As sole proprietor of a small business, I’m always looking for ways to reduce my taxes. For self-employed individuals like me, we reduce our self-employment taxes by reducing our income with expenses and deductions. However, an aggressive approach to reducing net taxable income translates into reducing future Social Security income. Sometimes, the loss of future Social Security income is greater than the self-employment taxes saved.

For self-employed individuals who must file federal Schedule C, Profit or Loss From Business, their net revenue of the business (gross revenue minus expenses) is recorded by the Social Security Administration. The net taxable amount, in most cases, becomes part of the historical earnings record for the individual.

Reducing Tax Income Reduces Social Security Income

The Schedule C dollar amount is transferred to Schedule SE, Self-Employment Tax. The net taxable amount is subject to up to 15.3 percent tax for Social Security (12.4%) and Medicare (2.9%) programs. Even though we get to deduct half of the SE tax on the federal income tax return, it can sting when we must write a quarterly estimated tax payment of 15.3% + during the year.

Consequently, finding legitimate expenses and other ways to reduce taxable income can save thousands of dollars. Unfortunately, after years of aggressively lowering their net taxable income, and thereby their historical Social Security earnings, some people learn their monthly Social Security will be very low.

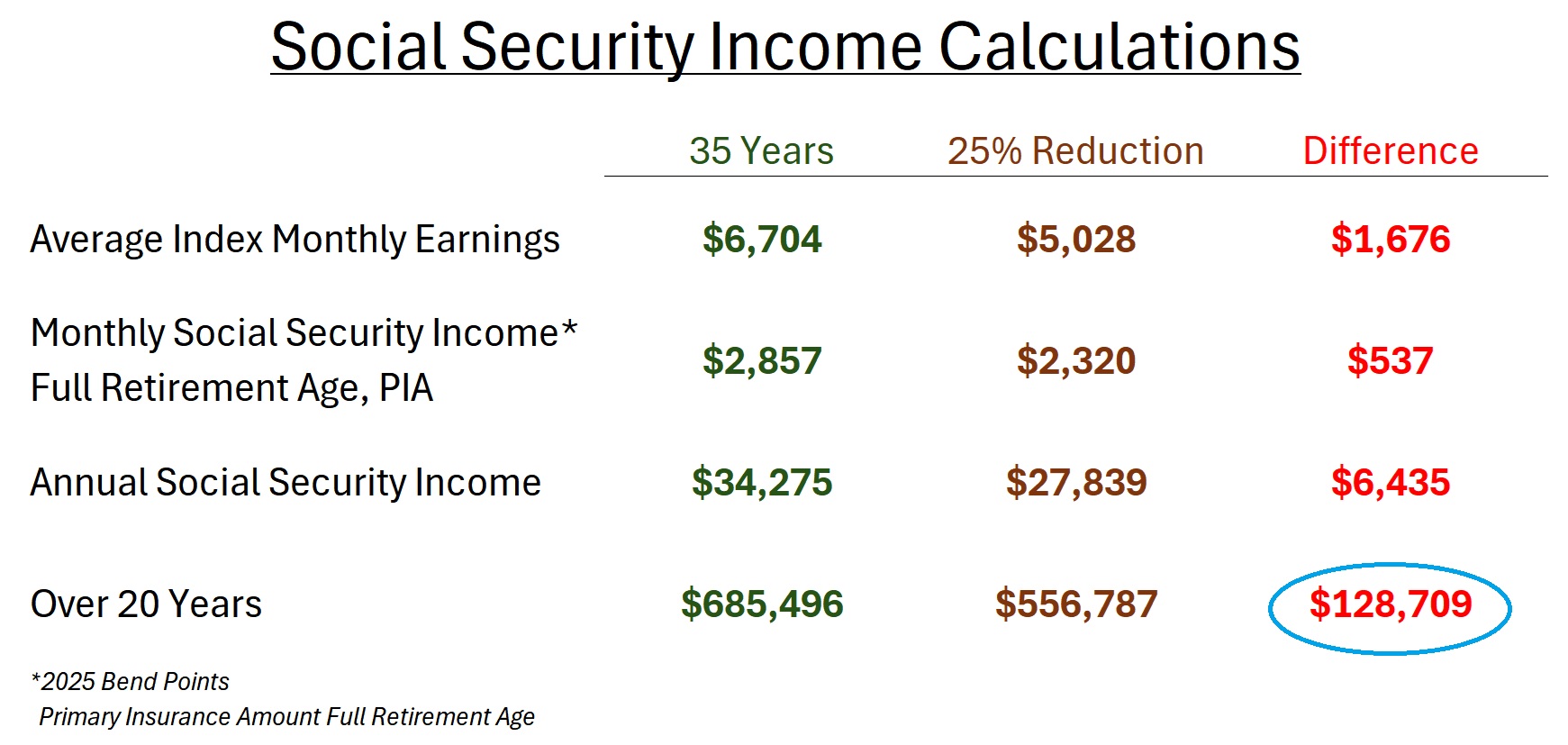

But how low will the Social Security income be with persistently low taxable earnings? Below I outline a scenario where an individual can lower their taxable earnings by 25 percent. Because the Social Security Administration uses the individual’s 35 years of index earnings to calculate the monthly Social Security income, this example has the individual’s income derived from their self-employment.

Over 35 years of business, this individual reported $1,679,217 of taxable income. They paid Self-employment taxes of 15.3 percent on each year of their earnings for a total of $295,920.

Reducing Income Reduces Self-Employment Taxes

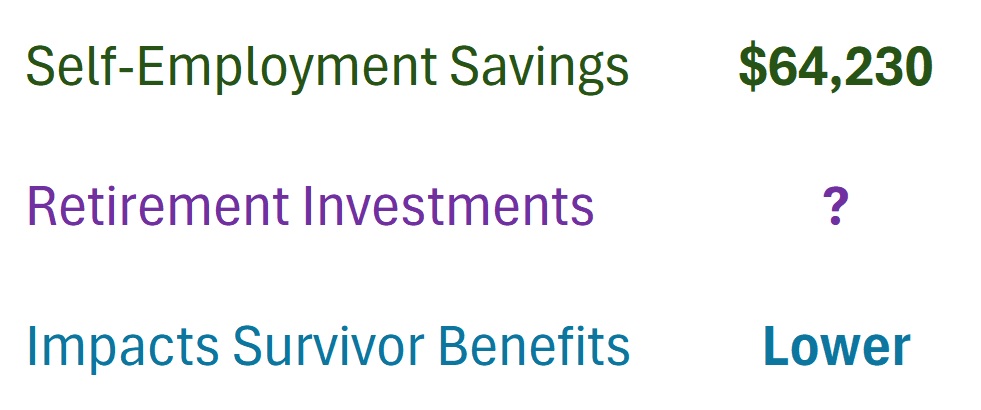

Let’s assume that this individual was able to reduce their reported taxable income by 25 percent. Total income over 35 years is reduced to $1,259,413. The Self-employment taxes are $192,690. The reduction of the taxable self-employment income over 35 years equals $64,230, not adjusted for inflation.

To calculate an individual’s monthly Social Security deposit (see how the PIA is calculated), the Social Security Administration takes the highest 35 years of income, adjusts the early years upward with an index, totals the indexed annual amounts and divides the number by 420. The result is known as the Average Indexed Monthly Earnings (AIME) for the individual.

The Average Indexed Monthly Earnings is reduced by $1,676 for the historical earnings that had been reduced by 25 percent.

The Social Security Administration then takes the AIME and applies a series of calculations to determine the Primary Insurance Amount (PIA) or monthly Social Security income deposit at full retirement age. (Example assumes the individual turns 62 in 2025 with corresponding bend points.)

With the reduced income, the Primary Insurance Amount is reduced to $2,320. The individual will have a monthly deposit at full retirement age that is $537 less per month with the lower income.

Reduced Income Costs More Than Saved SE Taxes

When the lower Social Security income is considered on an annual basis, the individual receives $6,435 less because of the lower reported income.

If we assume the individual collects Social Security for 20 years, they will receive $128,709 less with the lower income. The individual saved $64,230 on self-employment taxes with the lower income of 25 percent. However, in this scenario, the reduced income costs the individual over $60,000 in Social Security benefits if they retire at their full retirement age.

It is entirely possible that the individual’s income was reduced, in part, by funding a Simplified Employee Pension Individual Retirement Account (SEP IRA). The SEP IRA distributions could be equal to, or greater, than the difference between the full income and the income reduced by 25 percent.

The lower Primary Insurance Amount can impact survivors. A spouse and dependents who survive the death of the Social Security beneficiary will receive a lower monthly benefit based on the lower earnings.

There is nothing wrong with a sole proprietor employing an aggressive strategy for reducing their taxable income as reported on Schedule C. We just must be cognizant that lower reported taxable earnings will translate into lower Social Security deposits when we retire and for our spouses and dependents if we die early.

YouTube video reviewing a reduced self-employment income.