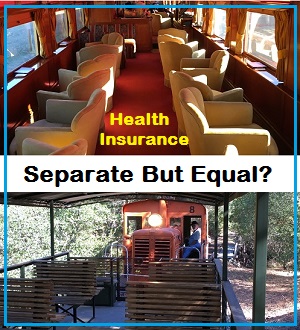

Health plans, like train cars, can be separate, but not equal. Group health plans have better networks and benefits than either individual and family plans or Medicaid. Everyone should have access to the same train car of health insurance benefits and coverage.

The United States has a system of health insurance and health care that can only be characterized as ‘separate but equal’. The dividing line is people who have employer or union sponsored health insurance versus the rest of the population that are in individual and family plans or Medicaid. For the some people the differences can be stark with a lack of timely access to care and specialists imposed by the health plans in the individual and family market’s narrow network. Why should American residents who don’t have a corporate or government employment be subject to the ‘separate but equal’ treatment premise that was dismantle for other segments of our economy starting in the 1950s?

Health Insurance Should Not Be ‘Separate But Equal’

The institution of ‘separate but equal’ treatment and facilities was promulgated by the Supreme Court decision of Plessy v. Ferguson in 1896. This court decision that upheld Louisiana’s separate but equal train cars – segregated train cars, one for whites and separate train cars for blacks – ushered in the era of Jim Crow laws. For many states, their residents lived under a quasi-apartheid system segregating to the maximum amount possible the black and white races. This extended into the public school system as well. The 1954 Brown v. Board of Education Supreme Court ruling reversed Plessy v. Ferguson, but the damage was already done in our society.

Employer sponsored health insurance really began to take off during World War II. The federal government had frozen wages to prevent inflation, but allowed companies to offer other benefits of employment. Heath insurance was one of the benefits. While employer sponsored health insurance is still a mainstay of corporate or government employment, health insurance costs have steadily increased faster than the rate of inflation.

It is the astronomical cost of basic health care and emergency care that has driven the growth for insurance from people who don’t have employer sponsored health plans. Health insurance is not so much about health care as it is about asset protection. One trip to the emergency room or critical illness can wipe out the savings of a family without health insurance and potentially force them into bankruptcy.

Employer sponsored health insurance is guarantee issue. That means regardless of your or your family’s health challenges the health plan has to accept you. Before the Affordable Care Act, individual and family plans were able to discriminate based on health conditions by either raising the individual’s rate or denying coverage altogether. Unless President Trump gets his way and repeals the ACA, health insurance for the individual and family market will remain guarantee similar to employer sponsored plans.

More Benefits With Employer Group Health Plans

The ACA went a long way to dismantling the ‘separate by equal’ division between individual plans and group plans. But while the group market employer plans and individual plans now share guarantee issue, there are still plenty of differences. Small and large group plans usually have a large networks of providers such as doctors, hospitals, urgent care centers, and out-patient facilities. Individual family EPO and PPO plans have decidedly narrow networks of providers and many doctors, even though listed as in-network, continue to refuse to accept individual and family plan members. Small and large group plans can also have larger drug formularies. In other words, they cover more prescription drugs. Individual and family plans can have smaller drug formularies leaving off popular, but expensive, brand name drugs.

Members of group plans may also get extra benefits not offered to individual and family plan members. There are wellness programs to help people lose weight, quit smoking, or increase their exercise. There may be dedicated staff to help members in group plans plan for their care before a health care procedure and while they are recuperating. Some group plans have rolled out house calls by doctors. Many of these extra benefits are absent from individual and family plans.

Slim Benefits Of Medicaid

For people on Medicaid, Medi-Cal in California, the options and benefits are even smaller. The Medicaid HMO plans have a limited number of primary care physicians and even fewer specialists. Unless you have a critical illness such as cancer or a heart attack, some Medicaid beneficiaries can wait months to see a doctor and get needed health care services. If Medicaid reform is pushed through congress and the program is turned into a block grant for states, access to health care and coverage will diminish even further.

At the highest level, the disparity in health care services cuts along employment and income lines. But we all know that the disparity of health care services hits hardest on people of color and low income families. The manufacturing companies that ushered in widespread health insurance benefits in the Midwest and southern states no longer exist. Government employment has shrunk or is growing at a much slower pace. Large urban centers are now where the bulk of companies are located that offer employer health insurance. This leaves large swaths of the United States without good comprehensive health insurance plans.

Individuals And Families Forced Into Separate Health Insurance

This raises the fundamental question of why should an individual who doesn’t work for government or a company that offers health benefits have access only to individual plans that are not as good. The plans are separate and they are not equal. Medicaid certainly is not equal to either individual insurance or employer sponsored health insurance. Why, when ‘separate but equal’ was struck down over 60 years ago, do we still maintain a health insurance system that penalizes people because of where they live or the occupations they chose to pursue?

Some supporters of the repeal and replacement of the ACA have defended the loss of Medicaid health insurance for low income people by telling them to get a job. I have no doubt that these same people would have been supporters of the Plessy v. Ferguson decision. They probably think Brown v. Board of Education was judicial overreach. We know that the advocates of repealing the ACA want states to have more control over the type of individual plans that are offered. In other words, they want to allow states to allow stripped down health insurance plans that don’t cover what has become to be known as essential health benefits.

Health Care Needs Don’t Vary By State

The logic that states somehow have unique populations of people with different health care needs from the rest of the country is a absurd. The human condition does not changed because of the state you reside in. A pregnant woman in Arkansas needs the same pre-natal and post-natal care as mother in California or New York. To mandate that employer plans cover maternity and not individual plans is just another way to discriminate against a group of people.

The goal for allowing states to limit covered benefits is an attempt to lower the cost of health insurance in general. But the health plans aren’t the problem; it’s the providers and drug companies. Once you begin to reign in the costs of health care services and drugs, you will begin to naturally limit health insurance rates. But to harness health insurance rate increases by limiting covered benefits only shifts the cost burden to members enrolled in those plans.

Negotiated Rates Hold Down Rates

Once a person turns 65, or otherwise becomes eligible for Medicare, they do enter a health insurance system that is applied equally to all persons regardless of income or employment. Medicare works to hold down health care costs by negotiating prices on a regional basis. To further hold down the increasing costs of Medicare, the Center for Medicare and Medicaid Services needs to have the authority to negotiate drug prices as well.

One obvious solution for dismantling the disparity between group plans and individual plans is to implement some sort of single payer health insurance program. The main obstacle, as I see it, is that the providers such as large medical groups and hospitals don’t want to be involved. They don’t want their revenue models disturbed. They don’t want to limit either their salaries or profits. And yet they are a main component of runaway health insurance rates because of the prices they charge. (Neither the ACA nor health care reform before congress in the summer of 2017 addresses the cost of health care.)

Virtually every hospital accepts the lower reimbursement rates from Medicare. But many hospitals, and doctors, refuse to accept the lower reimbursement rates for either the individual and family plans or Medicaid. I completely understand that a hospital is trying to balance their budget based on differing reimbursement rates they receive – for the exact same health care procedure – from Medicare, employer plans, and to a lesser extent individual plans and Medicaid.

Revenue Sharing Among Hospitals And Doctors

One option for encouraging more hospitals and medical groups to accept individual plans and Medicaid is to introduce a revenue sharing model. They have such an arrangement in major league sports and the ACA’s reinsurance program for health plans. In order to keep the smaller market sports teams competitive or health plans serving populations with greater health challenges, revenue is shared among the companies. The latest CMS report on the transitional reinsurance program among health insurance companies shows it help stabilize the market place and tempered rate increases.

Summary-Reinsurance-Payments-Risk-2016

Summary of the ACA reinsurance program to stabilize health insurance rates through 2016.

Let’s be honest, the public perception regarding certain doctors, medical groups, and hospitals is not uniform. Some of these providers are perceived as providing a higher level of care than their competitors. Consumers select plans based on the doctors and hospitals within the network. If, under a single payer plan, all doctors and hospitals are available, those with better reputations, or marketing campaigns, will see a surge in new patients. This could drain the revenue from smaller medical groups and hospitals. Consequently, those providers who may see a decline in patients could receive a transitional payment from providers who have gained under a more open market situation.

Access to health care services is not equal in the United States. Your health plan determines the type of care you receive. The health plans in the employer, individual, and Medicaid markets are separate and they are not equal. The ACA moved us in direction of more equality for all residents regardless of the market type of the health plan. Current Republican proposals under President Trump will widen the gap in disparity between group plans and individual plans. We need to move in a direction the guarantees access to the same level of health care services regardless of whether you work for government, a large employer, have your own individual plan, or are awarded Medicaid because of your income. It is time to dismantle the flawed ‘separate but equal’ assumption of health insurance in the United States.