Under H.R. 1, One Big Beautiful Bill Act, Congress expanded health plans eligible for Health Savings Accounts to include Bronze 60 and Catastrophic plans bought through the Marketplace Exchange. Traditionally, only High Deductible Health Plans qualified for tax-deductible contributions to a Health Savings Accounts.

When you are enrolled in a High Deductible Health Plan (HDHP), you can make contributions to a Health Savings Account. Those contributions, up to certain limits, can be deducted from your federal tax return to lower taxable income. The contributions in the Health Savings Account (HSA) are always under your control and grow tax free.

More Plans Eligible for Health Savings Account

Previously, only health plans that met the IRS definition of a HDHP could have the HSA contributions deducted from the federal tax return. With the passage of H.R. 1, it appears that Bronze 60 and Catastrophic health plans are now eligible for HSA contributions when purchased through the Marketplace Exchange like Covered California.

Initially, HDHP had no first dollar coverage for health care services. The plan member had to pay the full negotiated amount of the health care services or prescriptions until a deductible was met. With the Affordable Care Act, preventive office visits were covered 100 percent by the health plan.

With the onset of the Covid-19 pandemic, HDHP were allowed to cover telehealth visits at low or no cost to the plan member. The coverage of telehealth visits was extended by H.R. 1 for HDHPs.

The assumption of HDHP is that you pay for your health care services directly from the HSA. Additionally, you would have accrued a significant amount of money in the HSA so that if a catastrophic event occurred, you had the money available to cover the deductible and maximum out-of-pocket amount. A benefit of the HSA is that you can also pay for other health care services such as dental and vision services directly from the account.

For the purposes of defining the parameters of a HDHP, the IRS released updated plan design and HSA contributions for 2026.

- For self-only coverage, the HDHP deductible could not be less than $1,700 or $3,400 for a family. Once the deductible is met, the plan member goes into a coinsurance percentage until the maximum out-of-pocket amount is met.

- The maximum out-of-pocket amount HDHP cannot exceed $8,500 for an individual or $17,000 for a family.

- For 2026, individuals can contribute a maximum of $4,400 to an HSA or $8,750 for a family. The contribution amount is prorated based on the number of months you are enrolled in the HDHP.

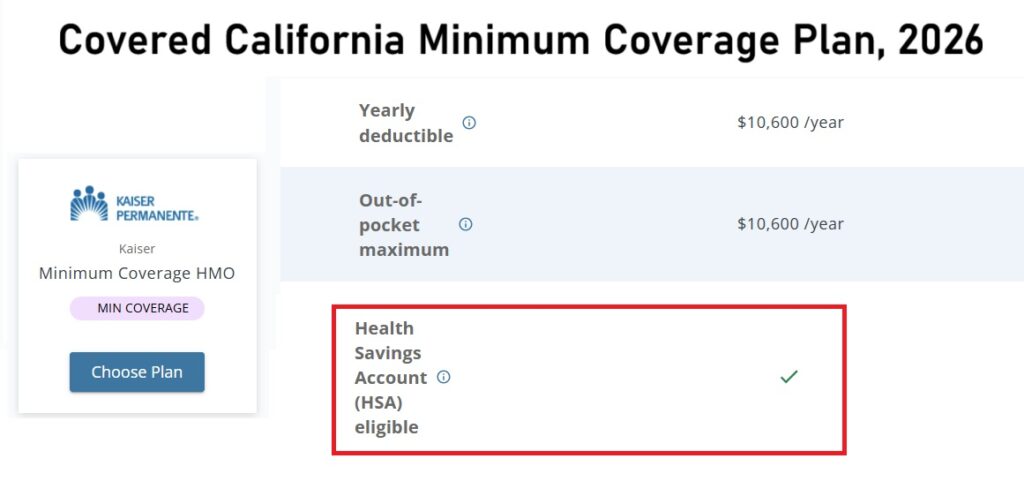

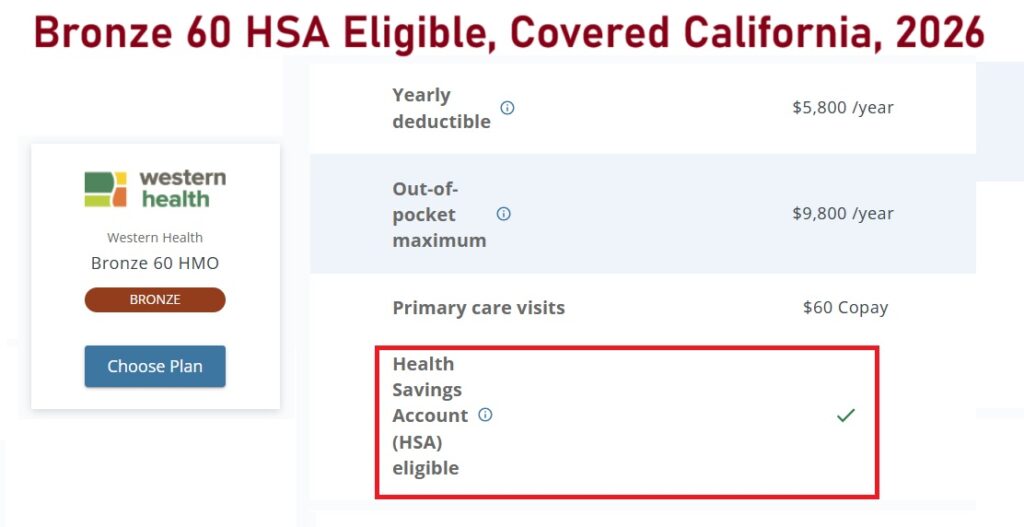

Bronze and Minimum Coverage Plan Now HDHP

In California, neither the Minimum Coverage (catastrophic) nor Bronze 60 health plans met the definition of a HDHP until Congress passed H.R. 1. Both plan designs cover first dollar health care expenses before a deductible is met. In addition, the maximum out-of-pocket amount for both plans exceeds the HDHP limits.

The economic theory behind HDHPs is that if the plan member must pay the full rate of the health care services before the health plan cost-sharing is triggered, the plan member will shop for the lowest price of the service or prescription medication. This comparison shopping, as the theory is professed, will drive down health care costs based on competition.

The reality is that people do not shop for a variety of reasons. First, most people just accept the referral of their primary care doctor to the specialist or facility to perform the health care service. Second, it is nearly impossible to shop for health care services because prices are not readily available to the consumer. Finally, individuals and families in HMO plan can’t go out-of-network and have the costs accrue toward meeting any deductible of maximum out-of-pocket amount.

Regardless of the contradictions between the IRS definition and congressional action, it appears that individuals in Bronze 60 and Minimum Coverage plans can open a Health Savings Account, make contributions, and deduct the contributions on their federal income tax return.

Unfortunately, the IRS has not issued any guidance for the 2026 tax year with respect to expanded definition of health plans eligible for a Health Savings Account. The language clearly states that the health plan must be purchased through a Marketplace Exchange like Covered California. That would seem to preclude Bronze 60 and Minimum Coverage plans bought off-exchange, direct from the insurance company, as being eligible for the HSA contribution deduction.

Perhaps the IRS will issue guidance before the end of 2025 so individuals and families can appropriately decide if they want that Bronze 60 plan and open a Health Savings Account.

YouTube video on expanded high deductible health plans.