Don’t be shocked if you are moving from Covered California to Medicare only to find worse coverage, fewer benefits, and higher costs. Covered California plans are fairly comprehensive and if you are receiving a hefty monthly subsidy, very affordable. Original Medicare is not the comprehensive health plan we are used to from Covered California. However, you can bundle a package of benefits together that is close or better than some Covered California health plans.

You cannot be enrolled in Medicare and a subsidized Covered California health plan. If you are eligible for Part A of Original Medicare, you are ineligible for the federal and state health insurance premium subsidies. If you don’t terminate your Covered California subsidized plan when your Medicare becomes active, you may have to repay all the subsidy amount you received for those months when Medicare became effective.

The Costs of Medicare

For most people, Part A of Original Medicare will be premium free if they, or their spouse, worked for 10 years, or 40 quarters, and paid the Medicare tax. Part B will have a monthly premium ($144.60 for 2020.) You must pay the monthly premium, either quarterly or have it deducted from your Social Security retirement check.

Original Medicare has no prescription drug benefits. You will need to enroll in a Part D prescription drug plan. If you don’t enroll in a Part D drug plan you be assessed a Late Enrollment Penalty. Part D plans can range in monthly premiums anywhere from $15 per month to over $80 per month.

At a minimum, your Medicare costs will be the Part B premium and the Part D drug plan premium. Unless you qualify for extra help from either Medi-Cal or Social Security Low Income Subsidy Part D program, you can count on a monthly cost of $160 for Medicare. That could be much higher than you are paying for your Covered California plan. But wait, it gets worse.

If you are enrolled in a Covered California enhanced Silver plan 94, 87, or 73, you have been receiving reduced cost sharing benefits. The Silver 94 for 2020 has $5 office visit copayments, $8 lab tests, and $50 for emergency room treatment. The drug benefit of the Silver 94 is equally as generous with non-preferred brand name drugs at $15 for a 30-day supply. The Silver 94 has a $1,000 maximum out-of-pocket amount.

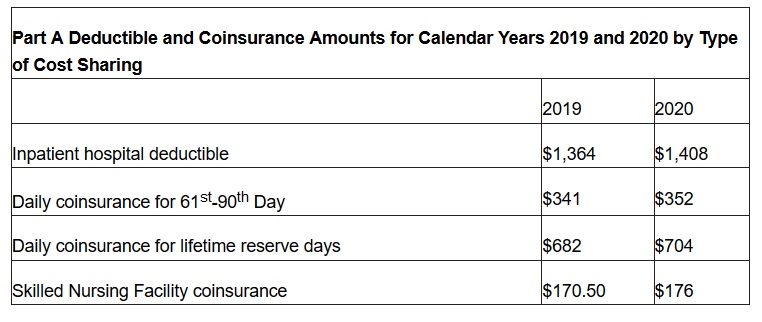

Original Medicare has no maximum out-of-pocket amount. Part A does have a hospital deductible of $1,408 for the first 60 days in 2020. Part B, out-patient services, has a $198 deductible then you go into 20% coinsurance on all Part B services for the rest of the year. Medicare does not cover acupuncture, chiropractic, podiatry, dentistry, or optometry and eye glasses. Similar to a Covered California plan, you will need a separate insurance plan for dental and vision services.

Reducing the Cost of Medicare

Unless you qualify for extra help from Medi-Cal, you will have to pay the Part B premium. If you don’t qualify for Medi-Cal, which has income and asset limits, you may still qualify for the Social Security Low Income Subsidy for the Part D prescription drug plans. The Social Security LIS has higher income and asset levels than Medi-Cal. Apply for both Medi-Cal and Social Security as you have nothing to lose if you are denied. Another way to lower the monthly Medicare costs is to enroll in a Medicare Advantage plan that includes prescription drug coverage. There are frequently many Medicare Advantage plans that have monthly premiums as low as $0 per month, with drug coverage.

The Medicare Advantage plans are more like a Covered California health plan with predictable copays, coinsurance, and a maximum out-of-pocket amount. Some Medicare Advantage plans will even have some added benefits for chiropractic, dentistry, and vision. But the Medicare Advantage plans will not have the large nationwide network of doctors and hospitals like Original Medicare. Medicare Advantage plans will be HMO plans or a PPO with a regional network of providers.

Another option is to get a Medicare Supplement or Medi-Gap plan. Medicare Supplement plans cover many of the costs of Original Medicare. Medicare Supplement Plan G will cover all of the Original Medicare Part A deductible and other coinsurance associated with Part B. It will not cover the Part B deductible. Plan G monthly rates for a 65-year-old will be approximately $150. Medicare Supplements don’t cover prescription drugs. You will need a separate Part D plan for drugs.

If you opt for Original Medicare plus a supplement, and a drug plan, you will be looking at a monthly cost of approximately $325 per month. The amount may be considerably higher than what you are paying for your Covered California subsidized plan. That’s why it is important to apply for extra help from Medi-Cal and Social Security to reduce the health and drug insurance costs.

Medicare Claim Number

If you are not receiving Social Security, and won’t for several years, you may have to push your Medicare enrollment. For some people, Social Security automatically starts the process of getting your Medicare card and claim number to you. Social Security is the gateway because they know what your income is every year and if you are eligible for premium free Part A.

If you have not received any correspondence from Medicare approximately four to five months before you turn 65, reach out to Social Security. Go to the Social Security website and apply for Medicare. You need to get the Medicare card with the claim number before you can enroll in a Medicare Advantage plan, Part D drug plan, or a Medicare Supplement plan.

Terminate Covered California Enrollment

Your Medicare coverage will usually start the 1st day of the month in which you turn 65 or become eligible for Parts A and B if you are under 65. This means you want to terminate your Covered California enrollment by the 15th of the previous month. Your Covered California health plan will not be automatically cancelled just because you turn 65 or gain Medicare coverage. What may be shut off is the subsidy. You may find that you have to pay the full price of your health plan if you have not activated Medicare and terminated the Covered California plan.

If you have a Covered California plan with a spouse or dependent, you will want to remove just yourself from coverage. Don’t remove yourself from the household. The subsidies are based on the household size. If you remove yourself from the household, the subsidy for the other household members will be incorrectly reduced. If other household members are in Medi-Cal, you will need to notify your county Medi-Cal office so they can make the appropriate changes on their end.

Additional Medicare Information