One of the most confusing pieces of insurance for Medicare beneficiaries is the Part D prescription drug plan. The benefit structure with deductibles, coverage gaps, catastrophic phase, and drug tiers is enough to give a rocket scientist a headache. To make matters worse, the plan sponsors play a shell game with drugs they cover and juggle them between the drug tiers within different plans.

Estimated reading time: 9 minutes

Confusion Is The Common Denominator of Medicare Part D Plans

Part D Medicare prescription drug coverage was perhaps the worst piece of insurance legislation ever created. It had to have been written by the insurance companies in order to confuse plan members. The result is that many people just pick the lowest cost Part D plan in their area and hope for the best. Medicare has added to the misery of seniors by allowing the insurance companies to shuffle their covered drugs between tiers which means there is no standard drug formulary that can be compared easily.

In California there are 32 different Part D plans offered by 11 different insurance companies. One plan sponsor offers six different plans. The only thing that differentiates these plans at first glance are the marketing names like Basic, Choice, Classic, Enhanced, Plus, Saver, Secure, and Value. These monikers are marketing gimmicks and tell the Medicare beneficiary nothing about the benefits of the plan.

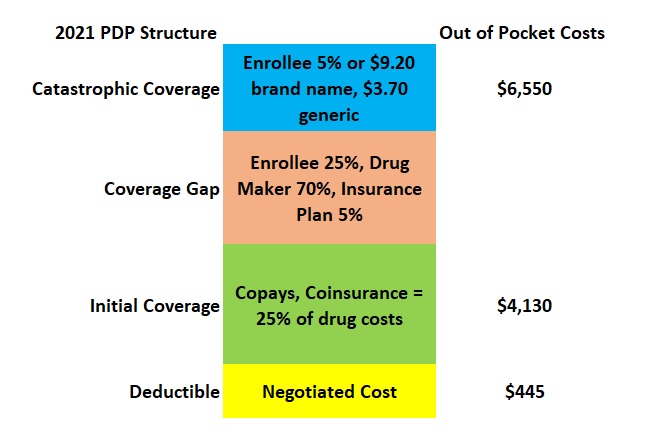

The Part D plans must follow a cost-sharing/benefit structure outlined in the original legislation and updated by Medicare every year. The Part D plans can have a

- A deductible amount

- Initial Coverage phase where the drug costs are lower and governed by either a set copayment or coinsurance.

- A Coverage Gap that is triggered after the plan member has spent $4,130 where the drug costs spike up to a set 25 percent cost share. After a complicated calculation based on the out-of-pocket costs of the plan member, drug maker discount, and insurance plan cost share equaling $6,550…

- Catastrophic phase commences where the drug costs drop down to 5 percent or set copays for brand name and generic drugs.

If this odd benefit structure is not confusing enough, Medicare allows the plan sponsors to add other layers of obfuscation on to the plans.

As long as the plan offered is within an actuarial range, the plan sponsors can significantly change the plan structure. Some plans may have a reduced deductible or no deductible at all. Other plans will have the copays of the Initial Coverage phase slide into the Coverage Gap.

The plan sponsors know that some people will select a “no deductible” plan, without knowing that they will pay more for their drugs with higher copays or coinsurance. Another marketing trick is extending the Initial Coverage copays into the Coverage Gap phase. This would appeal to people who are rightly concerned that their drug costs will jump in the gap. Of course, their prescription drug costs may never reach the coverage gap phase.

Because the cost-sharing benefit structure can be materially altered by the plan sponsors it is basically impossible to compare Part D plans based on the original Medicare structure.

The Shell Game of Drug Tiers

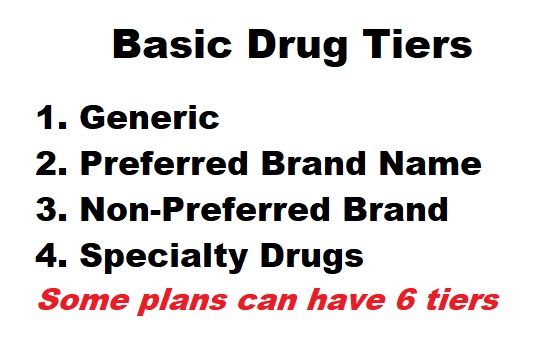

Drug tiers are another way plan sponsors confuse prospective members. All of the drugs covered are assigned to a drug tier to determine the cost in in the Initial Coverage phase. The basic drug tier levels are

- Generic

- Preferred Brand Name

- Non-Preferred Brand

- Specialty

Some plan can have 5 or 6 tiers to further segregate the drugs in discreet pricing columns. There will be plans where drug tiers are not subject to the deductible, but have a set copayment from the beginning of the plan.

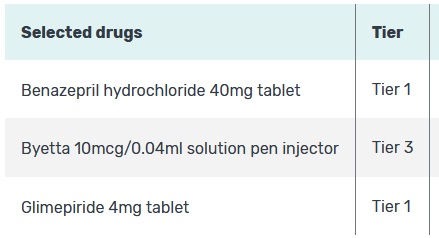

Unfortunately, the same drug may be in different tiers between different drug plans offered by the same company. This adds another wrinkle in determining the most cost-effective plan. This is further complicated if the drug in question is not used on a regular basis. The Medicare.gov drug plan program dictates that the drugs entered are used every month. This condition artificially inflates the overall cost of the drug plans with infrequently used drugs. Not all drugs are covered by all plans. The plans must have certain classes of drugs available, but your specific brand name drug may not be covered at all.

The Pharmacy Trap

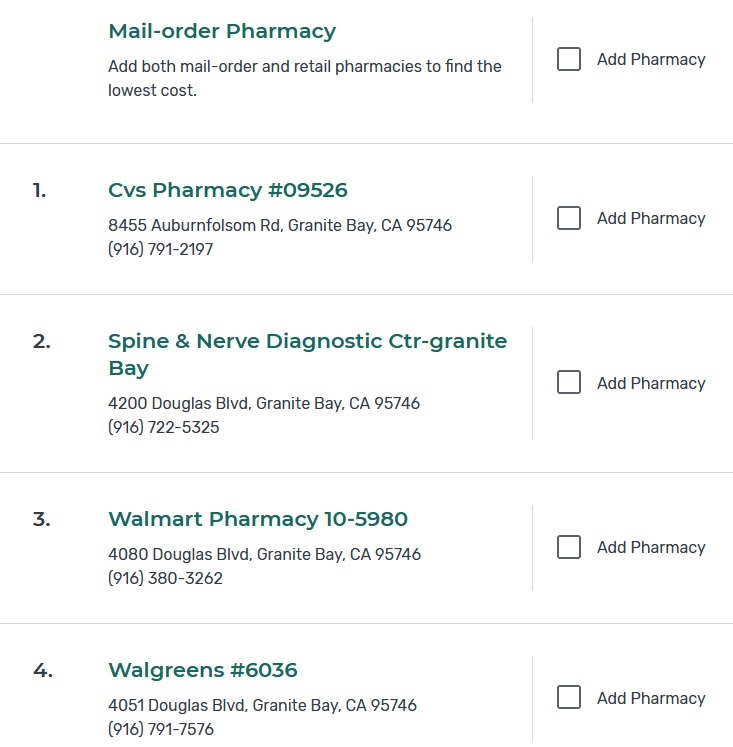

Finally, your pharmacy selection can make a big difference. If you enroll with a Part D and then pick up your prescriptions at a non-preferred or out-of-network pharmacy you will pay more. This another trick the plans and the Pharmacy Benefit Managers use to fleece consumers.

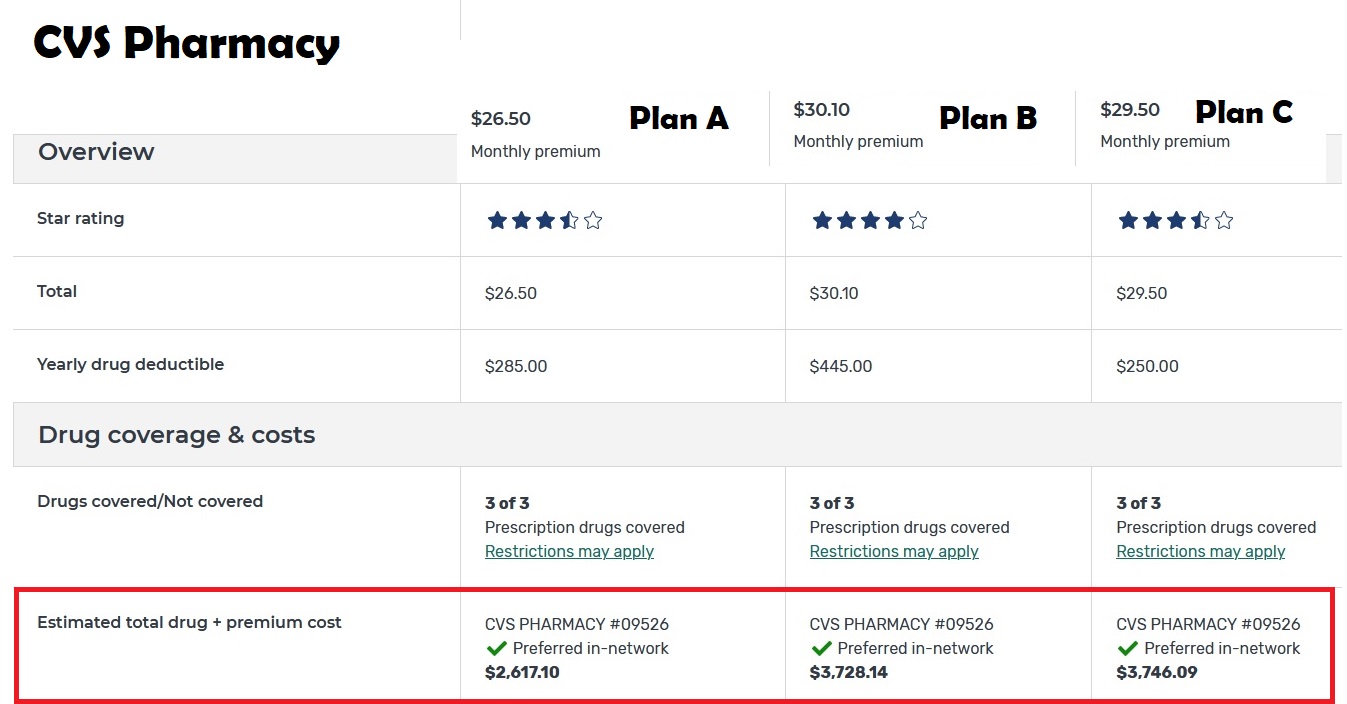

In this example, comparing the three lowest cost Part D plans with CVS as the preferred pharmacy. The lowest monthly premium plan actually has the lowest out-of-pocket costs. All plans have a deductible, but none of the are the same.

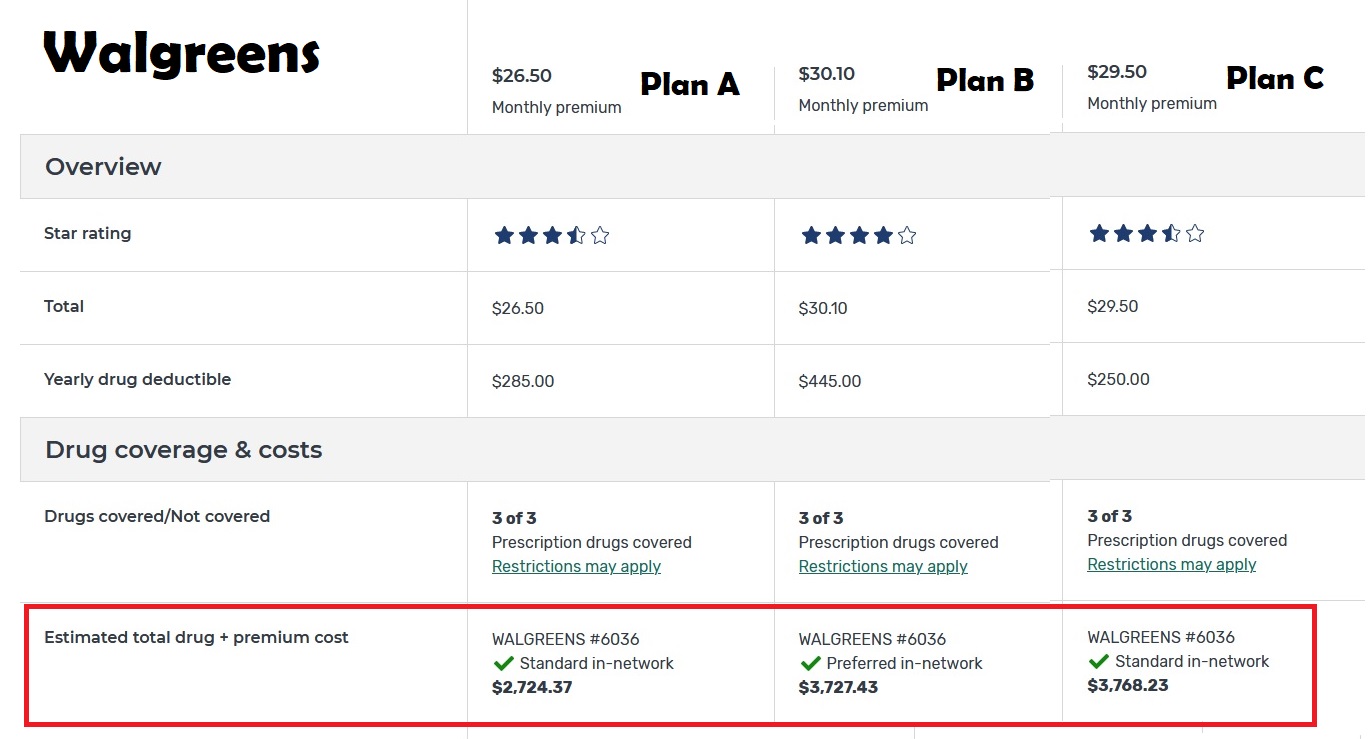

If we change the preferred pharmacy to Walgreens, Plan A is still the least expensive, but the overall drug costs go up by $107. This illustrates the role pharmacies play in determining the out-of-pocket costs for the plan beneficiary. This is wrong. It should not make difference where you get your retail prescriptions filled. All pharmacies should be preferred and in-network.

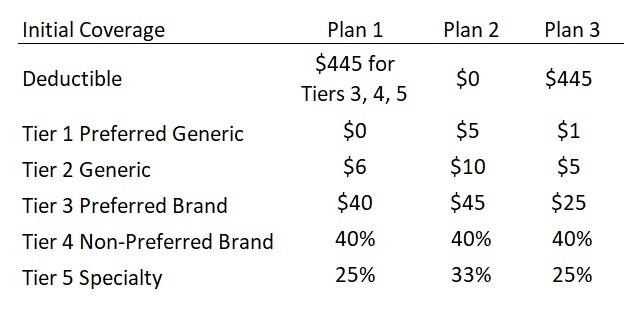

Part D Plans Are Not Standard Except for the Confusion

Here are three different drug plans. Plan 1 has a deductible, but only for Tier 3 drugs and higher. This means you go straight into the copay structure for Tier 1 and 2 on day one. Plan 2 has no deductible. Notice how generally the copays and coinsurance are higher for the no-deductible plan. Compare this to Plan 3 with a $445 deductible for all drugs. The copays and coinsurance are generally lower than Plan 2.

The Medicare.gov drug plan finder tool is the best program for determining your best Part D plans. It is not perfect and you will need to think about how you use your medications and make adjustments to the results. The Medicare.gov drug plan finder will rank the plans based on total cost of the premiums plus out-of-pocket costs.

To summarize, you can’t base your entire decision on the Part D’s monthly premium or deductible. You have to dig into the drugs you take, their respective tiers, and how often you use the drugs. There may be instances where a higher premium plan will actually save you money if your drug is in a tier not subject to the deductible. Regardless, it is all too confusing for normal human beings to figure out.

The whole Part D mess is exasperating because Medicare subsidies the Part D Plans. Yes, Medicare pays the insurance company to lower the monthly premiums of the enrolled member. If Medicare is subsidizing these plans, they can demand they adhere to a set benefit structure, drug tiers, and drug formulary so normal human beings can make an intelligent selection, not a decision based on marketing gimmicks.

The YouTube Version Of This Post