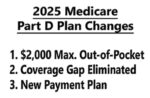

Social Security recipients who have a Part D drug plan need to review their 2025 monthly premium rate. The changes to the Part D drug plans with a lower maximum out-of-pocket amount has forced many Part D plan sponsors to raise their monthly premiums. Rate increases of $30 to $50 per month is not uncommon.