Cal. There were 4.8 million children, 18 years old and younger, enrolled in Medi-Cal, a large portion of which became eligible with the expansion of Medi-Cal under the Affordable Care Act.

For dependents, 18 years old and younger, they are eligible for MAGI Medi-Cal if the household income is below 266 percent of the federal poverty level. If the household income is over 139 percent of the federal poverty level, but under 266 percent of the federal poverty level, the dependents will be transitioned into Medi-Cal while the adults are eligible the premium tax credits offered through Covered California.

MAGI Medi-Cal is like a Private Plan

In California, MAGI Medi-Cal HMO managed care plans cover all the same benefits as individual and family plans sold through Covered California or directly from the health insurance companies off-exchange. With the Medi-Cal HMO plans there is no monthly premium and there is no cost for covered health care services, including prescription drugs.

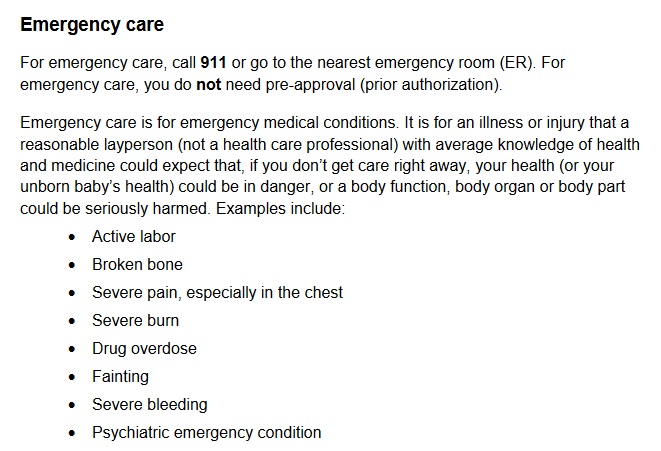

A real bonus with Medi-Cal is that you are covered for emergency services anywhere in the United States. If you receive care for a serious or life threatening emergency, the Medi-Cal plan will consider whatever hospital you are taken to as being in-network with the plan.

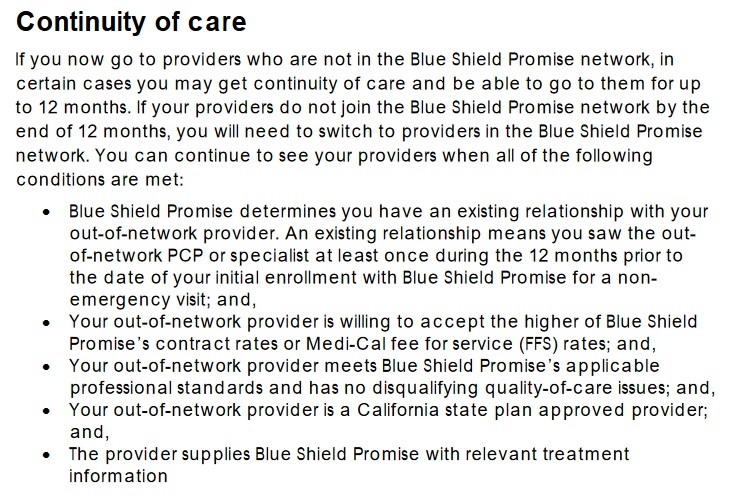

Another issue for people transitioning from private health insurance to Medi-Cal is continuity of care. If you are being treated for an illness, the Medi-Cal must accept those providers and their services under the continuity of care provisions.

Each California county handles their own Medi-Cal eligibility and enrollment. The Medi-Cal HMO plans may be county based, like L. A. Care, or you may have other options such Molina, Health Net, Kaiser, Anthem Blue Cross, or Blue Shield. Most children and adults who become eligible for MAGI Medi-Cal are given the option to enroll in one of the available plans in their county.

The Medi-Cal HMO plans are very similar to private health insurance plans. The plans have member ID cards, a provider network, and a drug formulary. One of the biggest complaints I hear is that the Medi-Cal HMO plans have few primary care providers and specialists that are accepting new patients. I also hear the same complaint from my clients in private health plans.

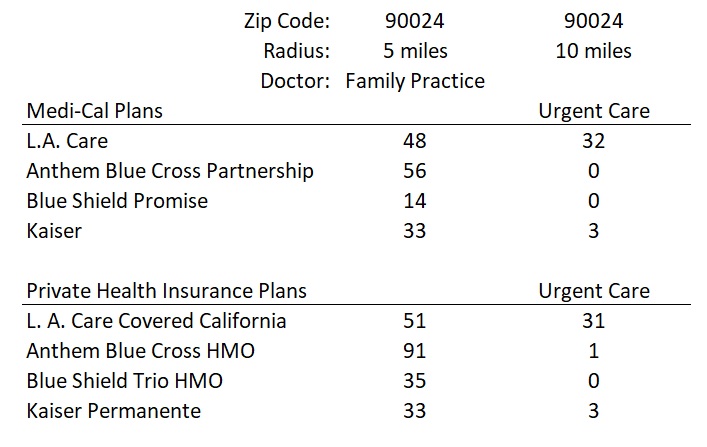

To see how Medi-Cal HMO plans compared to private HMO plans I did a random sampling of some providers in the 90024 zip code of Los Angeles. My first search was for primary care physicians in family practice within 5 miles of the zip code. I compared the Medi-Cal HMO plans to private HMO health plans offered in the same zip code.

As would be expected, the private health plans had more doctors, but not by much. L. A. Care was about even. Anthem Blue Cross plan showed 35 more doctors in their private plan and Blue Shield had 19 more. Blue Shield also had the least number of doctors of any of the Medi-Cal or private health plans.

Kaiser had the exact same number because Kaiser only has one network for all their different plans, regardless of if it is Medi-Cal, Medicare, or private insurance.

I also looked at Urgent Care providers within a 10-mile radius. Urgent Care is important because for people who rarely use health care services, it is usually the unexpected accident that drives them into the health care system. Unlike emergency care, where any hospital you are taken to will be considered in-network, receiving services from an out-of-network Urgent Care center will not be covered. L. A. Care had a similar number of Urgent Care centers in either the Medi-Cal or private plans. Kaiser, as expected, had the same number of Urgent Care centers. Both Anthem Blue Cross and Blue Shield struck out with virtually no Urgent Care centers in either the Medi-Cal or private health plans. The lack of in-network Urgent Care centers is a real problem for many of the health plans.

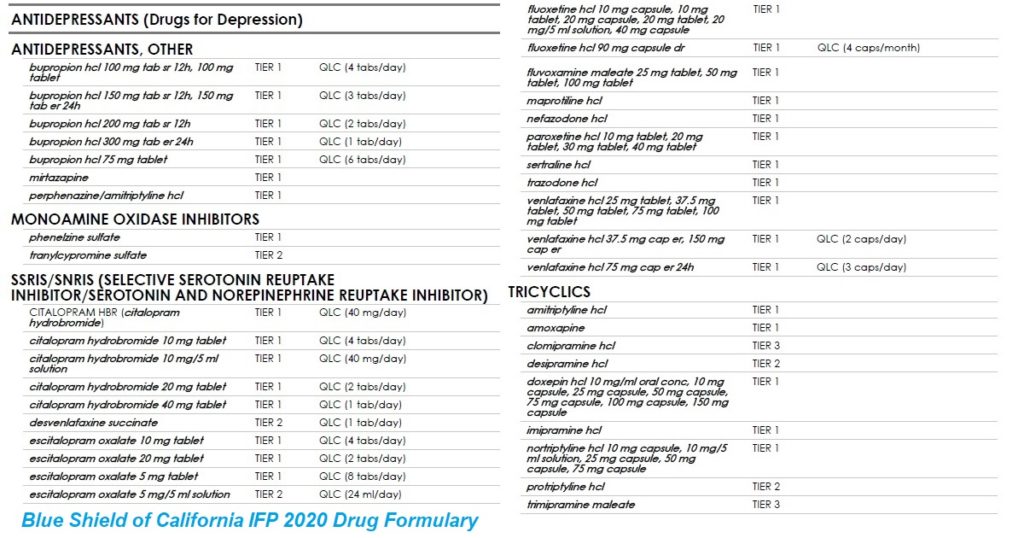

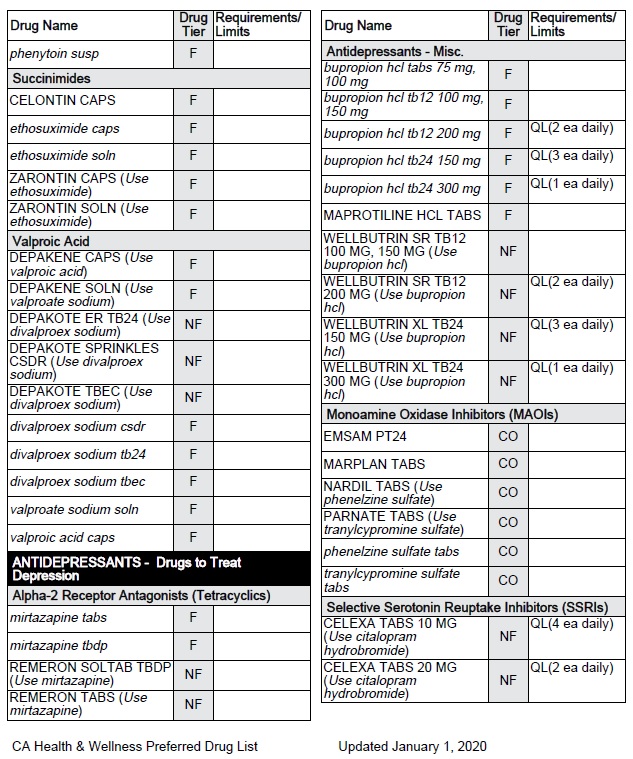

Another complaint about Medi-Cal HMO plans is that they have fewer prescription medications available. Certainly, many of the brand name drugs that have a generic equivalent will not be available in Medi-Cal plans. But this is also the case for private health insurance in many drug categories. Both Medi-Cal and private health plans directed members to use generic fluoxetine over the brand name of Prozac.

The cost of prescription medications is one of the primary drivers of rate increases for all health insurance plans. A quick comparison for anti-depressant drugs between the Blue Shield HMO individual and family private plan and the California Health Wellness Medi-Cal HMO plan shows more drugs available for Blue Shield members than the Medi-Cal plan.

Each Medi-Cal HMO plan may have a slightly different drug formulary, just like private insurance. In addition to doing a provider search for doctors, you can do a search for prescription medications for each of the MAGI Medi-Cal HMO plans.

Enrollment into a Medi-Cal HMO plan satisfies the new California individual mandate to have minimum essential coverage or be subject to a penalty. Medi-Cal is really good health insurance especially for people who are transitioning between jobs or trying to get a new business off the ground. Medi-Cal is not perfect, but neither is private insurance. But for the cost, Medi-Cal beats going without health insurance.