The High Deductible Plan G Medicare Supplement will save you money based on the lower monthly premiums versus a standard Plan G. It could also cover significant portions of your Original Medicare cost sharing. However, High Deductible Plan G members must be cognizant that they need savings to cover the costs of Medicare health care costs.

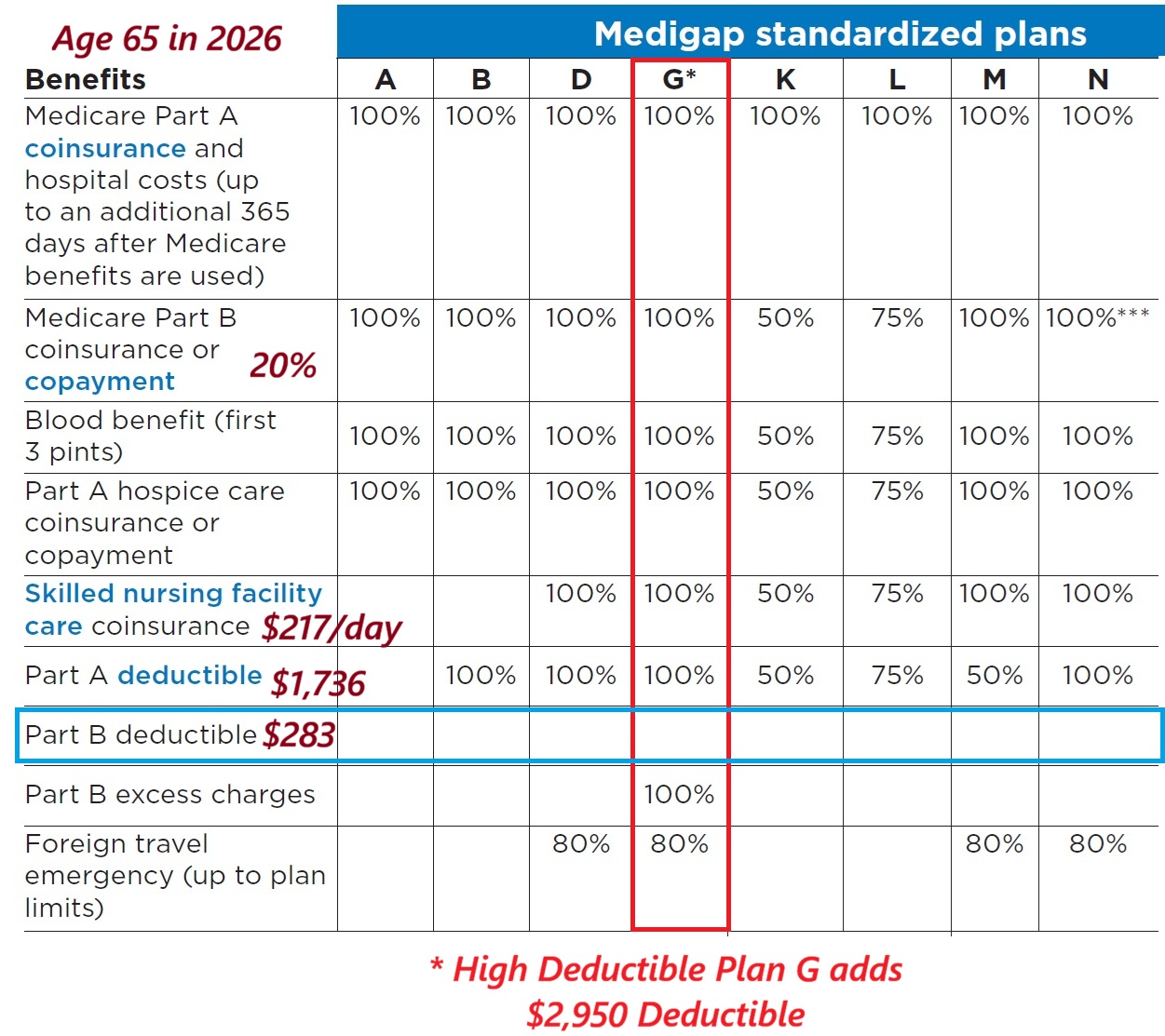

This analysis compares the High Deductible Plan G versus the standard Medicare Supplement Plan G. Standard Plan G covers all Original Medicare health care costs except the Part B deductible of $283 for 2026. The High Deductible Plan G adds a deductible amount of $2,950 (2026) before it covers all of the Original Medicare costs like the standard Plan G.

Premium Savings with High Deductible Plan G

Understandably, if you are bearing more of the Original Medicare health costs under a High Deductible Plan G, the monthly premiums should be lower. The monthly premiums for a High Deductible Plan G can be half or more of a standard Plan G rate.

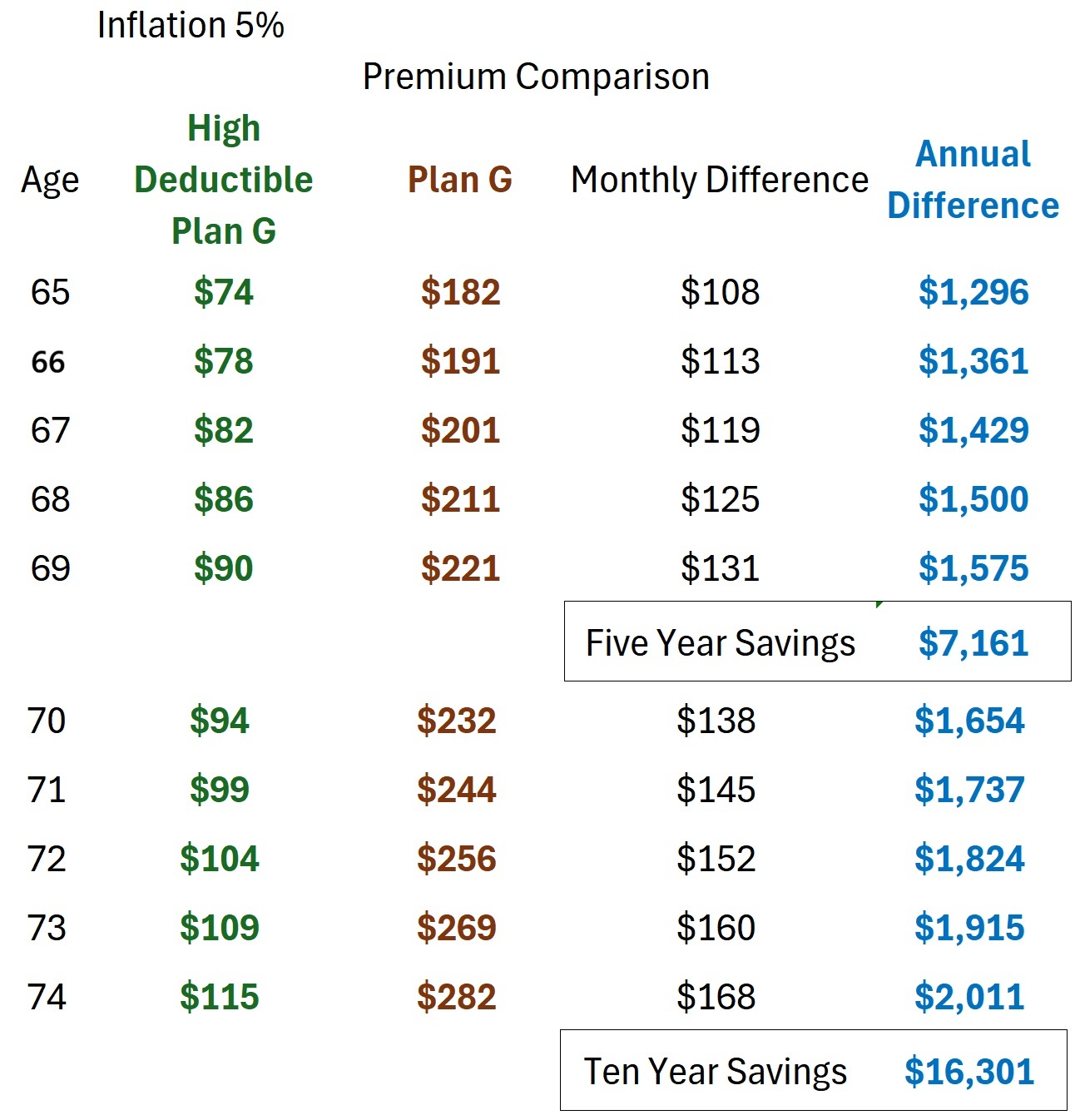

This monthly premium comparison is directly from the rate sheet of a insurance company both offering High Deductible and standard Plan G Medicare Supplements in Northern California. The rates are based on guaranteed issue. They are not adjusted for inflation, and no discounts have been applied. This particular health insurance carrier uses age bands. This means that the rates, as published for 2026, are the same for two consecutive years. A 66-year-old pays the same rate as a 65-year-old. Most carrier increase the rate for each year of age.

Let’s say you become newly eligible for Original Medicare at age 69 in 2026. The High Deductible Plan G monthly premiums will be $91 a month versus a standard Plan G at $218 a month. That is a monthly savings of $127 a month or $1,524 annually. In general, the monthly premium difference with this carrier, between the High Deductible and standard Plan G ranges from $1,200 to $1,700 a month.

Inflation Increase Plan G Rates Over Time

Of course, this comparison is in the absence of inflation increases. The carriers can apply a universal increase to the rates for all plans and ages. Between 2016 and 2025, the Consumer Price Index inflation averaged 8 percent. In other words, in addition to receiving a higher monthly premium because you get one year older, the premium may also be bumped up because of inflation.

In this rate comparison, I have applied a 5 percent increase to all rates. Because the High Deductible Plan G has a lower premium to begin with the final dollars amounts are not as large as the Plan G. For example, the High Deductible Plan G at age 74 increased from $107 to $115. The standard Plan G increased from $255 to $282. The premium savings between the two plan types is also larger by $20 a month.

High Deductible Plan G and Medicare Health Care Costs

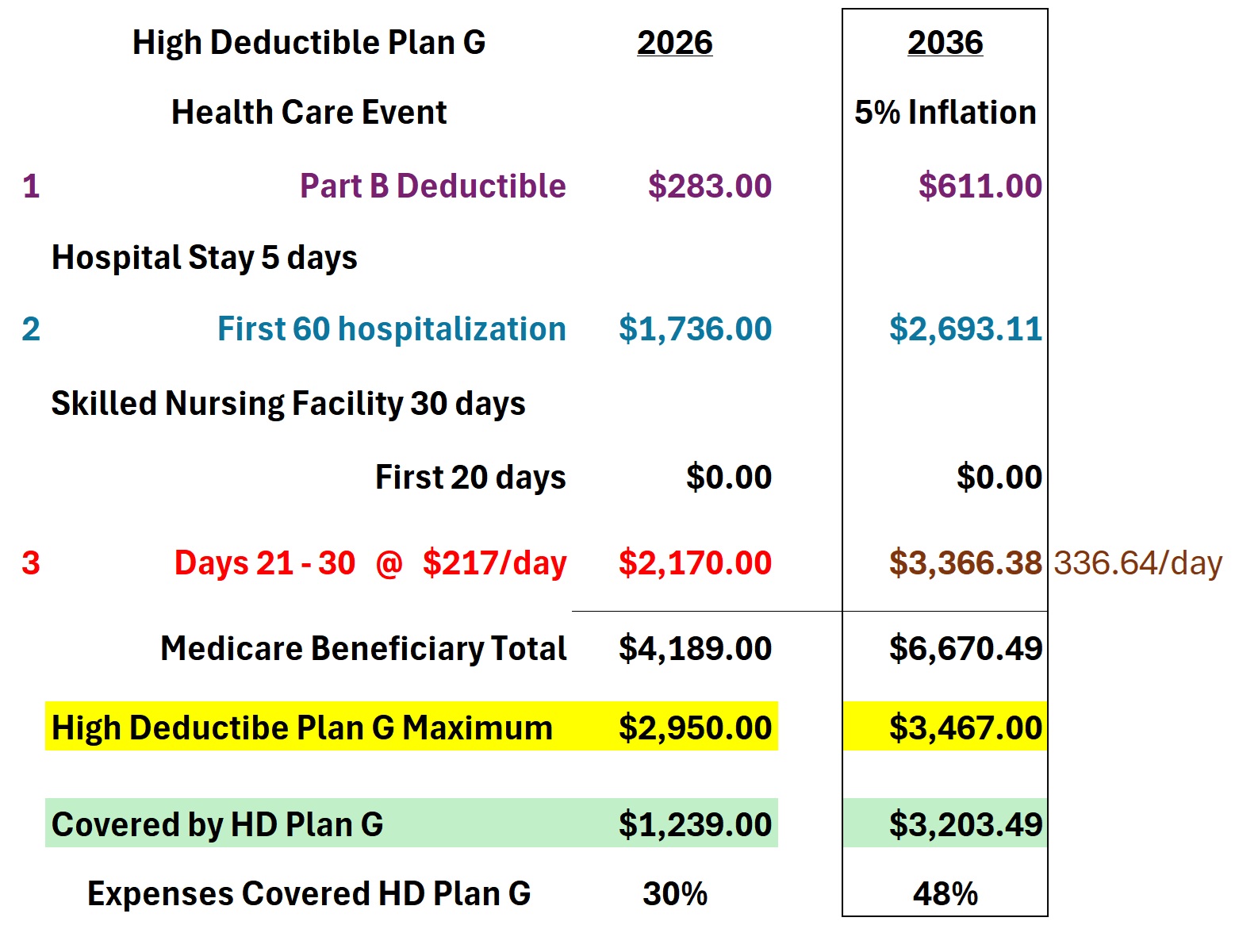

But does the High Deductible Plan G protect you from catastrophic Medicare health care costs? In the example below, the Medicare beneficiary has a medical event where they must be hospitalized for five days. They must then reside in a skilled nursing facility for 30 days to recuperate. The costs are 2026 and 2036 where a 5 percent inflation adjustment has been applied to the Medicare costs.

With either the High Deductible or standard Plan G you will have to pay the Part B deductible. Under Original Medicare, the first 60 days of hospitalization has a set copayment of $1,736 in 2026 and potential copayment of $2,693 in 2036. With Original Medicare, the first 20 days in a skilled nursing facility is $0. Days 21 – 100 are $217 per day for 2026, $336 per day in 2026 under our 5 percent inflation scenario. (For the inflation increase, I applied the 5 percent to each year for the specific costs. For example, $100 x 1.05 = $105 year 2. $105 x 1.05 = $110.25 year three, etc., for the ten year period.)

The High Deductible Plan G deductible will also increase according to the Consumer Price Index. This means that under the 5 percent inflation assumption, the 2026 deductible of $2,950 increases to $3,467. After the High Deductible Plan G deductible in 2026, the plan then covers the remainder of Medicare health care costs of $1,239 of the total Medicare health care costs of $4,189.

For the 2036 scenario, after the High Deductible Plan G deductible of $3,467, the plan covers the remaining $3,203 of the total Medicare health costs of $6,670. The big assumption in this future scenario is that Original Medicare cost sharing does not increase faster than the Consumer Price Index inflation percentage.

High Deductible Plan G Considerations

You should only consider a High Deductible Plan G only if you know you will have the money in savings to cover the deductible amount of the plan. Use caution if you are assuming that the premium savings of the High Deductible Plan G will fund the deductible of the plan. While we don’t expect major health care events every year, it is possible to accrue significant Medicare health care costs with chronic illness over several years and always having to meet the deductible of the High Deductible Plan G.

Another consideration is, under most situations, if you enroll in the High Deductible Plan G, and later want to move to a Plan G, you will have to answer medical questions to get approved. If you have a cancer diagnosis or a physician has told you that surgery is necessary, you most likely will not be accepted for the higher coverage of Plan G.

The High Deductible Plan G Medicare Supplement provides a reasonable annual maximum out of pocket amount. In other words, you know that you have a backstop, maximum liability, to Medicare health care costs with the High Deductible Plan G without the higher premiums of a standard Plan G. If you have tolerance for higher medical costs under Medicare, couple with a lower monthly premium, a High Deductible Plan G is worth considering.

YouTube video of High Deductible Plan G costs.