You might assume that a life insurance agent like me would have lots of life insurance, but I don’t. I only have $25,000 in life insurance for my final death expenses. While some people want a large death benefit to leave to their family or friends, I only want a life insurance death benefit to cover expenses such as cremation, settle outstanding debts, and provide for a small celebration of life gathering.

Of course, everyone’s wishes for their final sendoff are different. Like most people, I only began thinking of end-of-life scenarios when I reached my 50s. My primary goal is not to burden anyone with the costs of my death whether that is paying for medical expenses or covering credit card purchases.

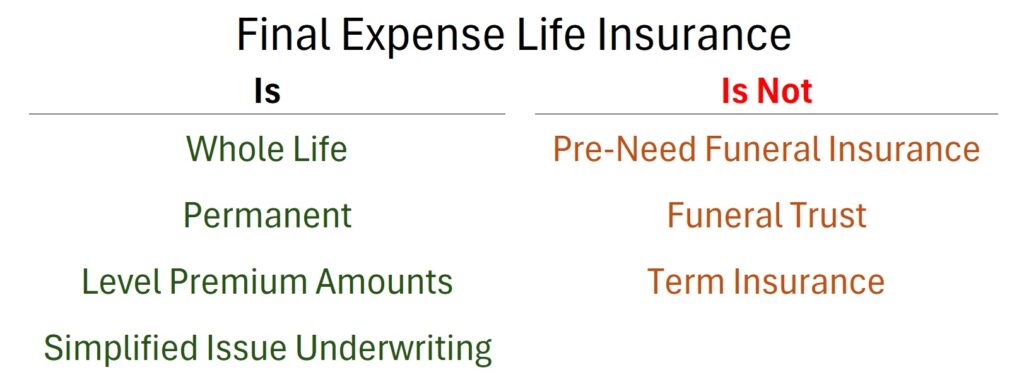

It would be wonderful to leave family members, nonprofits, and charities large sums of money as a legacy with life insurance proceeds. However, the cost to purchase a large amount of permanent life insurance when you get older is very expensive. The permanent, or whole life, insurance known as final expense life insurance is more affordable, relative to my budget.

There was a time when I had lots of life insurance. When my son was young and I wanted to make sure he had enough money for college, I had a large term life insurance policy. Now that he is through college, I don’t see a need for a large monthly or annual premium for life insurance. I would rather put a little extra money into savings for the next big expense such as car repairs, a new roof on the house, or some other unexpected expense.

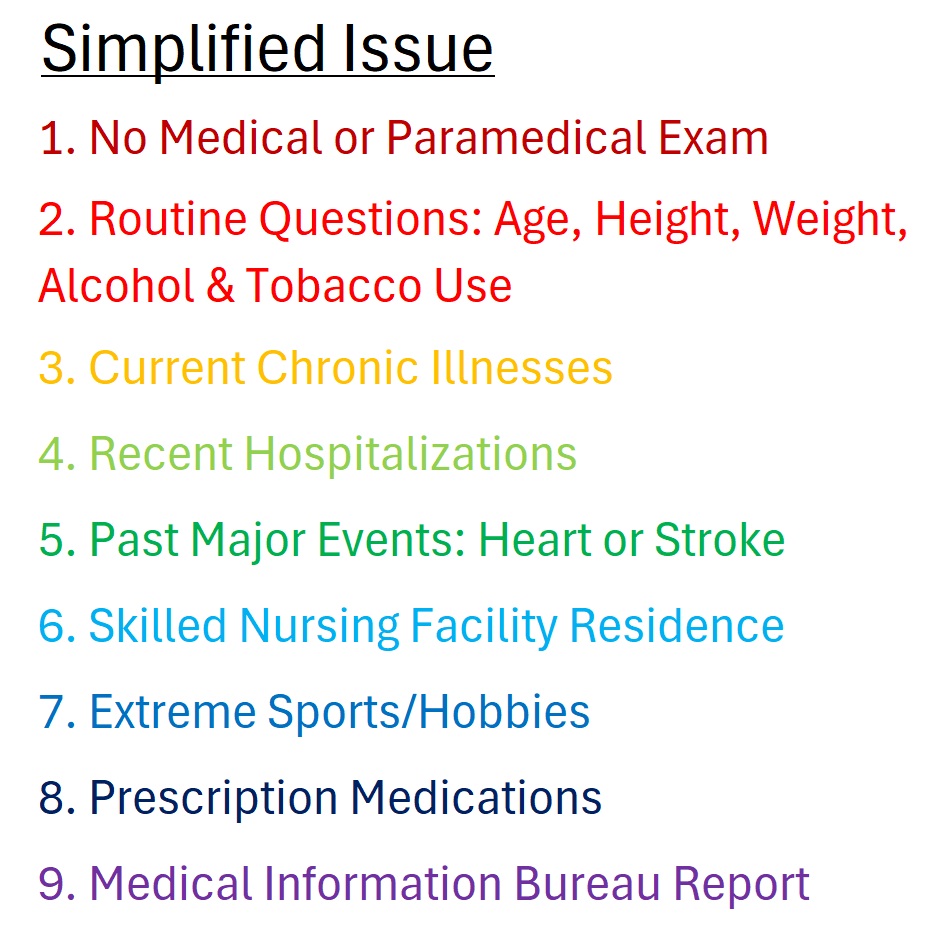

Consequently, I only need a small amount of life insurance to cover my final expenses. Fortunately, final expense life insurance can be affordable because of the relatively small death benefit compared to big term life insurance policies. Conversely, final expense life insurance is more expensive than term life insurance, per thousand dollars in death benefit, because it is simplified issue. There are no medical exams and only a few health questions.

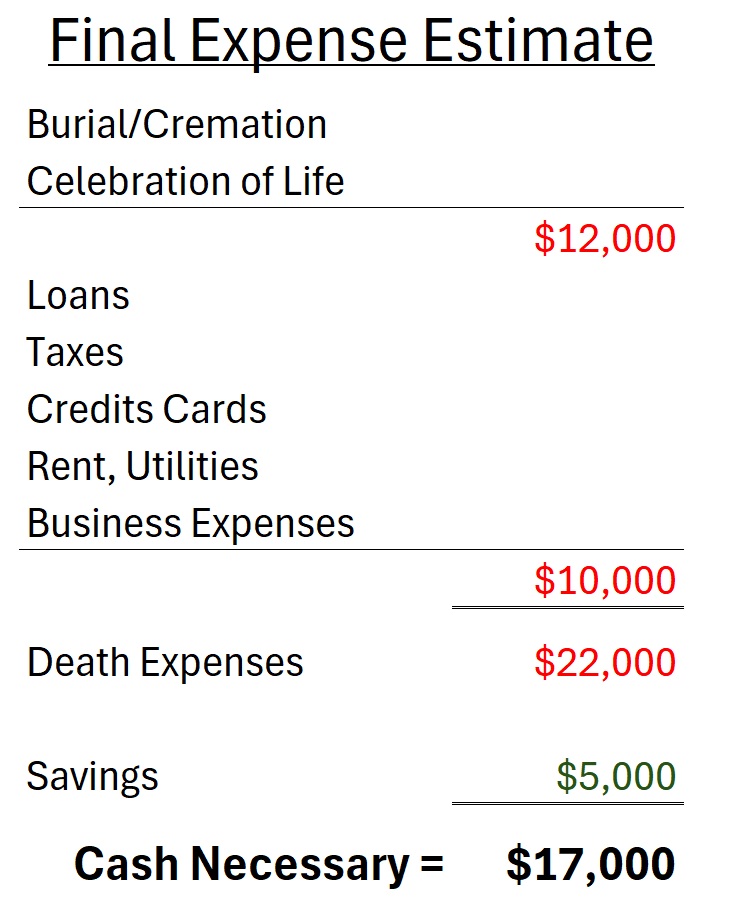

In my review, I have budgeted $12,000 for cremation and a small celebration of life. This amount is high, but I was trying to factor inflation if I live a long time. Next, I estimate it will take $10,000 to clear up all of my outstanding debts and business expenses. This dollar figure is inflated as I may die after I retire and no longer have business expenses or quarterly estimated tax payments. I am hoping that my small $5,000 in savings will be easily accessible to pay for the final expenses. Subtracting savings, I figure $17,000 in cash is required. A $25,000 final expense policy will cover the current situation and allow for inflation in the future.

A final expense life insurance policy can have a death benefit as little as $5,000 or as much as $50,000. The final expense life insurance is permanent. As long as you make the monthly or annual premiums, it won’t be cancelled. It has a fixed premium for the life of the policy. The premium will not increase because of inflation, or you become ill.

Final expense insurance is like a traditional life insurance policy. You name a beneficiary to receive the death benefit. After the designated beneficiary clears up your final expenses, any leftover funds are theirs to keep. The final expense death benefit can be assigned to a favorite charity, church, or nonprofit if the money is not needed for final expenses.

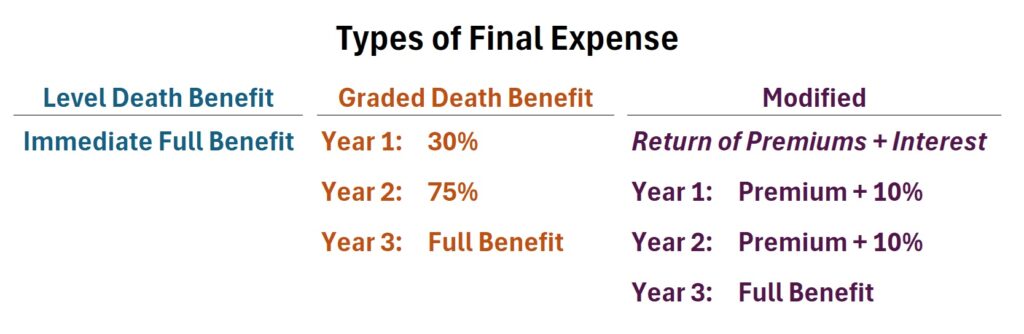

Some policies have certain conditions that help reduce the premiums. Graded final expense life insurance policies will pay a certain percentage of the death benefit if you die in the first couple of years. They might only pay 30 percent in year one, 70 percent in year two, and 100 percent in year three onward.

Another product type is the modified final expanse policy. If you die in the first two years of the policy, the insurance company returns all the premiums paid plus interest. In year three, the policy pays the full death benefit.

Final expense life insurance policies are simplified issue. There are no medical exams. There are questions pertaining to your overall health and past medical history. While you may have some chronic illnesses, that does not mean you will not be offered a policy. The rates may be higher, or it might be a graded or modified policy type. The underwriting is not as stringent as someone applying for a million dollars of term insurance.

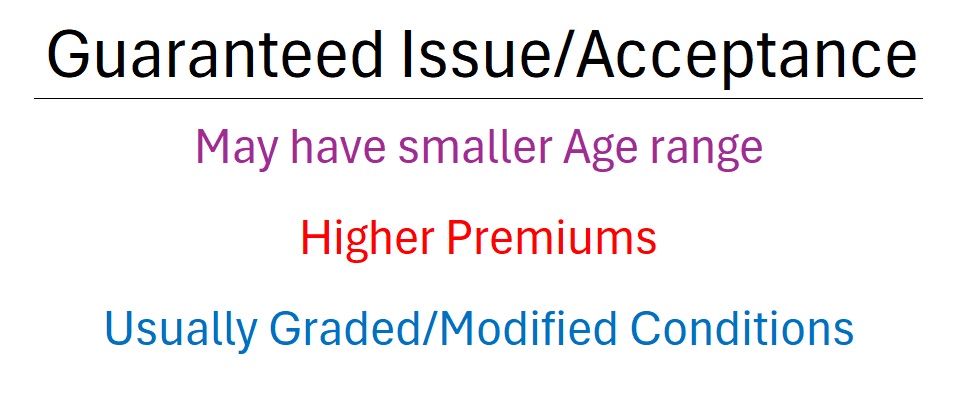

Some final expense life insurance policies are guaranteed issue. In other words, you will be issued a life insurance policy under almost any health situation. Expect these guaranteed issue policies to have a lower maximum death benefit and higher premiums. Guaranteed issue policies may also have the graded or modified conditions.

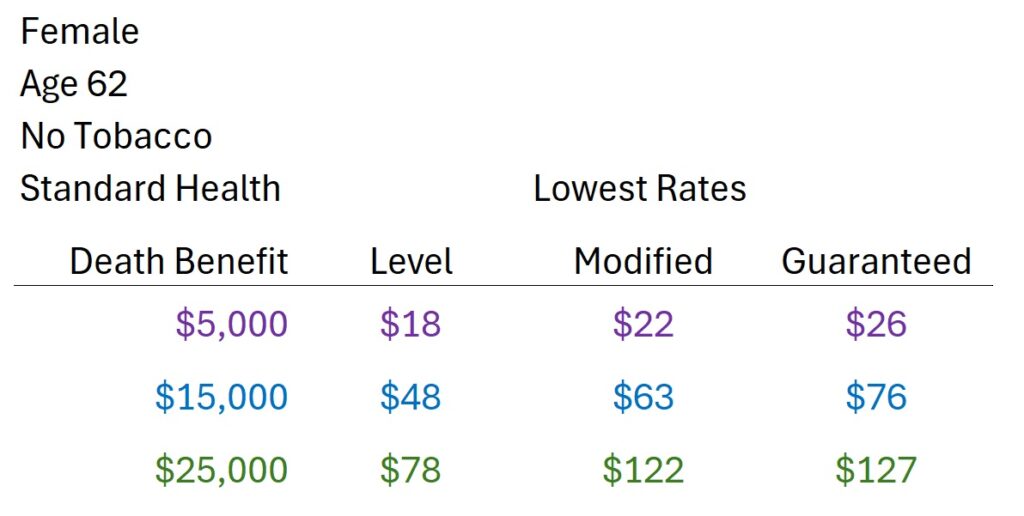

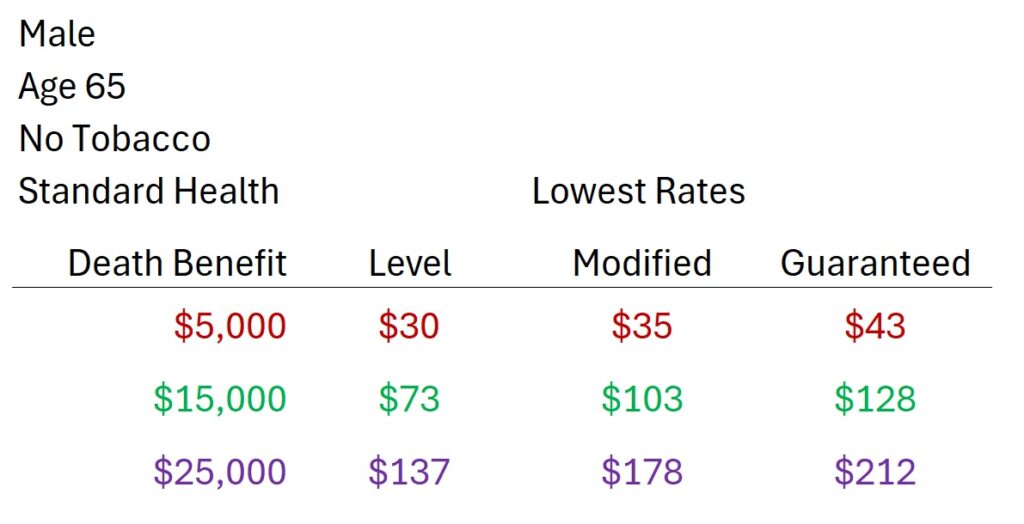

A 62-year-old woman with standard health may be able to obtain $15,000 in level final expense insurance for less than $50 per month.

The rates for men are always higher than for women. A $15,000 policy of level final expense insurance can be 1.5 time more expensive. In all cases, as the death benefit increases, the monthly or annual premiums increase. Rates will also be higher with modified and guarantee acceptance policies. Usually, modified conditions are the result of a health concern for the individual. However, that doesn’t mean the individual won’t be issued a policy, only that it has a higher premium.

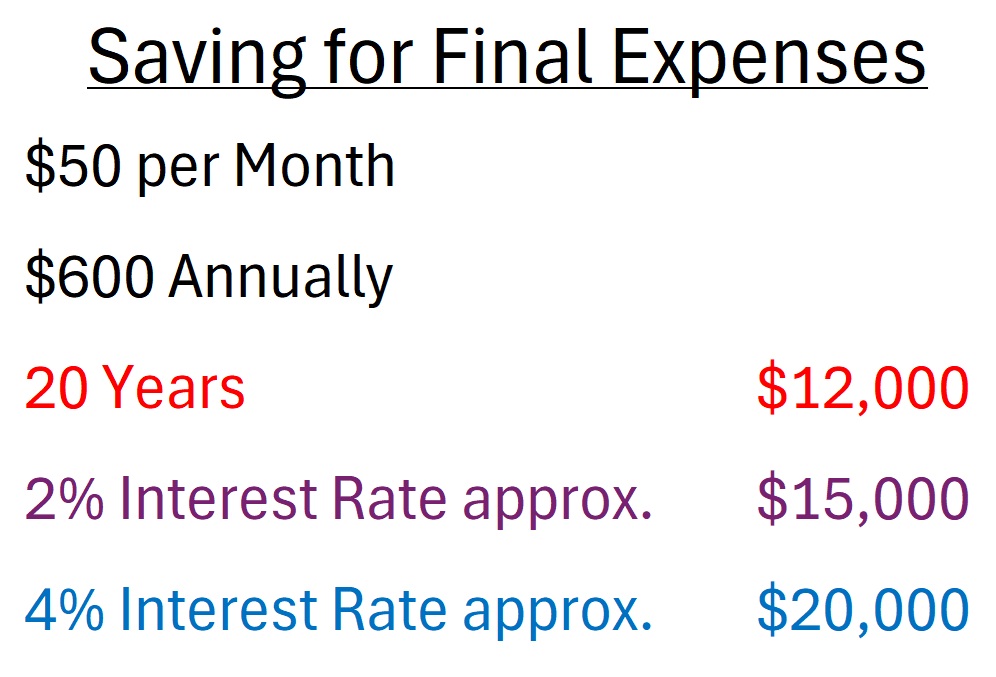

If a person starts saving for their final expenses when they are 50 years old, with just $50 per month, they could accumulate $12,000 in 20 years. If they are able to get a 2% or 4% interest rate on the deposits, after 20 years, they could accumulate $15,000 or $20,000. This would be equivalent to a final expense life insurance policy.

Of course, the benefit of life insurance is that it will pay immediately, potentially long before you have saved an equivalent amount of money. Final expense insurance can supplement any savings that has been accumulated. The policies generally pay within a few days of the insurance company receiving the death certificate. This relatively quick cash could be important if other assets such a car, home, or other property will require months before being liquidated. In other words, the life insurance helps the family meet obligations for funeral, burial, cremations, or life celebrations without a strain on their finances.

YouTube video of my final expense life insurance.