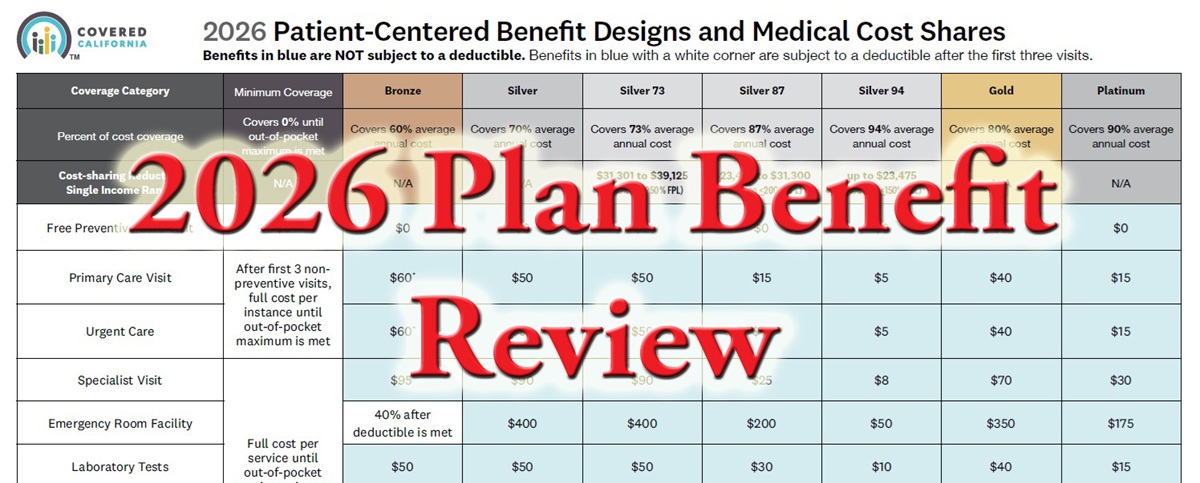

While there is turmoil surrounding the level of subsidies, the health plan options offered through Covered California are very similar to the previous year. All health plans include children’s dental and vision benefits. All of the standard benefit designed health plans – excluding enhanced Silvers – are also available off-exchange, direct from the health plan companies.

Minimum Coverage

Minimum coverage plans are available to individuals 30 years old and younger. There is no subsidy to lower the premium of the Minimum Coverage plan through Covered California. There are three health care services (any combination of primary care and urgent care) that are $0. The fourth office or urgent visit will be at the full rate. Otherwise, nothing is covered until you have accrued $10,600 in health care costs. After the maximum amount is met, the health plan covers all remaining costs with in-network providers.

Bronze HDHP

The Bronze High Deductible Health Plan has no first dollar health care services except preventive care visits. This means you pay the full negotiated rate for the services until you have met your deductible of $7,200. The deductible also happens to the maximum out-of-pocket (MOOP) amount. Once you have met your MOOP, the plan covers all services and prescriptions. The MOOP for 2026 is $7,200. Enrollment in the plan allows you to make contributions to a Health Savings Account.

Enhanced Silver Plans

The enhanced Silver plans 73, 87, 94 are only available through Covered California. They are offered based on you estimated household income. If you are offered an enhanced Silver plan (especially 87 or 94) you should seriously consider it. The reduced cost sharing and low maximum out-of-pocket amounts – in conjunction with the subsidy – make the plans a real value. The Silver 73 and 87 do have medical deductibles. However, the deductible is only applicable if you are hospitalized or in a skilled nursing facility. Otherwise, outpatient services that don’t have a set copayment, are subject to a coinsurance percentage of the total cost of the services.

Standard Benefit Bronze, Silver, Gold, Platinum

The Bronze 60 plan may be a good option for people who are looking to save money and do not use health care services on a regular basis. The Bronze 60 has unlimited office and urgent care visits at $60. You get three specialist visits at $95. Lab tests are unlimited at $50. All other health care services are subject to the medical deductible of $5,800. The Bronze 60 has a maximum out-of-pocket amount of $9,800.

The Silver 70 also has a maximum out-of-pocket (MOOP) amount of $9,800. But the Silver plan save money if the individual uses brand name or specialty drug prescriptions. After a $50 pharmacy deductible, many drugs under the Silver plan are subject to a copayment for a 30-day supply. The Silver plan’s $5,200 medical deductible only comes into play if you are hospitalized or in a skilled nursing facility. Outpatient surgery would be subject to 30 percent coinsurance.

Gold and Platinum plans have no medical or pharmacy deductible. The copayments for many routine health care services are less than Silver. Coinsurance under the Gold or Platinum plans are approximately 20 and 10 percent respectively. The Platinum plan has particularly good pricing on prescription medications, leading to quite a bit of savings. The MOOP for the Gold is $9,200 and $5,000 for the Platinum.

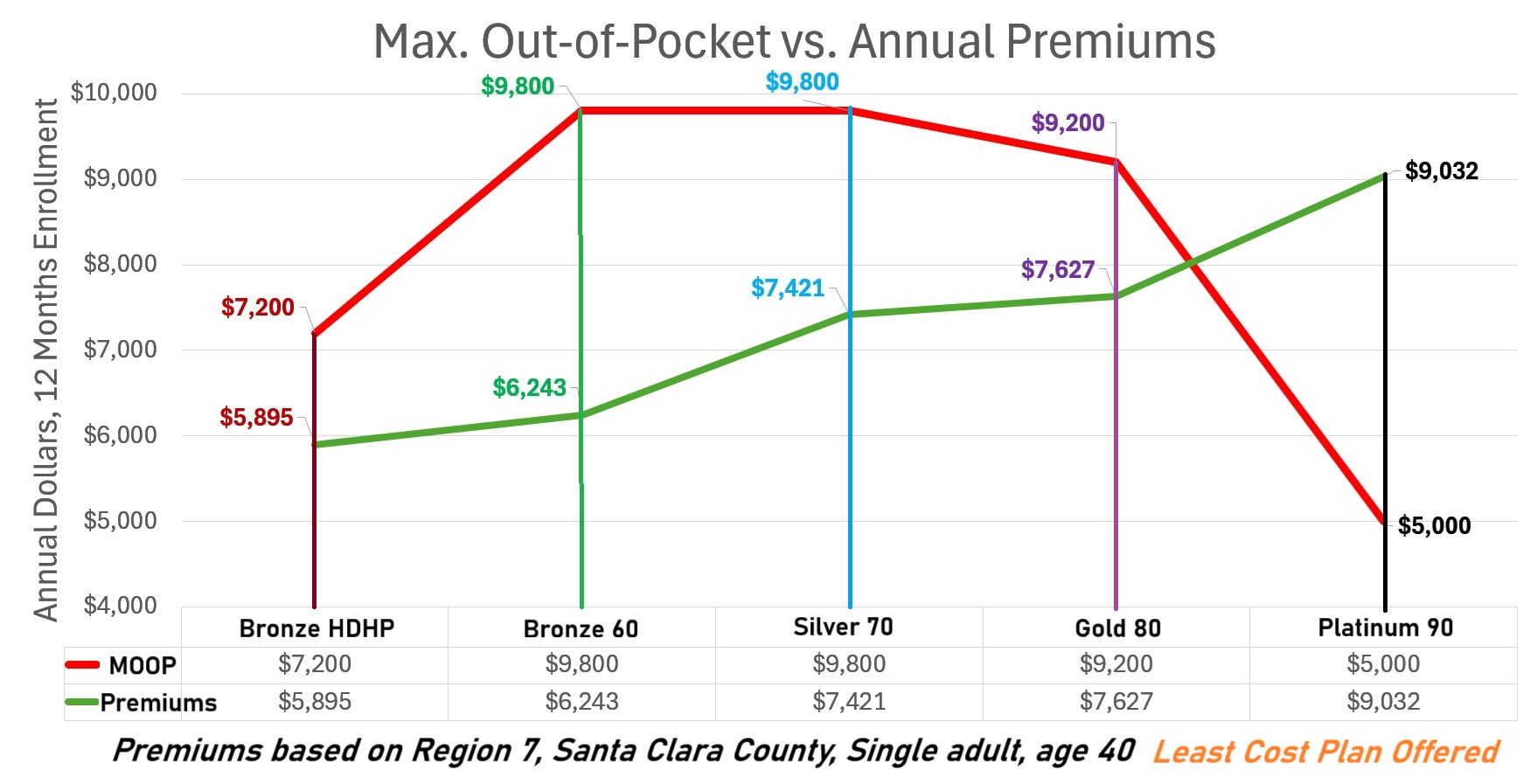

Cost of Maximum Liability Protection

Some people view health insurance as a cost to have a maximum liability to high-cost health care services. In other words, they make a monthly premium only to have a back stop to health care services in the event of a major illness or accident.

The example below is for a 40-year-old individual in Santa Clara County. The health insurance premiums are the full rate (no subsidy) for the lowest cost health plan in each metal tier. The premiums are annual, the full 12 months. The annual premium increases for each metal tier as the health plan assumes more responsibility for routine health care services.

While the premium line is below the MOOP for all tiers except Platinum, older individuals may have a premium curve greater than the MOOP of the health plans. However, the steps in the slope of the premium curve, regardless of age, will be similar. Platinum plans always have a higher premium than Bronze plans.

In this scenario, the least expensive option (MOOP plus annual premiums) is the Bronze HDHP. The Platinum plan was the second lowest. This is because of the low MOOP. If the individual never meets the MOOP of the Platinum plan, and uses very little health care services, another plan would have been a better fit. The analysis is predicated upon a medical event that would meet the MOOP of the health plan.

YouTube video reviewing the health plans.