It can be complicated to understand the different paths of acquiring health insurance in California. There are several different paths depending on your income, employment, age, and other factors such as if you are pregnant or disabled. Here are the main paths to health insurance.

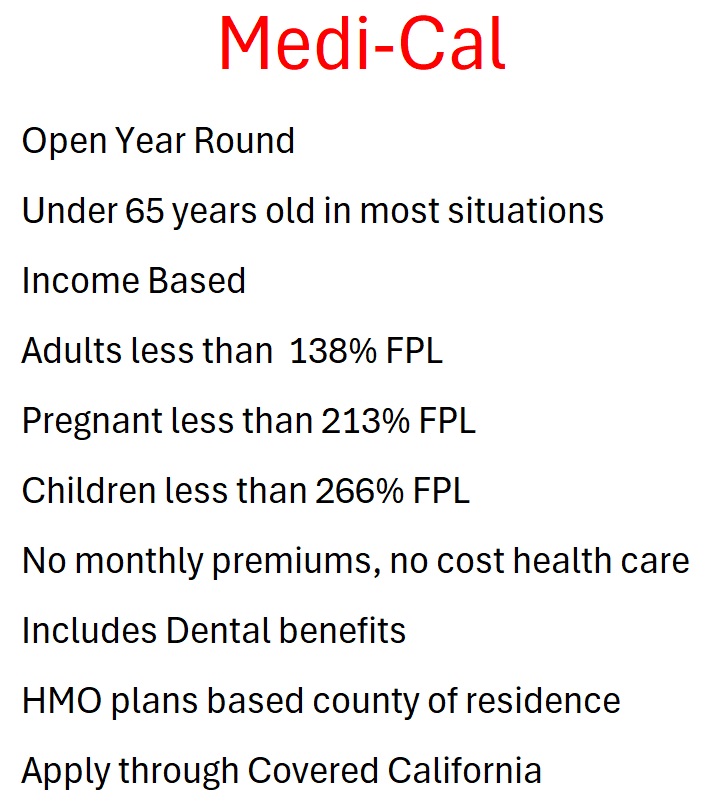

Medi-Cal

Modified Adjusted Gross Income (MAGI) Medi-Cal is available to adults whose household income is under 138 percent of the federal poverty level (FPL) and to children when the income is under 266 percent FPL. Eligibility is based on household income and if you have access to other health insurance such as employer group plans or Medicare.

Individuals who are pregnant can earn up to 213 percent FPL and qualify for Medi-Cal. Between 214 percent and 322 percent pregnant individuals can qualify for the Medi-Cal Access Program for Pregnant Individuals that helps covers the costs of pregnancy related health care services.

MAGI Medi-Cal has no monthly health insurance premium and no cost for health care services or prescription medications. The Medi-Cal plans are based on the county of your residence and are HMO plans. The health insurance covers all the same health care benefits within the HMO plan and a wide variety of drugs.

The easiest way to learn if you are eligible for MAGI Medi-Cal is to apply through Covered California. The Covered California application includes the necessary questions related to age and income of the household related to eligibility. If you and other household members are determined eligible for MAGI Medi-Cal, Covered California will forward the information to your county for final approval and enrollment.

Medi-Cal has no special enrollment period. You can apply for Medi-Cal at any time of the year. Dental and vision benefits are also part of the package for children and adults.

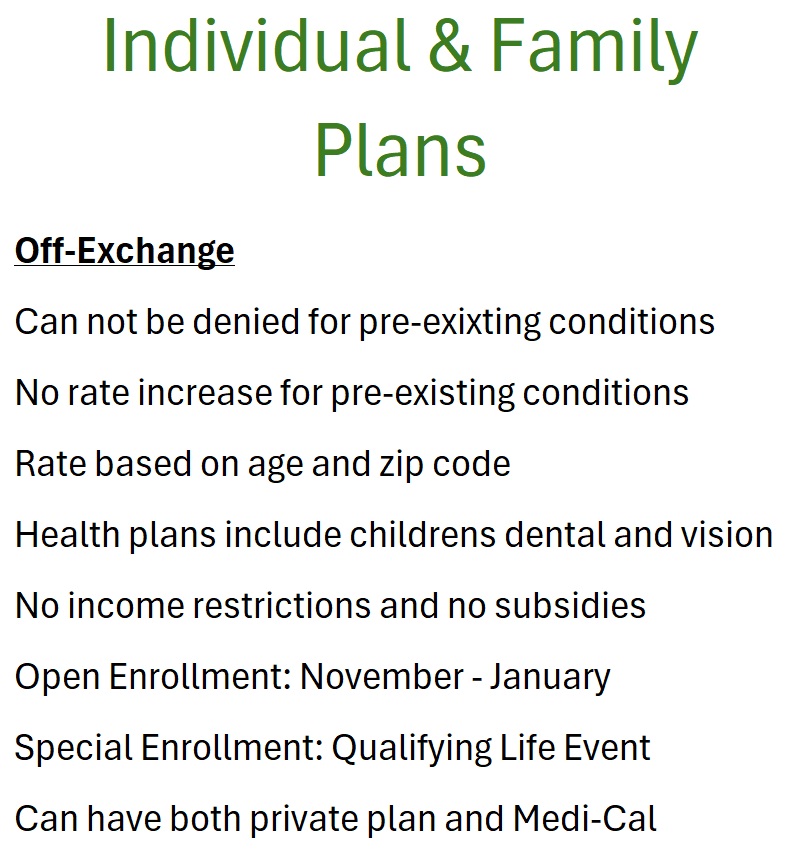

IFP or Individual and Family Plans

Off-Exchange

Health insurance is available from any carrier that offers plans where you live. When you purchase health insurance directly from the carrier, it is typically known as off-exchange. On-exchange is when you enroll through California’s marketplace exchange Covered California.

Outside of the open enrollment in the autumn, you need a qualifying life event for a special enrollment period to purchase an individual and family plan. Some of the qualifying life events that trigger a special enrollment period include losing health insurance or moving to California. You may need to supply documentation of the qualifying life event to enroll in an off-exchange during a special enrollment period.

The rates for the private individual and family plans are based on the person’s age and where they live. There is no rate increase for pre-existing conditions and you cannot be denied health insurance because of a pre-existing condition. Generally, individual and family plans are available to individuals under 65 years of age. Individuals over 65 years of age are normally eligible for Medicare.

An individual can be eligible for Medi-Cal and purchase a private individual and family plan. There are no subsidies to reduce the cost of the individual and family plan if you purchase it directly from the carrier off-exchange. All plans include dental and vision benefits for children 18 years old and younger. There are no adult dental or vision benefits in the health plans unless the service is determined to be medically necessary.

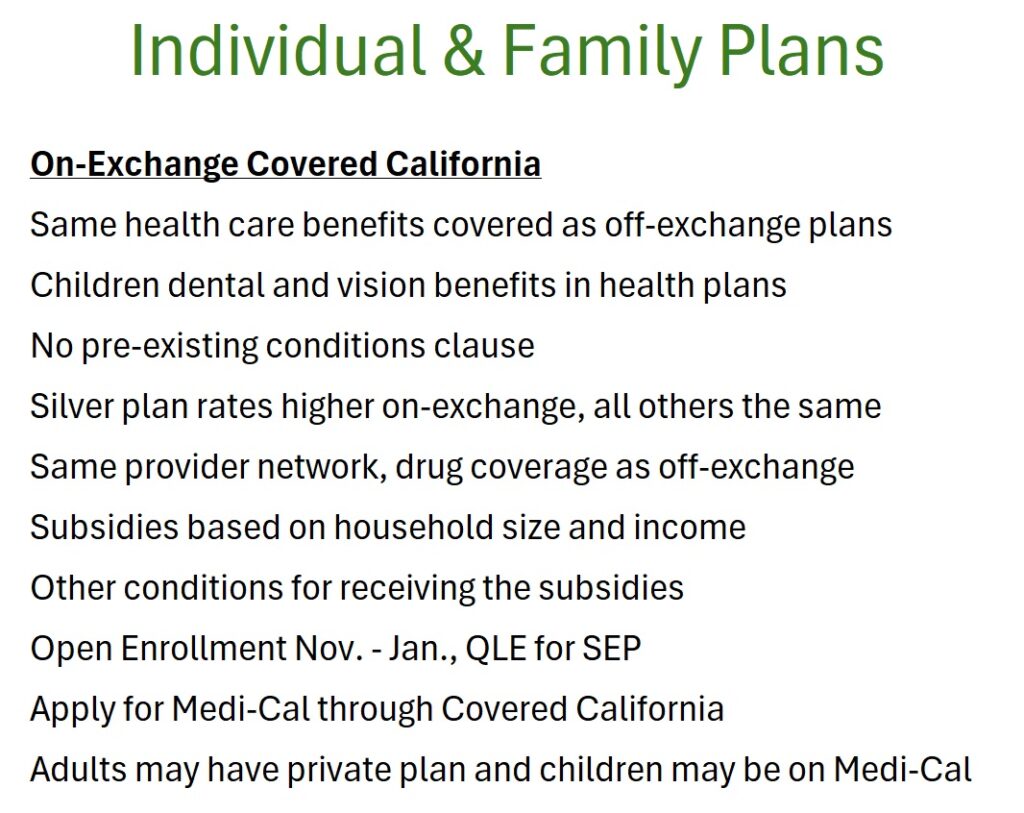

On-Exchange Covered California

Most of the plans offered off-exchange are also offered through Covered California. The rates are the same for the Bronze, Gold, and Platinum plans. The Silver plan rates offered through Covered California are 5 to 10 percent more expensive. However, the health care benefits are the same whether you enroll in a plan off-exchange or through Covered California. The provider network is also the same.

The only way to receive the Premium Tax Credit subsidies to reduce the cost of health insurance is to enroll through Covered California. Based on household size and income, you could be eligible for a subsidy that equals the monthly premium of the health insurance. There are other conditions that must be met in order to receive the health insurance subsidies such as agreeing to file a joint tax return if you are married.

Covered California also screens applicants for Medi-Cal eligibility. It is possible, based on the household income, that adults receive the subsidy and are allowed to select a private health plan while children are only offered Medi-Cal. Covered California applications for health insurance generally follow the same open enrollment and special enrollment period conditions as the off-exchange plans.

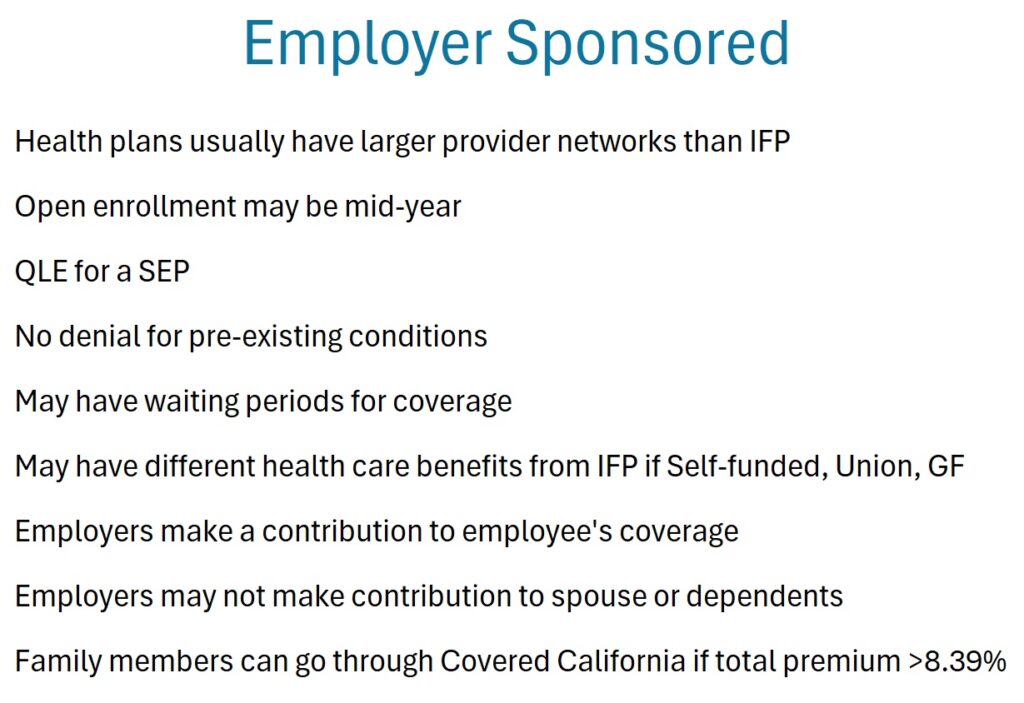

Employer Group Plans

Many employers offer their employees health insurance plans. The employer will contribute to the cost of the employee’s health insurance premium. An employee’s spouse and children usually are not offered any employer contribution to lower the cost of the health insurance. If the employer offers ’employee only’ insurance or the cost of the health insurance is more than 8.39 percent of the household income[1], for the entire family, then the spouse and dependents may apply through Covered California to be determined eligible for the health insurance subsidies.

If the employer plan is self-funded or a union plan, the health benefits may differ from either Medi-Cal or the individual and family plans. Most employer plans will have a larger network of providers than the individual and family plans. If you are offered an employer sponsored plan, you are generally ineligible for the subsidies offered through Covered California.

Enrollment periods can differ from the individual and family market. The open enrollment period may not coincide with the end of the year and begin in January. If you miss the open enrollment period for your employer group plan, you will need a qualifying life event to enroll in the middle of the year.

Not all employer plans cover children’s dental and vision benefits like the individual and family plan have. The employer plans will cover prescription medications.

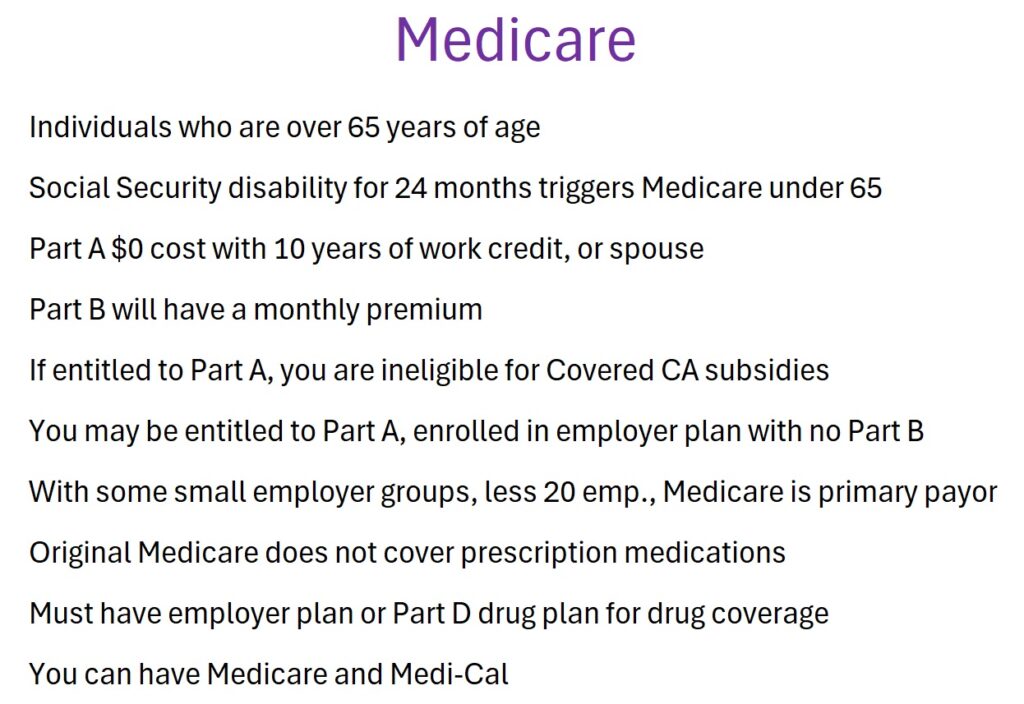

Medicare

Individuals who are 65 years of age are eligible for Original Medicare. You may also be awarded Medicare if you have been determined disable by Social Security for 24 months. If you have worked for 10 years and paid Medicare taxes, or if your spouse has the necessary work credits, then Part A of Original Medicare will be $0. There is a monthly premium for Part B outpatient services.

If you are eligible for Part A of Medicare, you are ineligible for the subsidies through Covered California. You do not have to enroll in Part B of Medicare if you have health insurance from a large employer group. However, for some small employer groups, Medicare is the primary payor of health care services, and you should enroll in both Parts A and B of Original Medicare.

Original Medicare does not cover prescription medications. You will need to enroll in a Part D prescription drug plan for coverage of drugs or enroll in a Medicare Advantage plan that includes coverage for drugs. If you accepted Part A of Medicare and opted out of Part B because you still have employer sponsored health insurance, the employer plan will normally include creditable drug coverage.

[1] Publication 974, Premium Tax Credit, 2023, Employer-Sponsored Plans, page 11.