Taxpayers reconcile their ACA health insurance subsidies using form 8962. This post pulls from the form and instructions for 8962 to walk through the process reconciling the Premium Tax Credit health insurance subsidies received during 2025.

For the walk through, we will use Mary Lynn, a single adult, who received ACA Premium Tax Credit health insurance subsidies through Covered California in 2025.

ACA Health Insurance Subsidy Tax Reconciliation

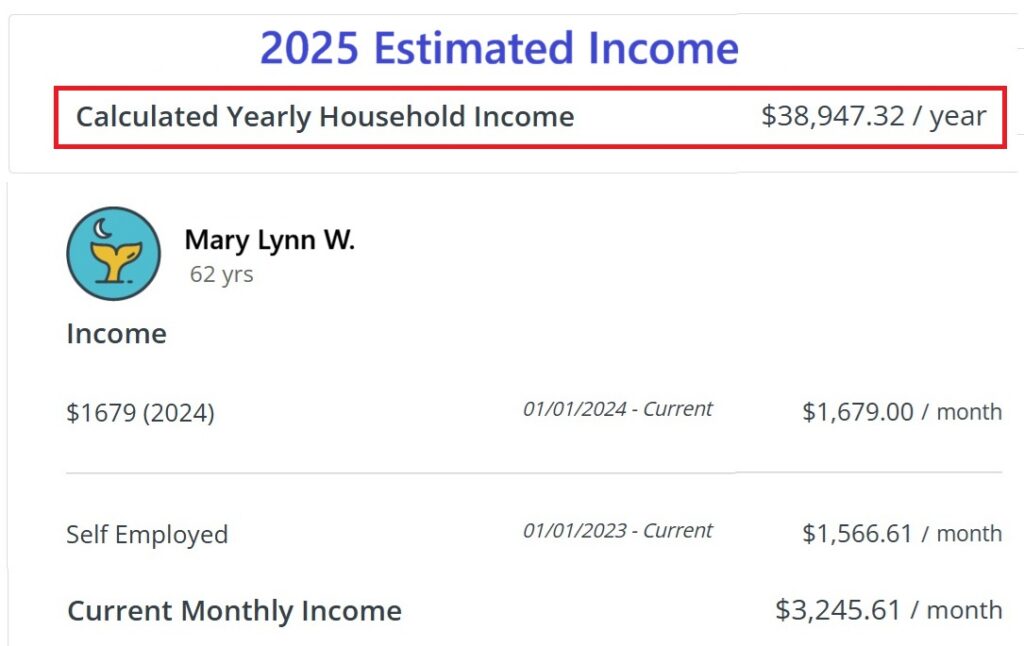

Mary Lynn had estimated her income at $38,947.32 for 2025 and received a subsidy based on that amount to lower the health insurance premium. However, Mary Lynn’s final Modified Adjusted Gross Income for 2025 came to $45,000.

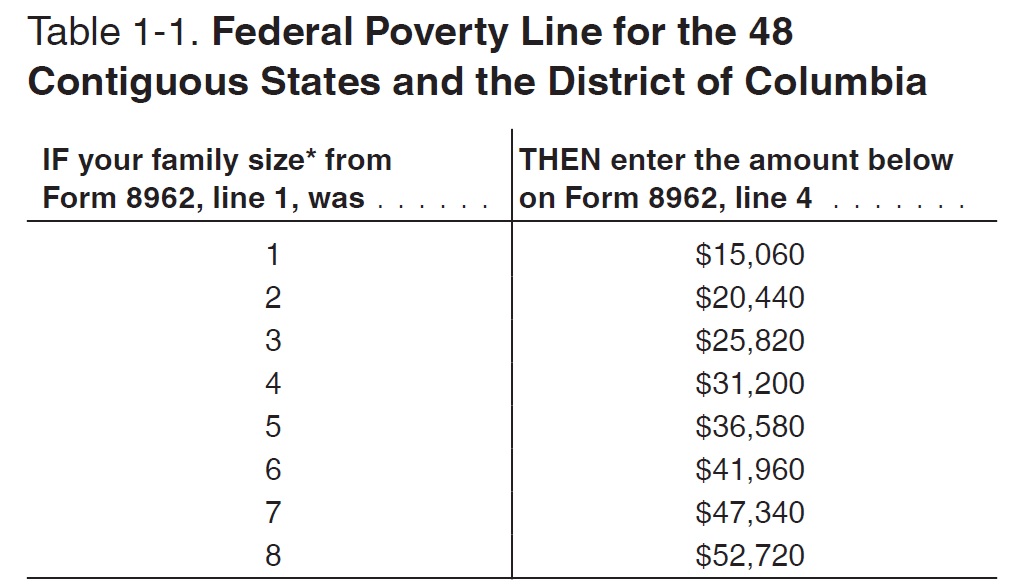

Part I of 8962 calculates the consumers fair share for health insurance, line 8a. First, Mary Lynn’s income of $45,000 (line 3) is divided by the federal poverty for 2025 found in the instructions for 8962.

The $45,000 income divided by $15,060 yields a percentage of 299 (line 5). Then you go to the 8962 instructions to find the applicable figure.

The applicable figure for an income of $45,000 or 299% FPL is 0.0596, entered on line 7. This essentially translates to a consumer fair share for health insurance as 5.96 percent of the household income. The applicable figure is multiplied by the household income to get the consumer fair share (line 8a).

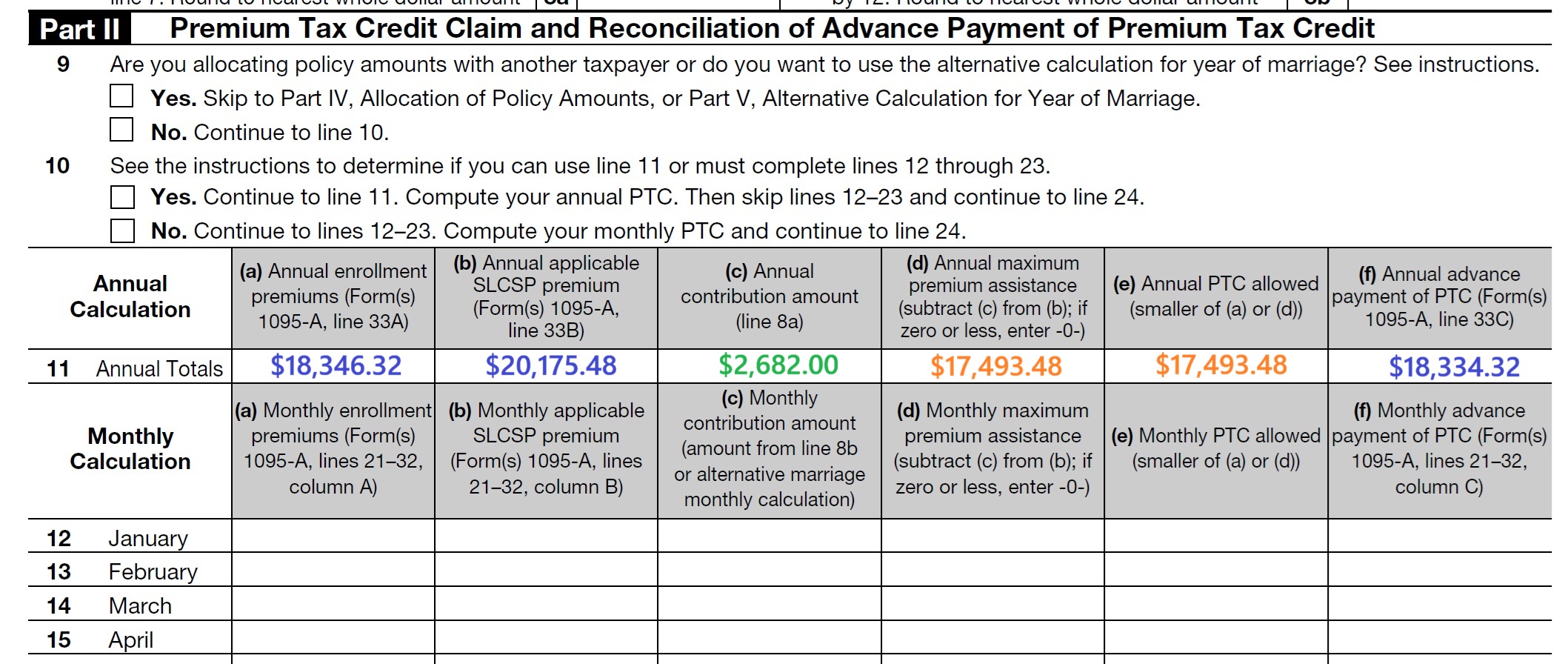

Mary Lynn received a 1095-A from Covered California that reported total monthly premiums (col. A), Monthly second lowest cost Silver plan premium (col. B), and the total Premium Tax Credit subsidy advanced to her health plan every month to lower the health insurance premium (col. C).

Form 8962 Dollar Amounts from 1095-A

Information from the 1095-A is transferred to Part II of 8962 on line 11 columns a, b, and f. If you receive multiple 1095-As you would enter the dollar amounts by month on form 8962. The consumer fair share from line 8a of Part 1 is entered on line 11c. On line 11d, the consumer fair share of $2,682 is subtracted from line 11b the second lowest cost silver plan, which is the benchmark plan for calculating the subsidies.

Line 11e is the maximum allowable Premium Tax Credit subsidy allowed for Mary Lynn. It is either the lower of the annual premiums (11a) or line 11d. For Mary Lynn, the maximum Premium Tax Credit she is eligible for is $17,493.48 or the second lowest cost Silver plan minus her consumer fair share of $2,682. Line 11e will limit the maximum subsidies to line 11a when the consumer enrolled in a health plan where the subsidy was greater than the annual cost of the health plan. This occurs when consumers enroll in some Bronze plans or lower cost Silver plans.

Repayment Limitation of Excess Premium Tax Credit Subsidy

Line 11f, total health insurance subsidies paid on behalf to Mary Lynn during 2025, is transferred to line 25. Covered California paid $18,334.32 in subsidies, but Mary Lynn, because her income was higher than estimated, is only eligible for a maximum allowable Premium Tax Credit subsidy of $17,493.48. The difference is $804.84. Mary Lynn received $804.84 too much in health insurance subsidies. She must pay this dollar amount back to the federal government (line 27 of Part III).

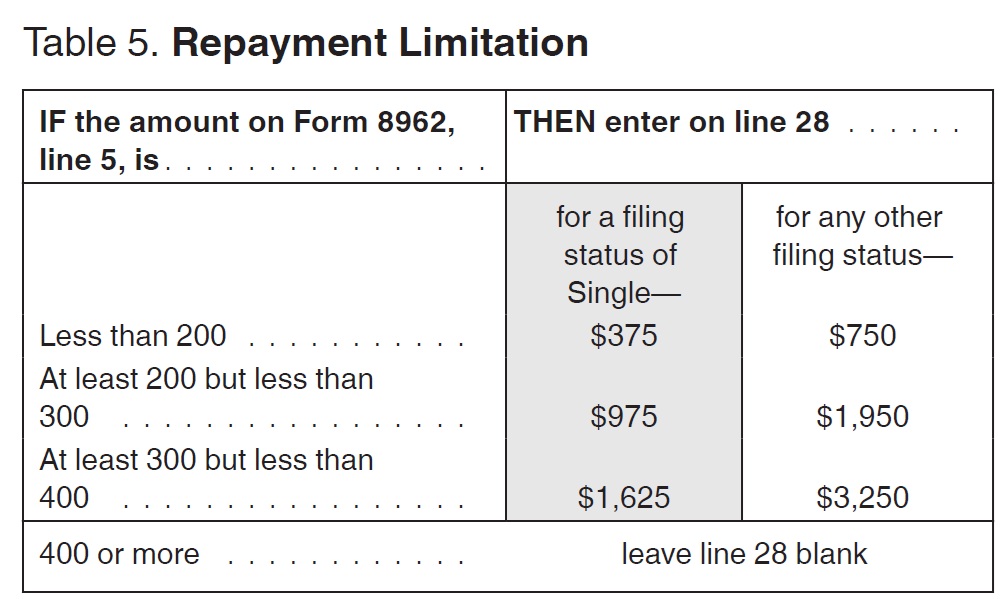

If Mary Lynn had to repay excess subsidies of $2,000, the repayment would be limited to $975 because her income is between 200% and 300% of the federal poverty level. Because her excess subsidy is less than $975, the $804.84 amount is transferred to line 29 of Part III.

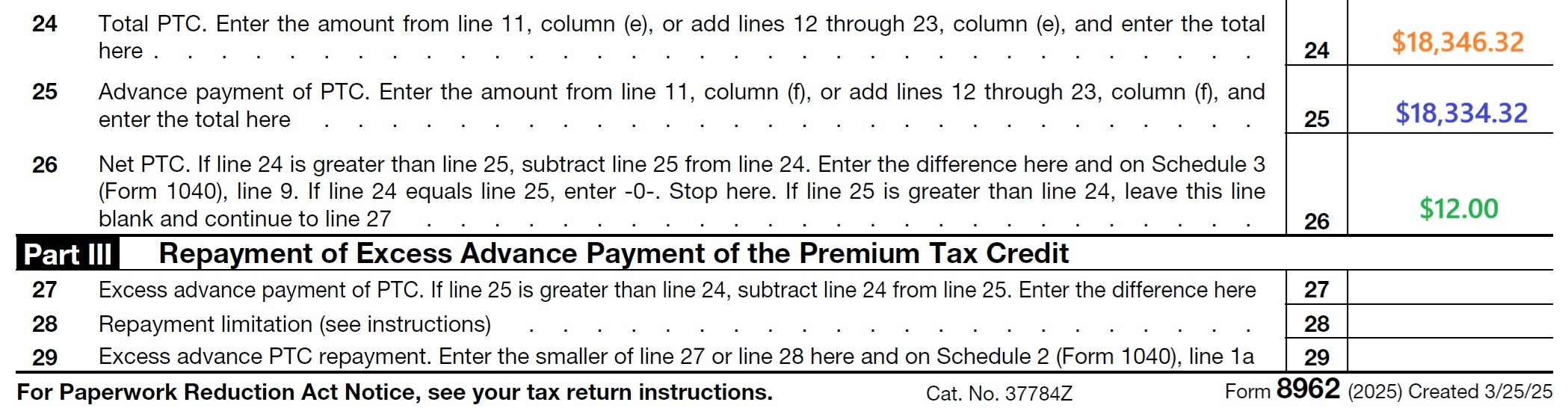

If Mary Lynn’s income was only $30,000 for 2025, less than her Covered California estimate of $38,947, she would be eligible for an additional Premium Tax Credit. At $30,000 income, Mary Lynn’s consumer fair share is only $588. Mary Lynn’s maximum Premium Tax Credit (line 11e) is the annual enrollment premiums, line 11a, or $18,346.32. Because Covered California only advanced $18,334.32, line 11f, she is due a refund, or extra tax credit, of $12.

YouTube video on the health insurance subsidy reconciliation.