Selling assets can generate Capital gains that leads to enough income to receive ACA health insurance tax credits.

Numerous individuals with income below the ACA threshold to receive tax credits must weigh the consequences of selling assets in order to be eligible for the tax credits to purchase a private plan through a Marketplace exchange like Covered California. The prospect of selling retirement assets early in order to qualify for affordable health insurance other than Medicaid or Medi-Cal is forcing households to engage in early tax planning strategies before they reach the age of 65 and are eligible for Medicare.

Selling assets avoid Medicaid and Medi-Cal

An unfortunate flaw of the ACA is that determines eligibility for the tax credits to lower the monthly health insurance premium amount solely on income. Many people who have structured their lives to live on very little income, but may have a nice nest egg of assets, are only eligible for Medicaid. This is because their income falls below the federal poverty line established for Medicaid. For those individuals who would like assistance paying for a private plan they are faced with the prospect of selling assets to generate enough income to push them out of the Medicaid or Medi-Cal range.

ACA tax credits greater than tax liability

It is generally a disagreeable position when someone must sell assets early because the sale almost always generates a federal tax liability. In other words, the individual doesn’t get to keep all the proceeds from the sale of the assets, which could be real estate, stocks, bonds, mutual funds or even gold, because there are taxes on the profit from the original investment. However, in some cases, the tax credits received for ACA health insurance because the household income is higher might be larger than the tax liability incurred from selling assets.

The following is not tax or investment advice. You should always consult with your tax and financial advisors on the consequences of selling any assets.

Generating MAGI to reach ACA tax credits

For the purposes of determining the eligibility for the premium tax credits the ACA uses a Modified Adjusted Gross Income (MAGI) formula that includes normally non-taxed Social Security Benefits and tax-exempt interest. Generally, individuals are trying to add to their MAGI to push them into the tax credit range which is over 138% of the federal poverty line in California. Short of going back to work or getting a new job at a higher wage, people have sold assets that provide a capital gain that is reported on line 13 of the 1040 Income Tax Return. This capital gain or income is enough to keep them off the Medi-Cal rolls.

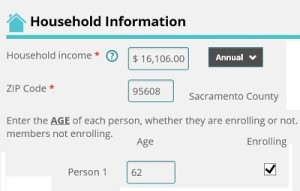

62 year old woman doesn’t want Medi-Cal

How might the selling of assets to raise the MAGI look like? For this example let’s assume Mary receives

- $10,000 from Social Security

- $2,000 from tax exempt interest

for a total Modified Adjusted Gross Income of $12,000. Mary is 62 years old, lives in Sacramento, is not married and has no dependents. Mary’s current income only qualifies her for Medi-Cal. In order to exceed 138% of the federal poverty line in California, under the 2014 FPL guidelines, Mary needs to have a MAGI that exceeds $16,106 annually. To be eligible for tax credits the Mary would need an additional $4,106 of taxable income. That additional income can come for the sale of assets or early distribution from a retirement account.

Selling assets is tricky

Just selling $4,106 in assets won’t always yield that same amount of income. This is where people need to talk with their financial advisor to determine the cost basis of their assets. Sometimes you may have to sell more than $4,106 in assets to generate the necessary capital gains income. In the worst case scenario outlined by the IRS, the tax on the capital gain of $4,106 would be 25% or $1,075.

Taxes, penalties and lost interest

But there are other taxes and penalties to consider when selling assets. There may be a penalty for underpayment of taxes from the IRS if there were no taxes withheld from the sale of the assets. There may be penalties for early withdrawal from an IRA and state taxes on the capital gain can actually be higher than the federal income tax. There are multiple points to consider before Mary rushes off and just sells some of her gold coins.

ACA tax credits can be substantial

Under the 2014 FPL guidelines, $16,106 MAGI will be eligible for tax credits in California and avoid Medi-Cal.

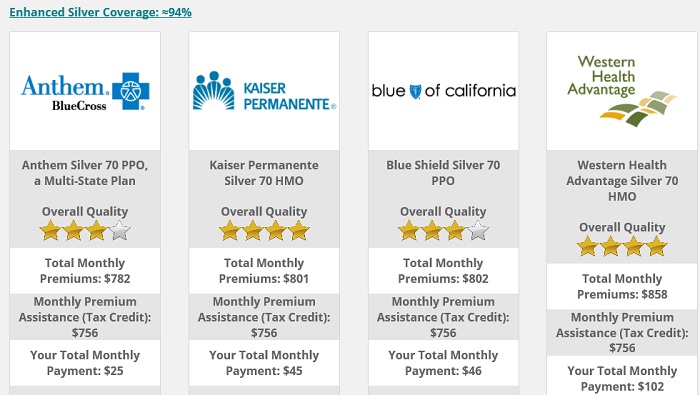

Let’s assume that Mary does sell enough assets to generate the required capital gain to make her MAGI $16,106, just over the Medi-Cal line. For her age and Sacramento residence the Covered California Shop and Compare Tool estimates she will be eligible for $756 in a monthly tax credit or $9,072 total annual tax credit. Further, let’s assume that Mary’s capital gain is completely wiped out by federal and state taxes, penalties, and the loss of future earnings from compound interest.

Tax credits can be more than capital gain taxes

If we subtract Mary’s total loss of $4,106 from her ACA tax credit of $9,072, we see that she has an overall gain of $4,966 for the year. In addition, Mary qualified for an Enhanced Silver 94 plan which has a lower deductible, copayments and coinsurance. The lower reduced cost sharing amounts can also add to Mary’s overall gain from her assets. Of course, only Mary can determine if selling those assets, incurring the taxes, and gaining the ACA tax credits was worth the hassle to have a private health plan over Medi-Cal which would cost her nothing per month.

A 62 year old person in Sacramento County with $16,106 MAGI is eligible for $756 per month in tax credits.

Always consult with a tax professional

For individuals with multiple health challenges that require a specialist not in the Medi-Cal system, there is no questioning that they wouldn’t sell assets just to become eligible for a subsidized private plan. But I can’t emphasize enough that careful consideration must be given to the consequences of selling personal assets just for the income. Always consult with your financial advisor and tax professional to get a clear picture on the taxes, penalties, and potential losses of selling assets for the ACA premium tax credits.