Health insurance companies are deploying a variety of measures to reduce fraud and abuse such as only accepting paper applications or requiring proof of residency and identity.

Kevin Knauss: Health, History, Travel, Insurance

Health insurance companies are deploying a variety of measures to reduce fraud and abuse such as only accepting paper applications or requiring proof of residency and identity.

As of January 12, 2016, I cannot recommend any individual or family enroll in a Blue Shield of California health plan either directly with them or through Covered California. As an insurance agent I have been dealing with Blue Shield’s nightmare enrollment, eligibility, and billing fiasco for over three weeks.

In 2016 Anthem Blue Cross introduced their new Tiered PPO Network health plans in four counties of California. The Tiered PPO marketing literature noted the member’s cost share would be less if he or she used a Tier 1 hospital, but it didn’t indicate how much less expensive it would be.

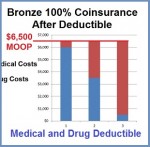

One of the most baffling health plan descriptions is the 2016 Bronze 60 health plan that states that the member is responsible for 100% coinsurance after the deductible. Most people who read this immediately shake their head and think, “I have to pay for all of my health care services EVEN AFTER I meet the deductible?” There really is no reason to buy health insurance if it never helps with the costs. The second part of the equation, not always referenced, is the calendar year maximum out-of-pocket amount of the Bronze plan which does limit a health plan members health care expenses.

It took me a long time to realize that the old adage of “It’s not what you know, but who you know” with respect to success was a crock of crap. Regardless of what or who you know, if you can’t produce something that people will consume, you will never be successful. The connections help get in you in the door. But if you can’t produce results, service, or products, you will be of little value to your associates.

Our son returned home from Williams College for Christmas break a very happy young man. His first semester at college in Massachusetts was far more challenging than he expected. It was also more fun and exhilarating than he expected. Even after the grueling course load, he was anxious to get back to Williams College and start the winter study program in early January.

As winter rain finally begins to fill Folsom reservoir from its historically low water level brought on by a prolonged drought, local residents will probably be just as quick to flush away their water conservation habits. The water conservation practices that Northern California residents temporarily adopted because of statewide drought reduction targets resulted in minimal disruption and sacrifice to our lives. That so many households easily reduced their water consumption by 25% to 50% over 2013 levels illustrates that suburban household’s waste more water than we thought. Even with Folsom Lake approaching near dead pool level in 2015, we were never pushed to conserve more water and there was never sense of urgency.

Blue Shield of California’s billing system that created major headaches for individuals and families in 2014 continues to stumble into 2016. Even through changes to the enrollment website, the simple tasks of determining an applicant’s eligibility and properly applying a premium still seems elusive to Blue Shield in several instances. For whatever reasons, several of the Blue Shield units – underwriting, eligibility, billing, member services, and IT- don’t seem to talk to one another.

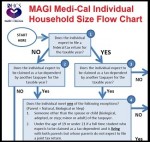

The Department of Health Care Services (DHCS) has developed a Medi-Cal household size flow chart. The DHCS Guide for Calculating MAGI Medi-Cal Individual Household Size was originally developed to help county eligibility workers ascertain the actual household size under the new Affordable Care Act (ACA) rules. The newly expanded Medi-Cal eligibility under the ACA revolves around on IRS definitions for tax dependents and non-filer rules. Because families can be so diverse and the rules regarding what constitutes a tax family so complicated, the flow chart for determining household size was created.

Even those people who hate Obamacare come running to it when they need help. A person who contacted me to clarify that he could enroll in an Obamacare plan because his Christian health care sharing ministry wouldn’t cover pre-existing conditions shows how people use these sharing ministries to dodge Obamacare and reveal their hypocrisy when they do need real health insurance.