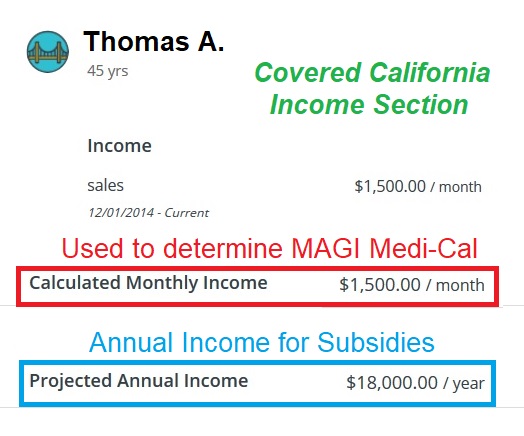

Modified Adjusted Gross Income or MAGI is California’s version of expanded Medi-Cal under the Affordable Care Act. Unlike other Medi-Cal programs, MAGI Medi-Cal does not consider your assets for eligibility for zero cost health insurance. MAGI Medi-Cal only looks at your monthly income that you enter in the Covered California application.

MAGI Medi-Cal Based on Monthly Income

Medi-Cal is California’s version of Medicaid. Medi-Cal is funded by both federal funds and State dollars. There are numerous health programs under the Medi-Cal umbrella. Many of these programs, and others administered by the Department of Health Care Services, consider both a household’s income and assets for determining eligibility. But this is not the case with MAGI Medi-Cal.

One of the confusing aspects of Medi-Cal eligibility is that you can apply for MAGI Medi-Cal through Covered California. It is confusing because Covered California posts an annual income chart that delineates whether a household’s annual income is MAGI Medi-Cal or eligible for the premium tax credit subsidies for private health insurance. Unfortunately, MAGI Medi-Cal focuses on your monthly income, not your annual income.

You may have made $30,000 in the first six months of the year, but if you have lost your job and have zero monthly income, when you apply through Covered California, you and your household members will be determined eligible for MAGI Medi-Cal. Another complicated feature of MAGI Medi-Cal, is that there are different income thresholds for dependents under 19 years of age, adults, and women who are pregnant.

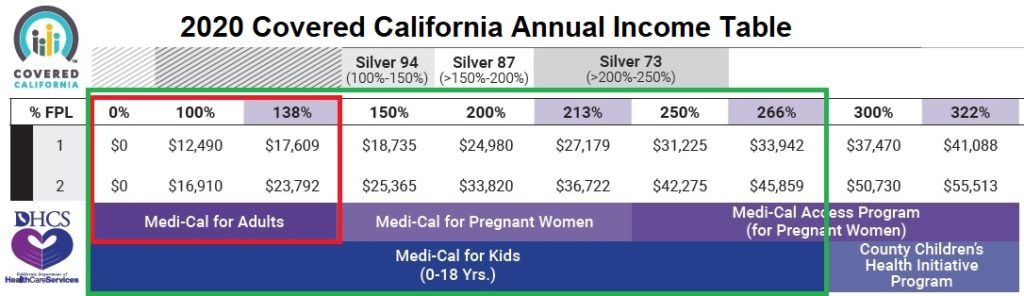

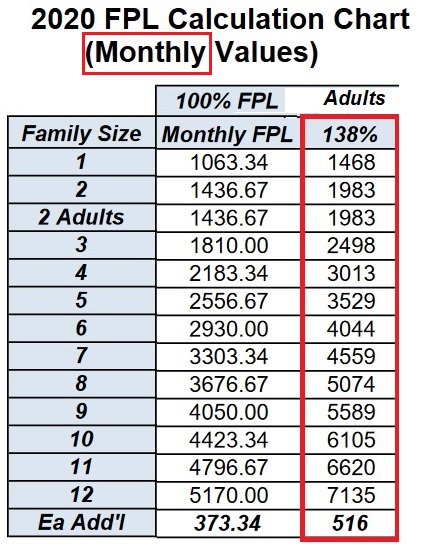

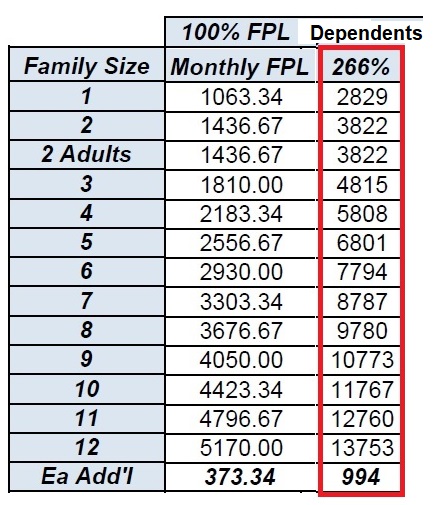

For adults, if the monthly income is under 138% of the federal poverty level for the household size, they are eligible for MAGI Medi-Cal. Dependents are eligible for MAGI Medi-Cal with household incomes up to 266% of the federal poverty level. This means if the household income is 200% of the federal poverty level, adults will be offered a subsidy through Covered California for private health insurance and the dependents under 19 years of age will be Medi-Cal. There are also two different programs for pregnant women; one at 213% of the FPL and Medi-Cal Access Program up to 322% FPL.

Covered California Income Section Determines Eligibility

Covered California doesn’t administer or enroll you into a MAGI Medi-Cal health plan. Through the Covered California income section where you enter you monthly income, the Covered California application system determines if you or your dependents are eligible for MAGI Medi-Cal. If your income indicates you are eligible for MAGI Medi-Cal in the Covered California system, that information is pushed over to the Department of Health Care Services and your county social services office.

Each California county is responsible for the final MAGI Medi-Cal eligibility determination and enrollment into a health plan. Once you or your dependents are determined to be eligible for MAGI Medi-Cal by Covered California, you must work with your county Medi-Cal office to make any changes to your account or data. The county Medi-Cal office can see everything you have entered in your Covered California account and can make changes to the account.

Whether you apply for Medi-Cal at your county social services office or through Covered California, you agree to report any changes to the household within 10 days. This means that if you move to another location, you have a new baby, or your income changes, it must be reported within 10 days. Even if the adults are receiving the health insurance subsidy through Covered California but your children are MAGI Medi-Cal, all changes must be reported to your county Medi-Cal office. If you make changes to your Covered California account, they will essentially be ignored.

MAGI Medi-Cal HMO plans based on county of residence

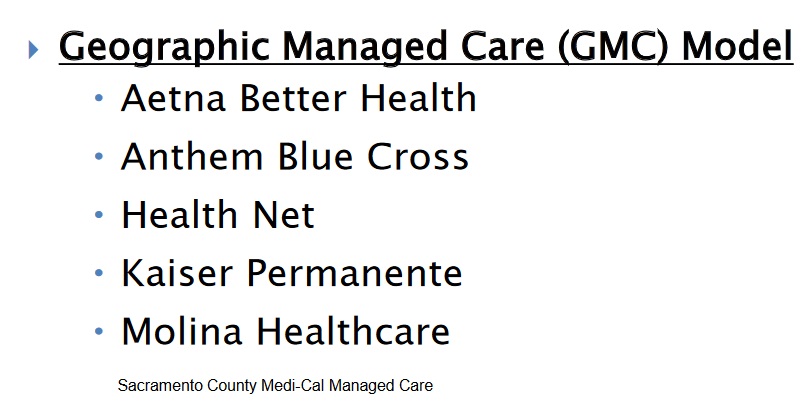

Not all counties offer the same Medi-Cal HMO plans. Some counties may only offer one health plan, while other counties such as Sacramento, Los Angeles, and San Diego may offer 3 or more different health plans. This is why it is important to tell your county Medi-Cal eligibility worker if you move. Moving to a new address in a new county may necessitate enrolling in a new health plan because your old health plan is no longer available.

The only difference between the plans is who administers it. Some counties may have their own plan, like L. A. Care, while other counties may use Anthem Blue Cross Partnership plan or some other privately run HMO. However, all the plans cover all the same benefits at generally $0 cost to the enrolled MAGI Medi-Cal enrolled member. What will be different is the network of providers. Some doctors and hospitals may be in one HMO plan, but not in a different plan run by a different company in the same county. Consequently, that is why it is important to check the network status of your providers on the HMO plan’s website.

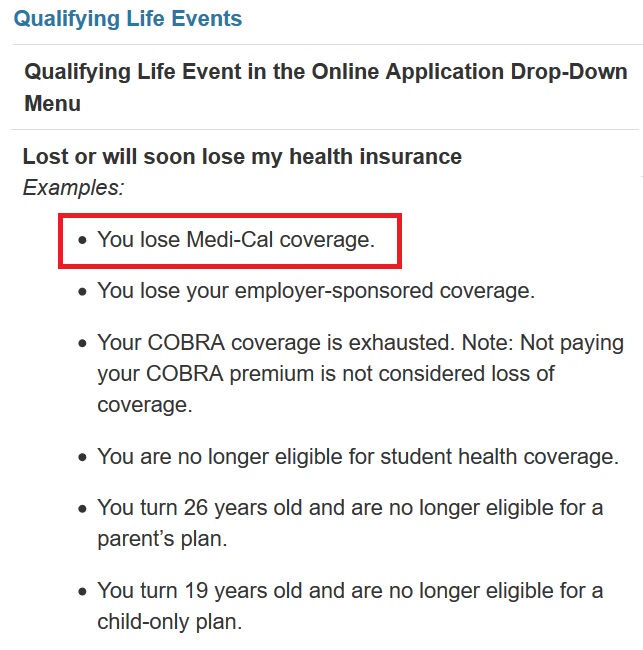

MAGI Medi-Cal Termination is Qualifying Life Event

If your monthly income increases above the threshold for MAGI Medi-Cal eligibility, the Medi-Cal plan will be terminated and you may be eligible for the subsidies through Covered California. The termination of your Medi-Cal health plan will not be retroactive and will not be immediate. Your county Medi-Cal office will give you plenty of notice of when your plan will terminate, usually the end of the next month after you report a change of income and they verify it with the documents you submit to them.

Loss of coverage is a qualifying event to enroll in a Covered California health plan with the subsidies. If your Medi-Cal terminates on August 31st, you have until that day to enroll in a Covered California plan to be effective September 1st. But don’t wait until the last minute. Covered California plans are not retroactive. If you apply for coverage through Covered California on September 1st, the plan will not start until October 1st. That means you could have a gap in coverage and there are no short-term medical plans in California.