Other plans may have an out-of-network deductible of $500 to $750+. The out-of-network deductible must be satisfied before the plan begins to share in the cost of the health care services or out-of-network services.

Kevin Knauss: Health, History, Travel, Insurance

Posts focusing on Medicare Parts A, B, C and D, Medicare Advantage, Supplements, changes in benefits, enrollment.

Other plans may have an out-of-network deductible of $500 to $750+. The out-of-network deductible must be satisfied before the plan begins to share in the cost of the health care services or out-of-network services.

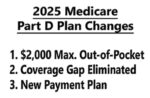

The 2025 Medicare Part D standard benefit structure will have a $590 deductible. After the drug deductible is met the plan member goes into the initial coverage phase. During the initial coverage phase, the plan member is responsible for 25 percent of the drug costs.

Not all the below options may be available to you because some are contingent on your age, employment, or income. Those health insurance alternatives available to you are worth investigating and considering if they meet your budget or adequately address health care challenges you may be facing.

Medi-Cal breaks up the income into unearned income, earned income, in kind income, and exempt income. Finally, there are certain expenses that will reduce the final countable income for eligibility in the Medicare Savings Program.

Pat and Don are a married couple. Pat is age 67 and Don is age 64. Pat retires from work and leaves the employer group plan. Pat activates Part B of Medicare. For the last filed tax year, the modified adjusted gross income for Pat and Don was $350,000. Pat will be subject to an Income Related Monthly Adjustment Amount for the Part B and Part D.

Once you leave your job and the health plan, you must enroll in Part B in order to enroll in a Medicare Supplement or Medicare Advantage plan. In this situation, enrollment can be a little confusing.

The paths to health insurance in California: Medi-Cal, IFP, Employer, Medicare, overview.

Of all the Medicare plans, the Part D Prescription (PDP) plans are the most confusing. The confusion arises because Medicare allows the Part D plans to offer alternate plans that differ from the standard plan. The alternate plans must be as good as the standard plan for the average Medicare beneficiary. Cost Sharing of the […]

If you find yourself in a Medicare Advantage plan you do not like, you have an escape hatch to another plan. The Medicare Advantage Open Enrollment Period is a short period of time when you can escape from your current enrollment, switch to another Medicare Advantage plan, or return to Original Medicare with a Part […]

Medicare Advantage plans, that cannot be paired with a Medicare Supplement plan, is another way to divert much of the storm of health care costs to the gutters and downspouts. The Medicare Advantage plans usually have the Part D drug plan embedded within the total package. There will still be some leaks from copayments and coinsurance with the Medicare Advantage plans.