Schedule 3 gathers additional credits and payments of the taxpayer. In this case, the taxpayer only has the $500 additional Premium Tax Credit to report and that goes on line 31 of form 1040.

Kevin Knauss: Health, History, Travel, Insurance

Posts related to the IRS and the Premium Tax Credit reconciliation, MAGI, Form 8962, for Covered California ACA.

Schedule 3 gathers additional credits and payments of the taxpayer. In this case, the taxpayer only has the $500 additional Premium Tax Credit to report and that goes on line 31 of form 1040.

Just because Joey’s 2023 final Modified Adjusted Gross Income was in the range for Medi-Cal, he will not lose his 2024 health plan and subsidies. The IRS does not report his income to Covered California to flip him into Medi-Cal. His 2024 subsidy is based on his good faith honest estimate of his 2024 income.

No one at Covered California calls the IRS for information and the IRS does not send Covered California any of your information. No one at Covered California will ever see your federal tax return unless you provide it to them.

Tom received unemployment insurance in 2021. Because of the unemployment insurance, Tom’s household income is 133 percent of the federal poverty level, regardless of his income. That 133 percent of the federal poverty level translates into $0 annual contribution for the second lowest cost Silver plan. Since the second lowest cost Silver plan premiums equaled $15,000 for the year that amount becomes the maximum subsidy allowed. Tom is eligible for an additional $2,318.40 ($15,000 – $12,681.40) in Premium Tax Credit because of the unemployment insurance benefit.

Taxpayers who have already filed their 2020 tax return and who have excess APTC for 2020 do not need to file an amended tax return or contact the IRS. The IRS will reduce the excess APTC repayment amount to zero with no further action needed by the taxpayer. The IRS will reimburse people who have already repaid any excess advance Premium Tax Credit on their 2020 tax return.

Unfortunately, many of us don’t fully factor in the costs of doing business when we think of our monthly income stream. Consequently, many small self-employed individuals may have applied and received unemployment benefits greater than the actual net taxable income received during normal business operations.

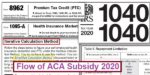

The Applicable Figure is multiplied by the MAGI. The results on Line 8a (45,000 x .0877) is $3,947, rounded up. Under the ACA, the Purmt’s should pay no more than $3,947 or $329 per month for the second lowest cost Silver plan for health insurance. The subsidy advanced by the market place exchange (Covered California, Healthcare.gov) is the difference between the cost of the SLCSP and the family’s consumer responsibility.

For most tax payers, the income they estimated on their application for health insurance will not be exactly the same amount as their final Modified Adjusted Gross Income (MAGI) on their 2019 federal tax return. Part II of form 8962 compares the subsidy you received (column f) to the amount of subsidy you are entitled to (column e) from data supplied by the market place exchange on form 1095-A.

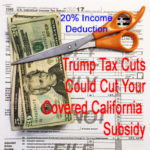

Basically, the redesigned 2018 form 1040 has made it more difficult to quickly locate all the necessary information for estimating a household’s MAGI. Virtually all of the dollar amounts were listed on the first page of the old form 1040. Now Covered California participants will have to review page 2 of the 1040 and Schedule 1 income and deductions to get most of the information for their estimated MAGI.

For the family of a small business owner, the reduction of the MAGI because of the 20% deduction could drop any dependents under 18 years old into Medi-Cal. A family of four earning $70,000 makes all the household members eligible the tax credit subsidy through Covered California. If the family reduces their income by the 20% deduction, the new income is $56,000. That is below 266% of the federal poverty level for a family of four and all dependents 18 and younger are then deemed eligible for Medi-Cal.