There are some situations where you must apply for Original Medicare as you approach age 65. Other scenarios give you the ability to delay enrollment into Original Medicare and the Part B premiums. I’ve put together a decision tree on the most frequent situations and whether you need to enroll or delay Medicare.

Medicare and Social Security Benefits

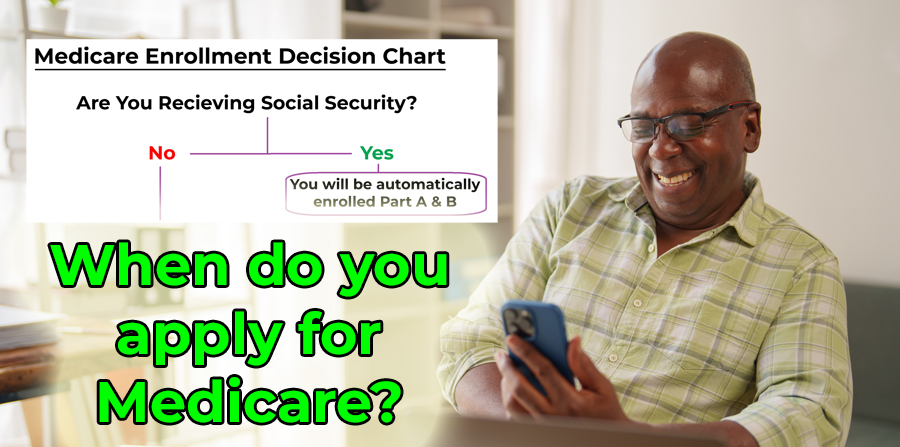

If you are receiving Social Security retirement benefits you will be automatically enrolled into Original Medicare. You don’t have to take it. Part A, hospitalization, is usually $0 premium a month if you or a spouse have worked for 10 years and paid Medicare taxes. If you are still working and have employer group coverage, you may want to opt out of Part B.

Medicare and Employer Coverage

If you are not receiving Social Security, the next question is if you have employer group coverage either through your work or that of a spouse. If yes, are there less than 20 employees in the company? If no, your employer is considered a large employer and the employer group plan is primary payor. This means the employer plan will pay for health care services first, then Medicare pays as the second payor.

This means you don’t have to enroll in Medicare when you have an employer group plan and the company has more than 20 employees. The employer group plan should be considered creditable coverage. Consequently, when you or your spouse separate from the employer, you can enroll in Medicare and not be subject to a late enrollment penalty.

If your employer has less than 20 employees, Medicare is primary payor. This means the group plan may wait until Medicare pays their portion of the health care. If you don’t have Medicare then you may have a big health care bill to pay. If you have coverage through a small employer group, seriously consider enrolling in Medicare.

Individual Health Plans and Medi-Cal

If you don’t have employer group coverage you may either have an individual and family plan or Medi-Cal. If your health plan is through Covered California, you will eventually lose the subsidy when Covered California determines you are eligible for Original Medicare Part A. Usually, Medicare is less expensive than paying the full premium of the individual and family. In addition, enrolling in Medicare when you are first eligible will avoid any late enrollment penalty.

If you have Medi-Cal, you need to enroll in Medicare. You may still be eligible for Medi-Cal extra help based on your monthly income and assets. With the Medi-Cal extra help, they are only covering the Medicare cost sharing. Medicare is the primary payor for health care services.

If you are using Veterans Affair health care services, it may be very advantageous to enroll in Original Medicare for extra protection from high health care costs. If you have CHAMPVA or TRICARE, according to the Medicare website [https://www.medicare.gov/basics/get-started-with-medicare/sign-up/when-can-i-sign-up-for-medicare] you need to enroll in Medicare. If you have TRICARE and are active duty, it is treated as a large employer and you don’t need to enroll into Medicare.

YouTube video of Medicare enrollment decisions.