Social Security optimization considers the entire household situation including dependent children, spouse, and income of the family. There are times when filing for Social Security retirement benefits before your full retirement age can help the entire family, even if claiming Social Security income early reduces your monthly Social Security benefit for life.

Each individual and every family are unique. Everyone’s financial situation is different from income to assets. Consequently, a Social Security filing strategy that works for one household may not be best for a seemingly similar household.

Social Security Roadmap Shows Maximum Income Options

To maximize Social Security income most people will wait until age 70 before filing for Social Security. At age 70 most people will realize a monthly Social Security income that is 124 percent larger than their primary insurance amount at their full retirement age. However, for some individuals and families, claiming Social Security benefits can actually provide a greater income for the family.

Social Security has over 2,700 rules governing claiming option and the benefit amounts. In addition, Social Security cannot give advice about specific strategies about when to file. The Social Security website has no analytical tools to determine how other family members would be helped or hurt by your or their claiming options.

Fortunately, to navigate optimizing your Social Security benefit, there is an application from the National Association of Registered Social Security Analysts Ltd. that considers all the filing options. The application generates a report called a RSSA Roadmap.

The Roadmap report is a fairly dense and comprehensive report that explores various options of when to file for Social Security retirement income. The report is built on your earnings history and that of your spouse if applicable. Then, various filing or claiming options are considered and presented.

Age Based Filing Options Illustrated

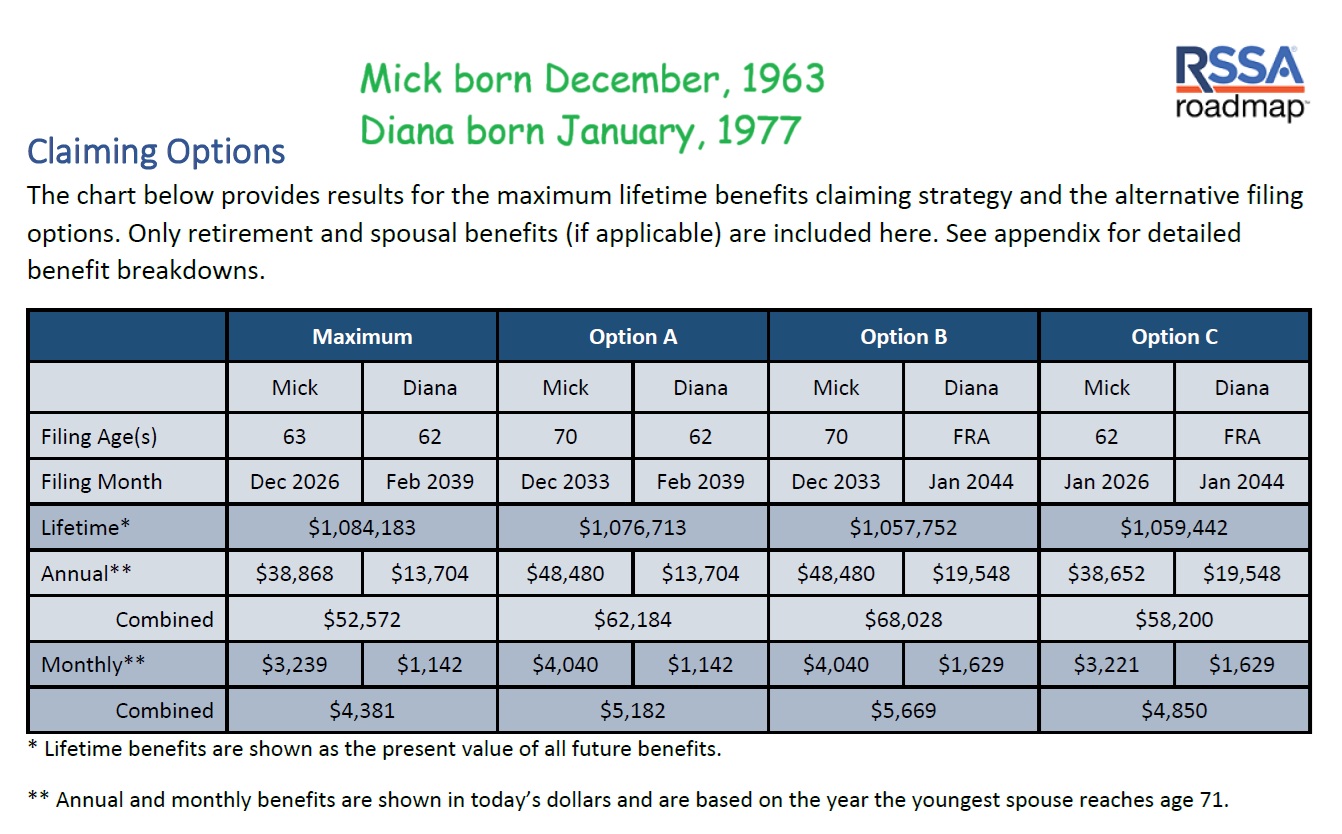

The Roadmap report generates the Maximum Social Security income scenario. We can also enter other age-based claiming scenarios that are detailed within the report. In the sample below, Mick was born in 1963, and his spouse Diana was born in 1977. Because Mick and Diana have children, the analysis concluded that Mick and Diana would receive the largest lifetime Social Security income benefit if Mick filed at age 63 and Diana claims Social Security when she turns 62 in 2039.

Options A, B, and C illustrate the lifetime, annual, and monthly income if Mick delayed filing until he was age 70 and if Diana waited to claim Social Security until she reached her Full Retirement Age (FRA). When structuring the report, both Mick and Diana estimate their longevity. The estimated year of their deaths is used to determine the dollar amounts and illustrated in today’s dollars.

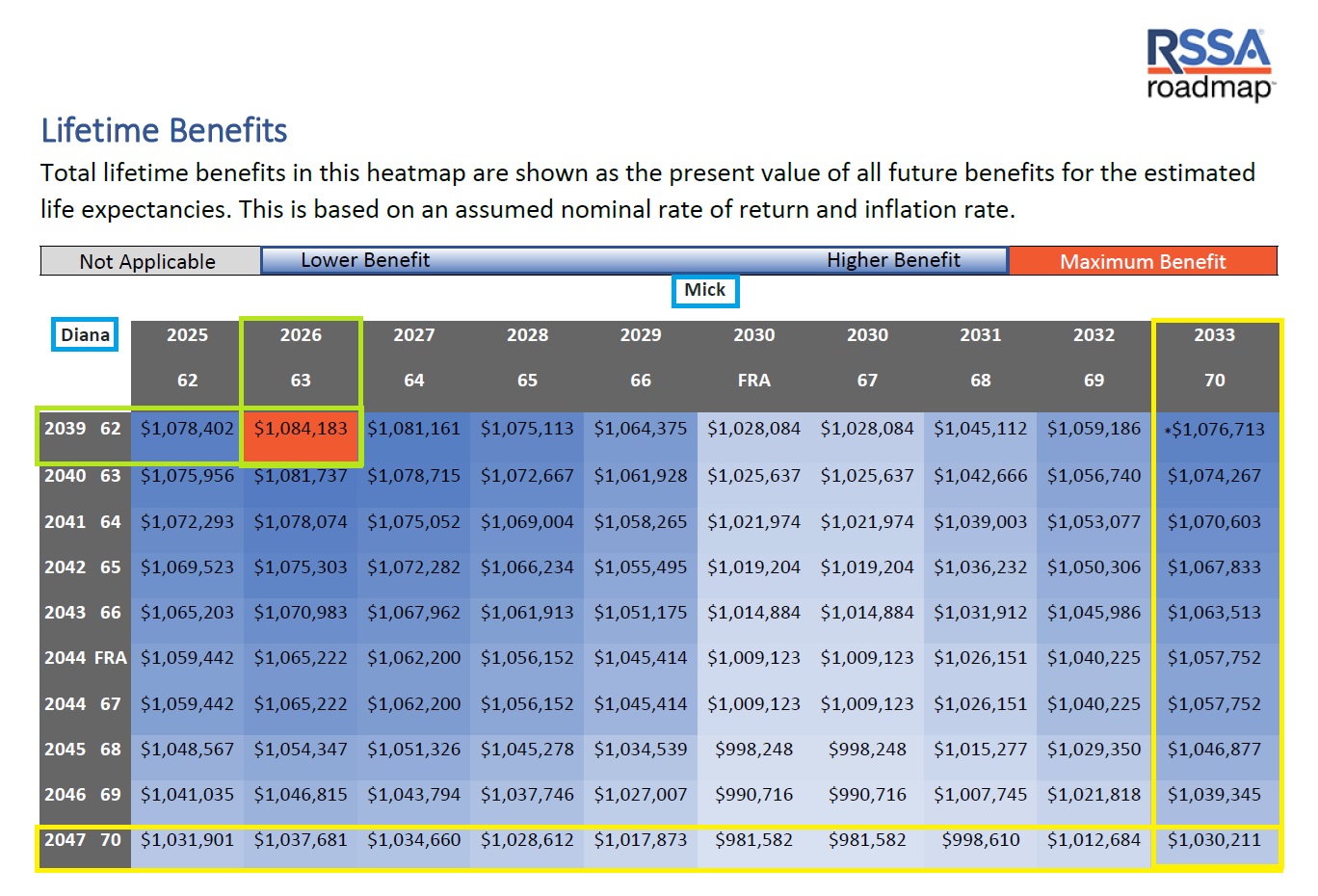

A lifetime benefits heat map is included in the Roadmap report. Along the left side is Diana’s year and age at which she can file for Social Security. Across the top is Mick’s year and age options for filing for benefits. Where Diana’s row and Mick’s column intersect, for a particular age, displays the lifetime Social Security benefits.

The maximum lifetime benefit for Mick and Diana occurs if Mick files for Social Security at age 63 in the year 2026 and Diana files at age 62 in the year 2039. The lowest lifetime benefit, according to the heatmap table, happens if both Mick and Diana file for Social Security at age 70.

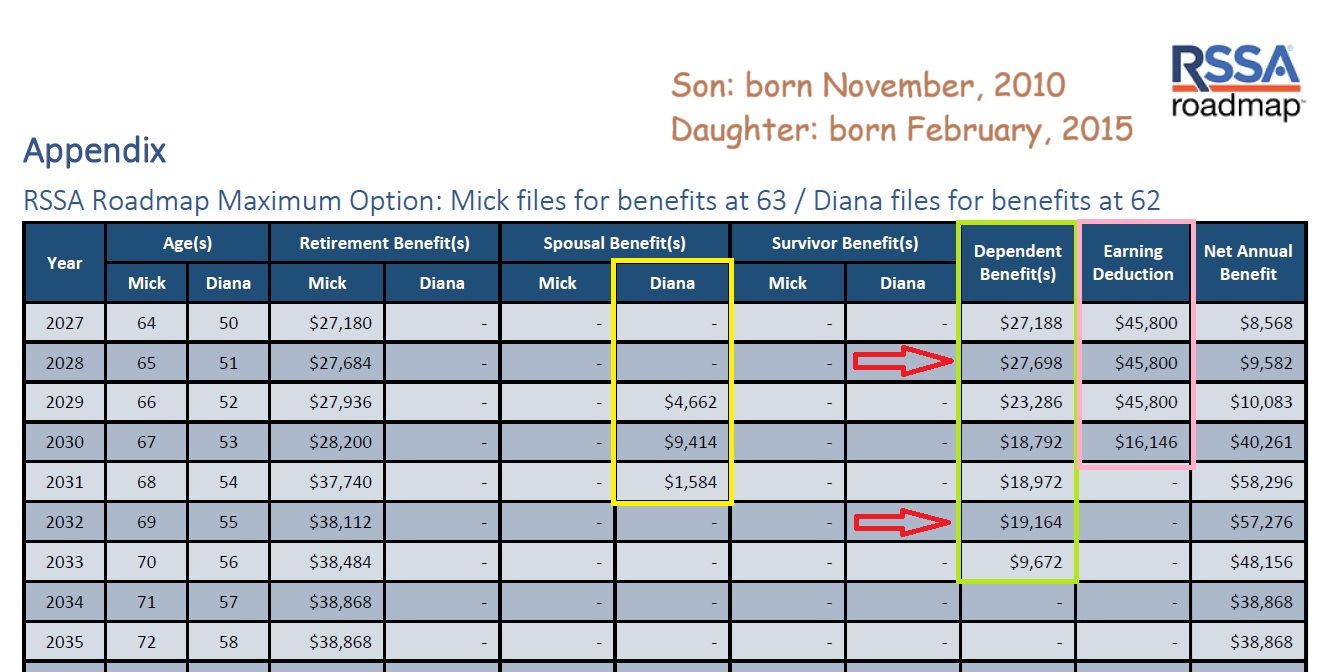

Annual Income by Social Security Beneficiary, Spouse, Dependents

The appendix of the report shows the annual benefit amount for each individual for each year by the various options. In the Maximum option, Mick’s annual Social Security retirement benefit increases each year because Mick continues to work and the Social Security cost of living allowances. Mick and Diana have children, and they are eligible for Social Security benefits through 2033 when there are no children under 19 years of age.

Diana did not receive any Social Security benefit in the first couple of the years because the maximum family benefit was met with the children. When their son turns 19 in 2029, Diana is eligible for benefit because Mick and Diana’s daughter is under 16 years of age. When their daughter turns 17, Diana is no longer eligible for a Social Security benefit. However, the daughter continues to receive a Social Security benefit until she turns 19 years old or graduates from high school.

Also note that because Mick continues to work, he incurs and earnings deduction until he reaches his full retirement age of 67. Even with the earnings deduction, the family still receives net benefit from the Social Security income benefits for Mick, Diana, and their children.

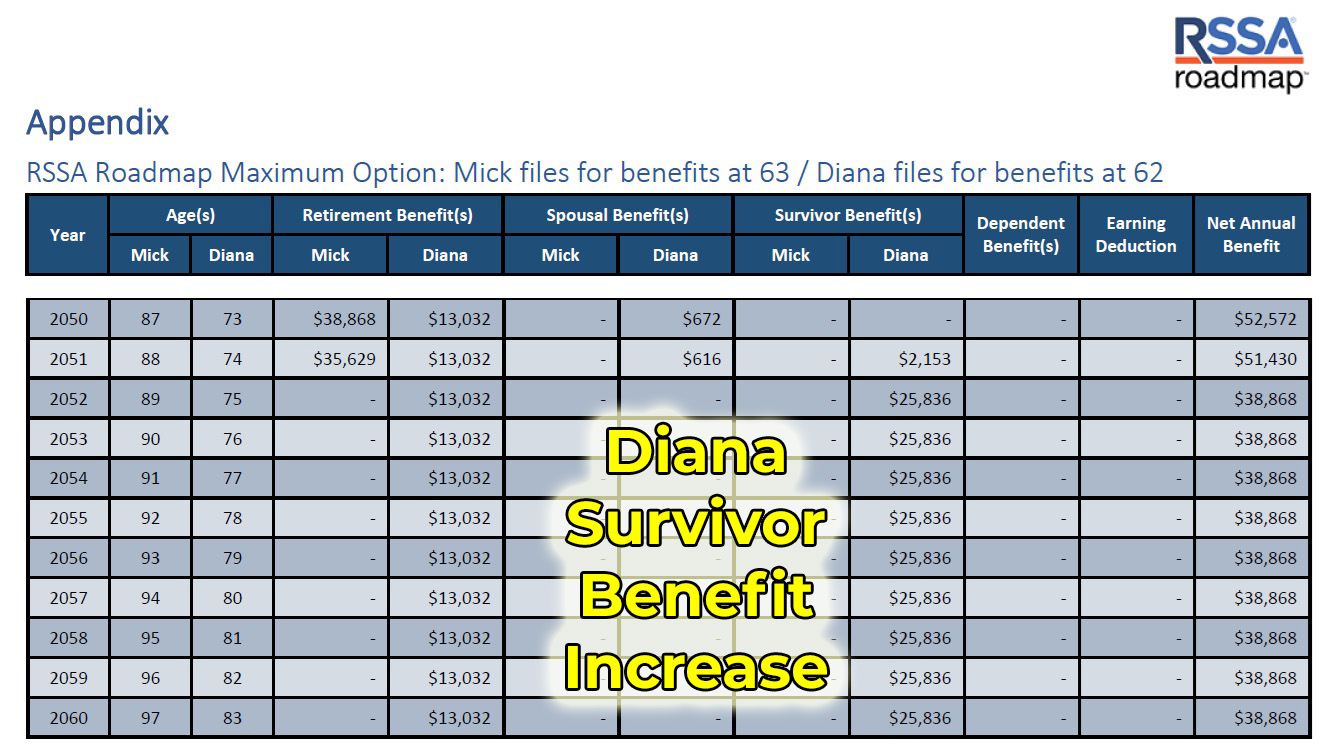

Survivor Benefits Detailed for each Option

Each option will illustrate the survivor benefits. In this case, Diana is eligible for a survivor benefit after Mick dies. The survivor benefit estimate, while far in the future, can help with planning to make sure Diana has enough income after Mick dies.

Upon reviewing and analyzing the Roadmap report, a couple like Mick and Diana have more clarity on their Social Security options. The report provides a snapshot of the various options for claiming Social Security retirement income. The individual and family still need to determine which scenarios work best for them and their situation.

YouTube video on Roadmap. Kevin Knauss RSSA Page